Financial Markets

US Stock Market

