Market Recap: 5-9 May 2025

Financial Markets

US Stock Market

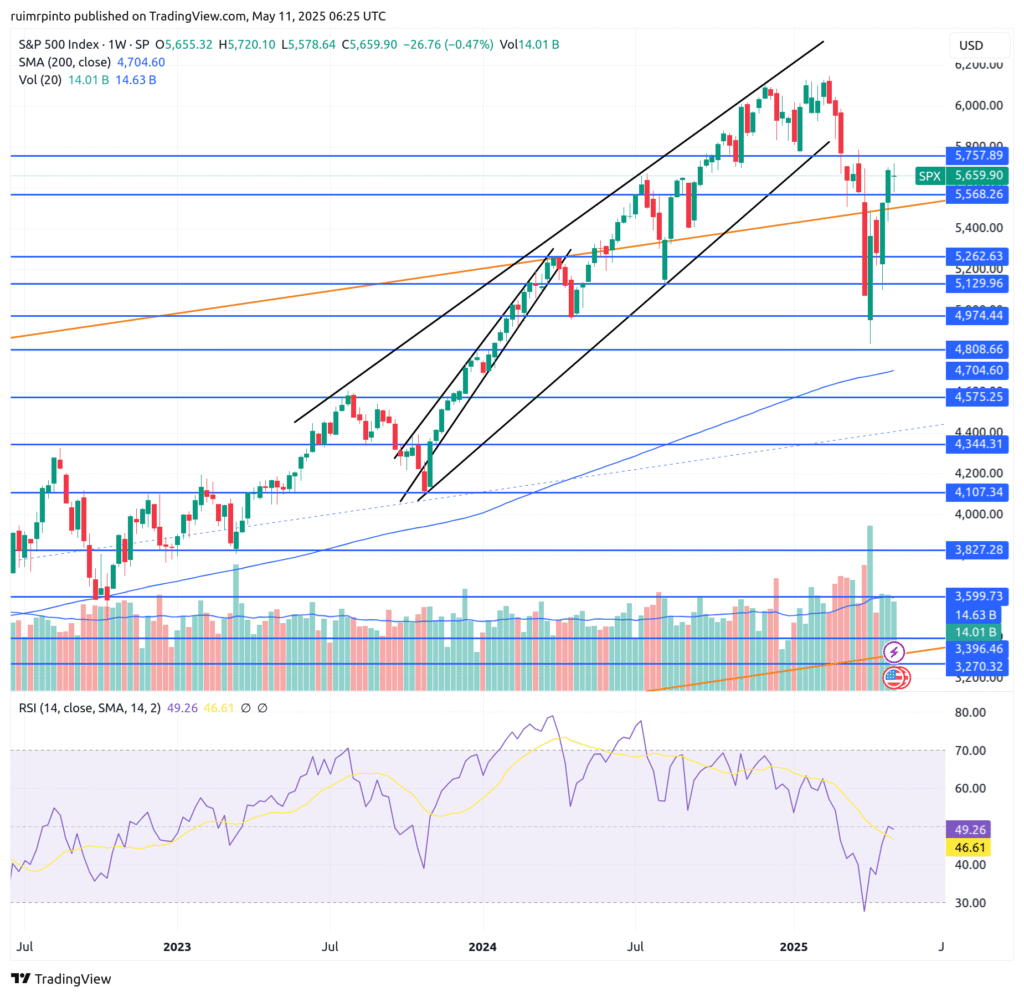

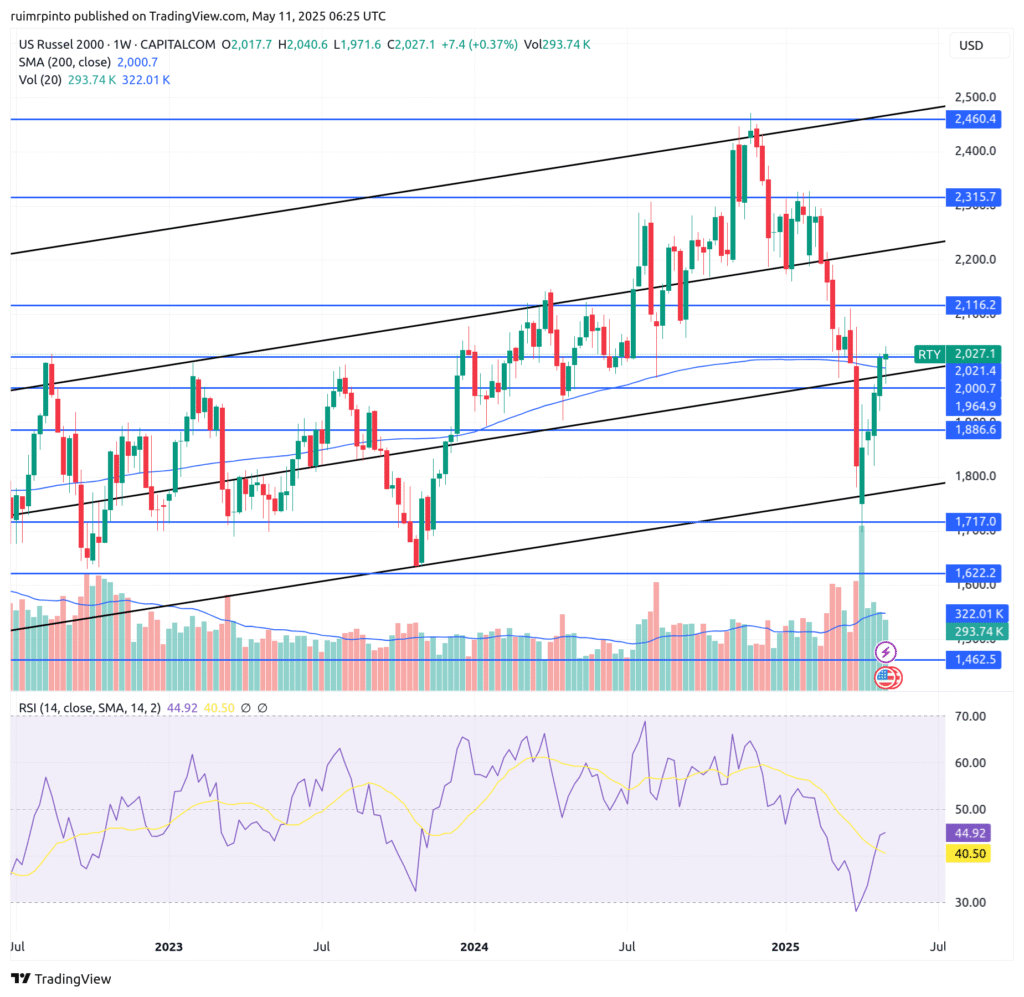

This week the S&P500 and the NASDAQ 100 stalled and lost a slight 0.47% and 0.2%, respectively. As we said last week, on the way up, the S&P encountered resistance around ~5650. The small cap index (Russel 2000) was up by 0.4% and should stall around current levels. Trading volumes were average.

COMMODITIES

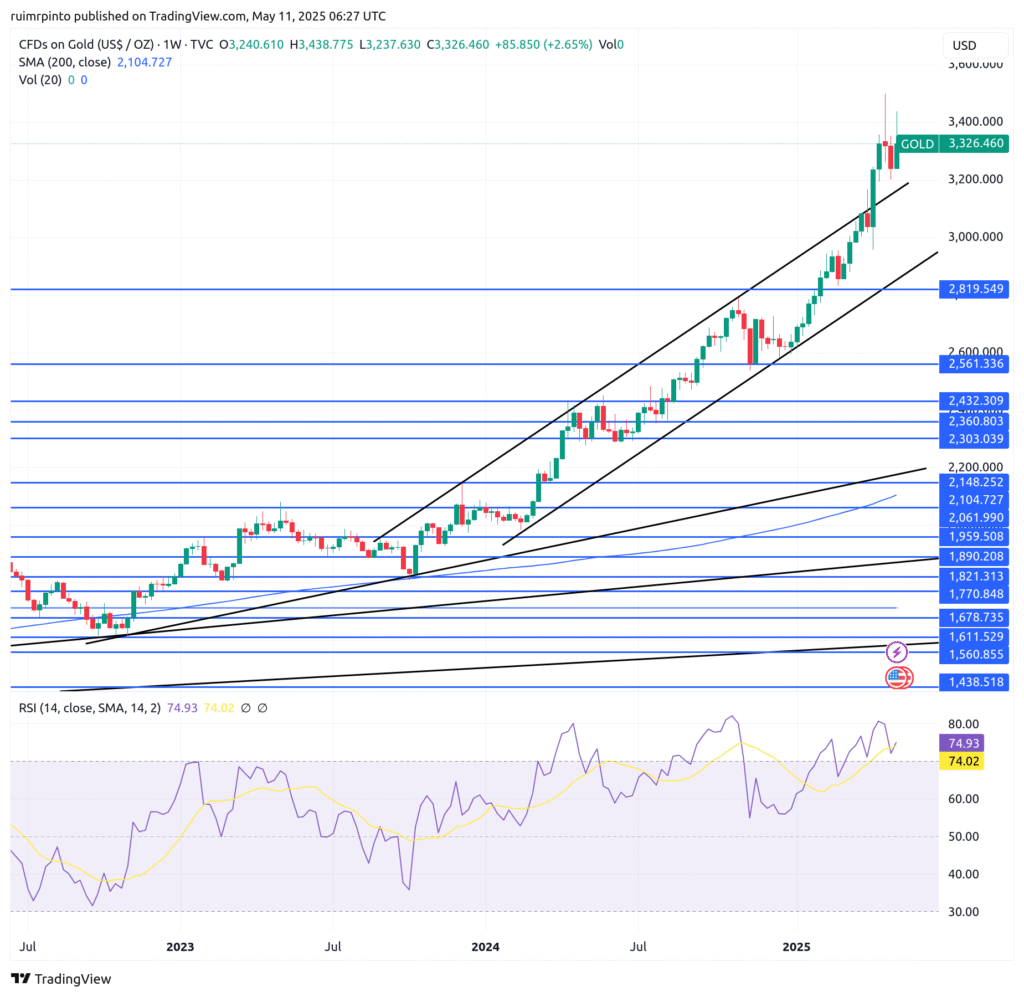

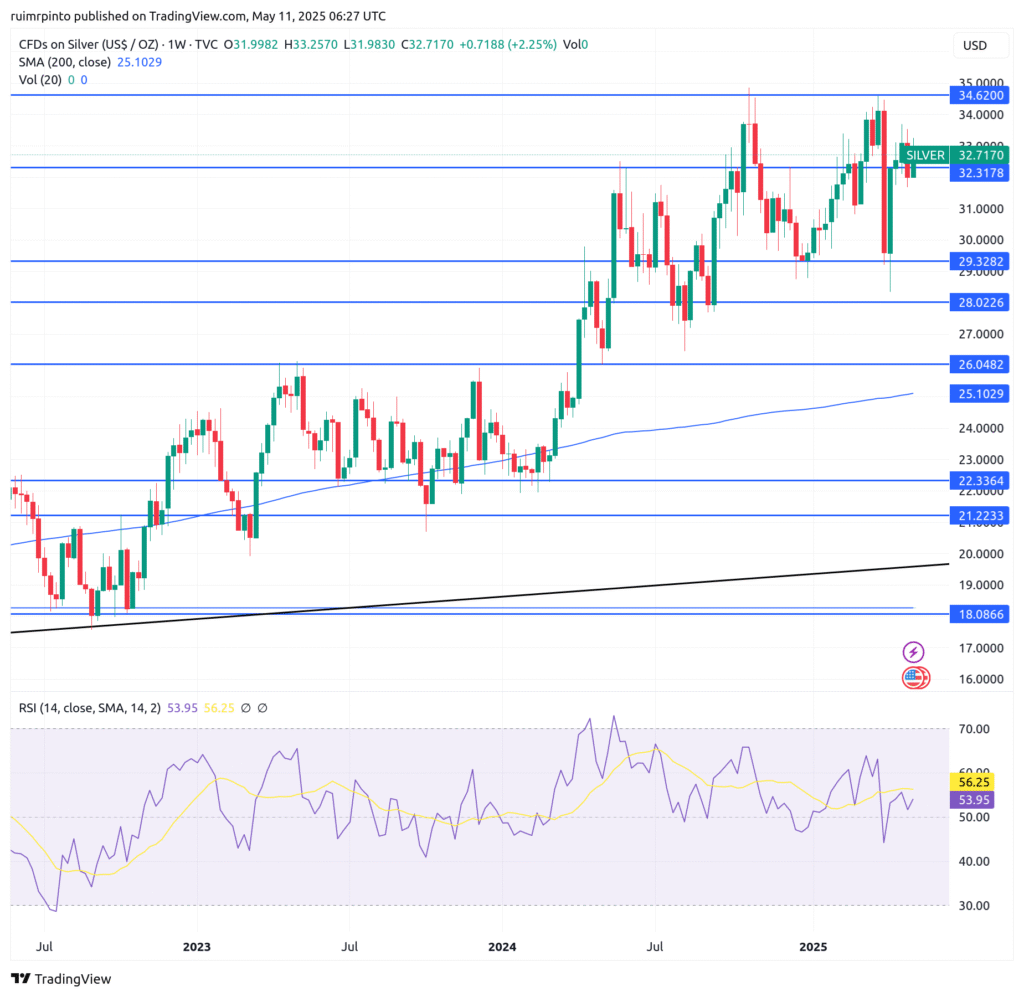

Precious metals held their levels this week, with gold and silver gaining 2.7% and 2.3%, respectively. In the near future gold may consolidate around current levels, at the top-end of the previous trend. Silver closed at ~32.7$/oz, and continues on a lateral trend – it seems stuck in the range 29-34$/oz.

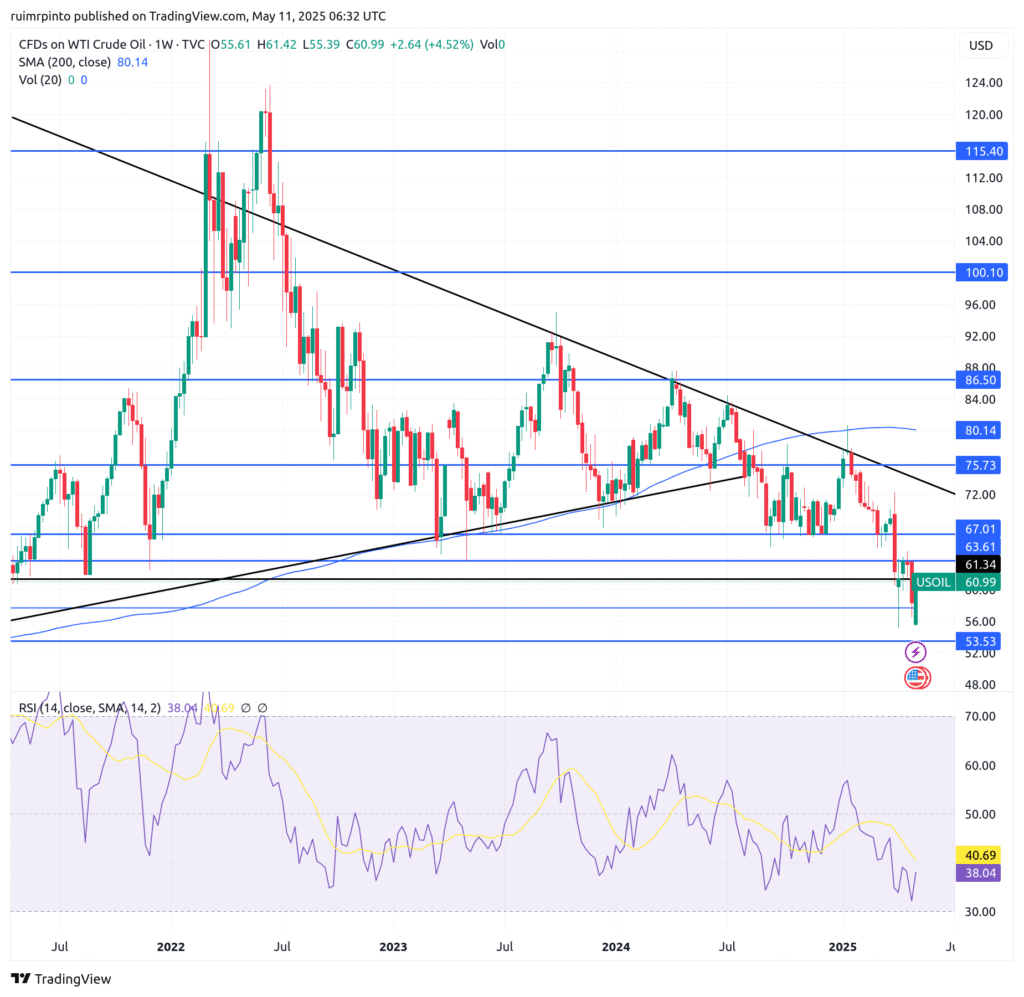

WTI crude oil fell momentarily to 55$ but recovered and closed the week at 61$/bbl. The trading range for the near future seems to be 54-64$/bbl, but oil may be subject to large swings due to wider macroeconomic developments.

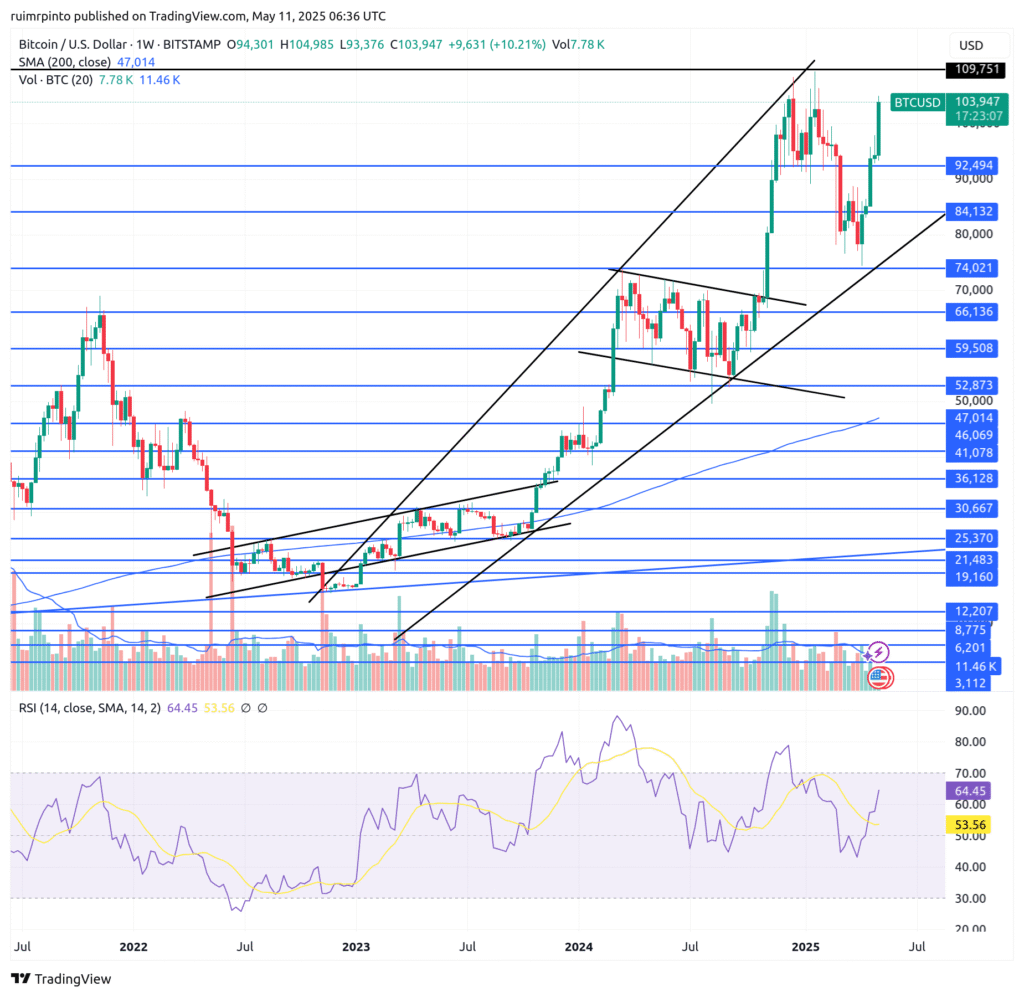

Bitcoin got pumped up this week by a whopping 10.2%, and is now around 104k$, close to all-time highs! Notice, however, the lower volume (below average)! The key resistance and support levels on Bitcoin, for the short term, are 109k$ and 92k$, respectively.

US DOLLAR, MONEY SUPPLY

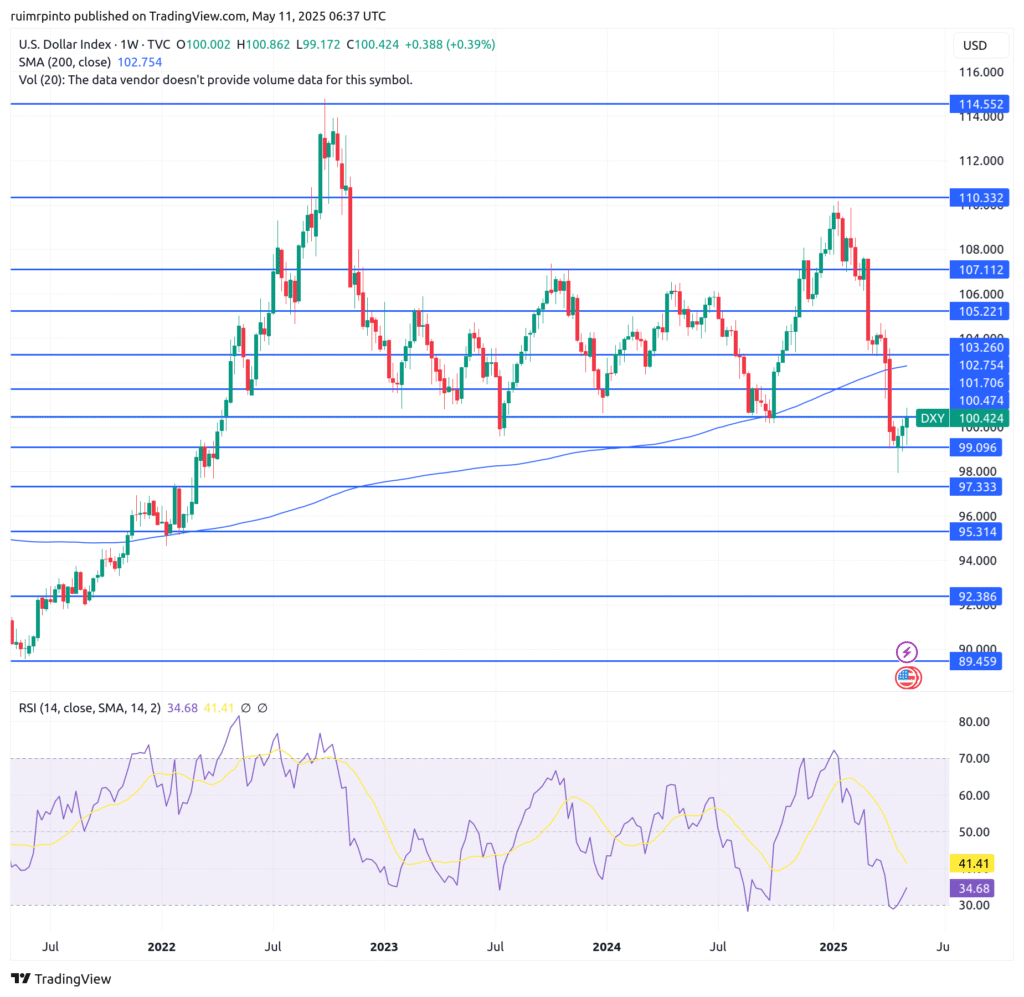

The relative strength of the US dollar (DXY) rose slightly (by 0.4%) during the week and closed at ~100.4. A weaker dollar may help the US to improve the competitiveness of their exports. The EUR/USD is around 1.125$, the GBP/USD is at 1.331$, and the USD/JPY is at 145.36 JPY.

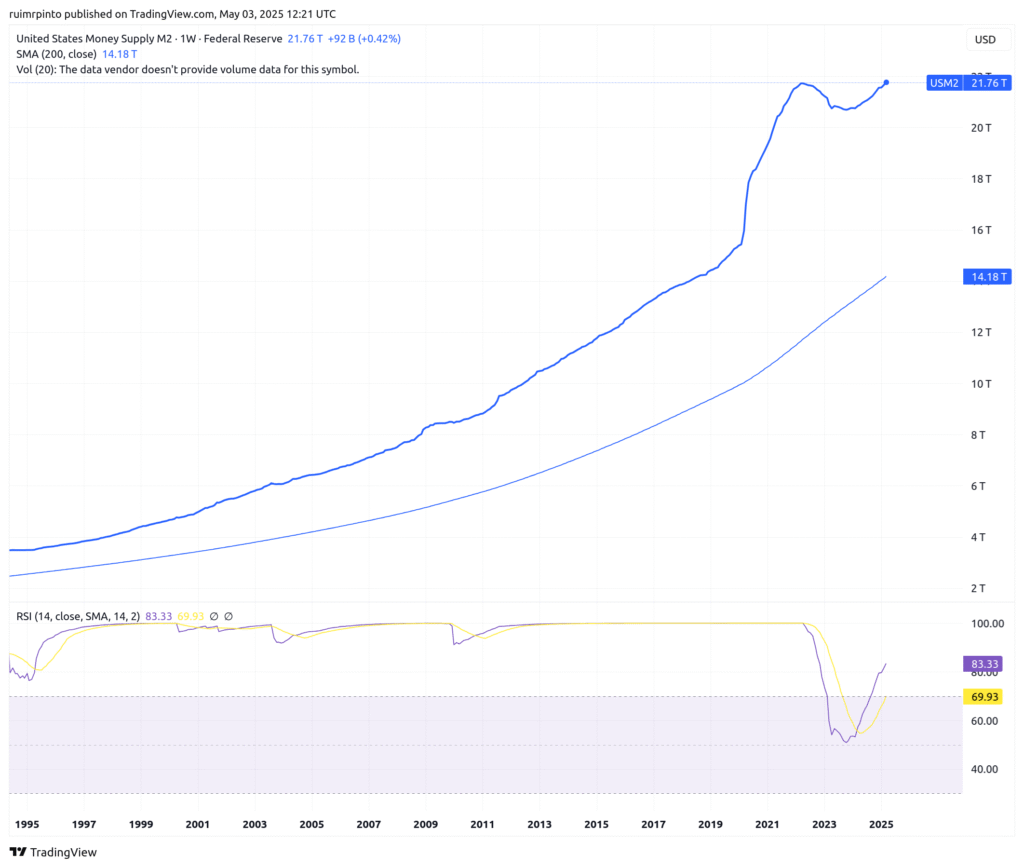

US M2 money supply at the date of 31st March 2025 was up by 0.4%, showing a slow increase over the previous month. If the money supply was going down, it would be another warning sign for the economy and equities. If financial stress in the banking system continues piling up, we will probably see a decrease of the money supply…

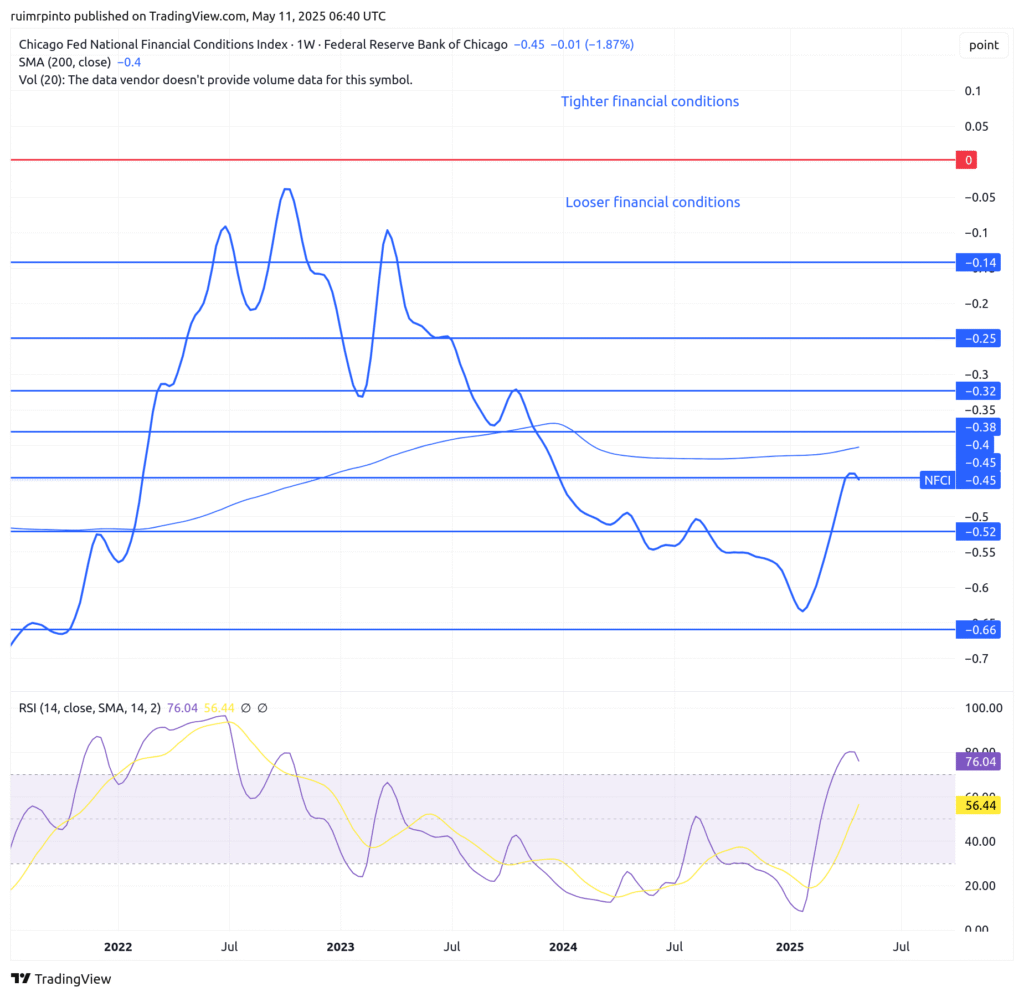

The national financial conditions index (NFCI) released on the 28st April 2025 loosened by 1.87%. Note that this indicator is delayed by two weeks. Positive numbers in the NFCI mean tighter financial conditions, while negative numbers indicate looser financial conditions.

BONDS AND OPTIONS

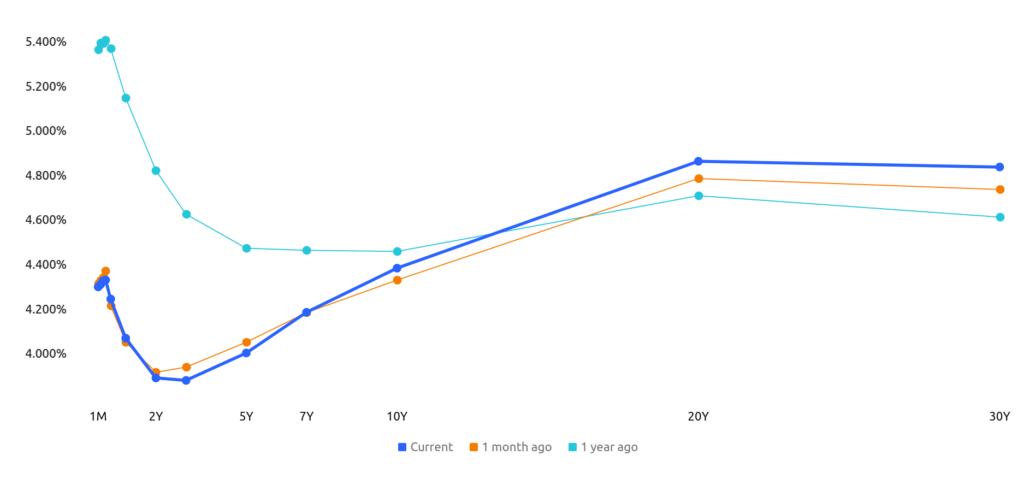

US bond yields rose slightly this week. Yields now sit at 3.889% for the 2-year and 4.382% for the 10-year. As you can see, the yield curve has uninverted since a year ago, and lower yields are expected in the next few years, likely as a consequence of a recession and interest rate cuts.

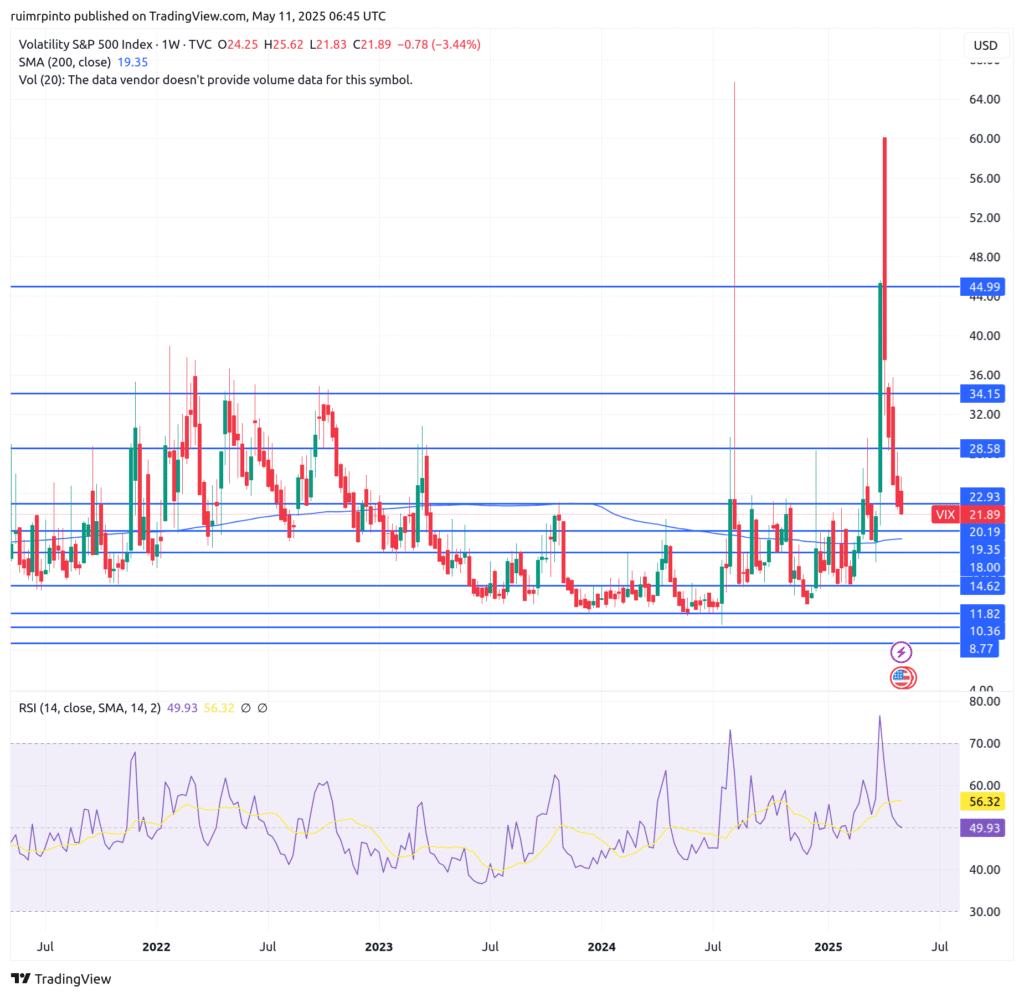

The VIX closed the week at ~21.8, showing a continuing decrease in risk perception in the options market. Soon, we will enter again into complacency territory. In our opinion, the overall systemic risk in the stock market and uncertainty about the US economy is too high to be fully allocated to stocks on the long side. At this point, we wouldn’t recommend selling puts unless you are really comfortable buying the underlying asset (cash-secured puts)!

Comment Section

This week was neutral in the equity markets, as we reach technical resistance and economic fundamentals stagnate. No major economic indicators were released except for the ISM Services PMI which remained slightly above 50.

On Wednesday, we had the FOMC meeting and the resulting interest rate decision and press conference. There was no change in the overnight rate (4.5%), but during the press conference it seemed that Jerome Powell is predicting a stagflation scenario. Prices will rise when tariffs enter in effect, but inflation may be more sticky, he said (in slightly different words). The FED will be in a reactionary mode, and waiting for incoming data regarding unemployment and inflation, to achieve its dual mandate of maximum employment and price stability.

This week, the White house announced an historic trade deal with the UK, but in fact, this deal only reduced or removed tariffs on some of the UK’s exports, including cars, steel and aluminum. President Donald Trump’s blanket 10% tariffs on imports from countries around the world still applies to most UK goods entering the US. So far, it seems that 10% tariffs could be the best deal other countries and trading blocs will achieve, according to analysts. The US insists that “President Trump continues to advance the interests of the American people, enhancing market access for American exporters and lowering tariff and non-tariff barriers to protect our economic and national security.”.

On Sunday, Reuters announced a positive development for the possible resolution of the Russia-Ukraine conflict:

“Russian President Vladimir Putin on Sunday proposed direct talks with Ukraine on May 15 in Turkey that he said should be aimed at bringing a durable peace, an initiative welcomed by U.S. President Donald Trump. Putin sent thousands of troops into Ukraine in February 2022, unleashing a war that has left hundreds of thousands of soldiers dead and triggering the gravest confrontation between Russia and the West since the 1962 Cuban Missile Crisis.”

Next week, producer prices, industrial production, Michigan consumer sentiment, export and import prices, as well as building permits and housing starts will be released. The earnings season remains in focus, with major reports expected from Cisco, Tencent, Alibaba, SoftBank, Walmart, and Target.

Have a nice weekend, and good luck!!!

Sources:

https://www.tradingeconomics.com

https://www.bbc.com/news/articles/c15ng4g5g0eo

https://www.whitehouse.gov/fact-sheets/2025/05/fact-sheet-u-s-uk-reach-historic-trade-deal

https://www.reuters.com/world/europe/putin-proposes-direct-talks-with-ukraine-may-15-2025-05-10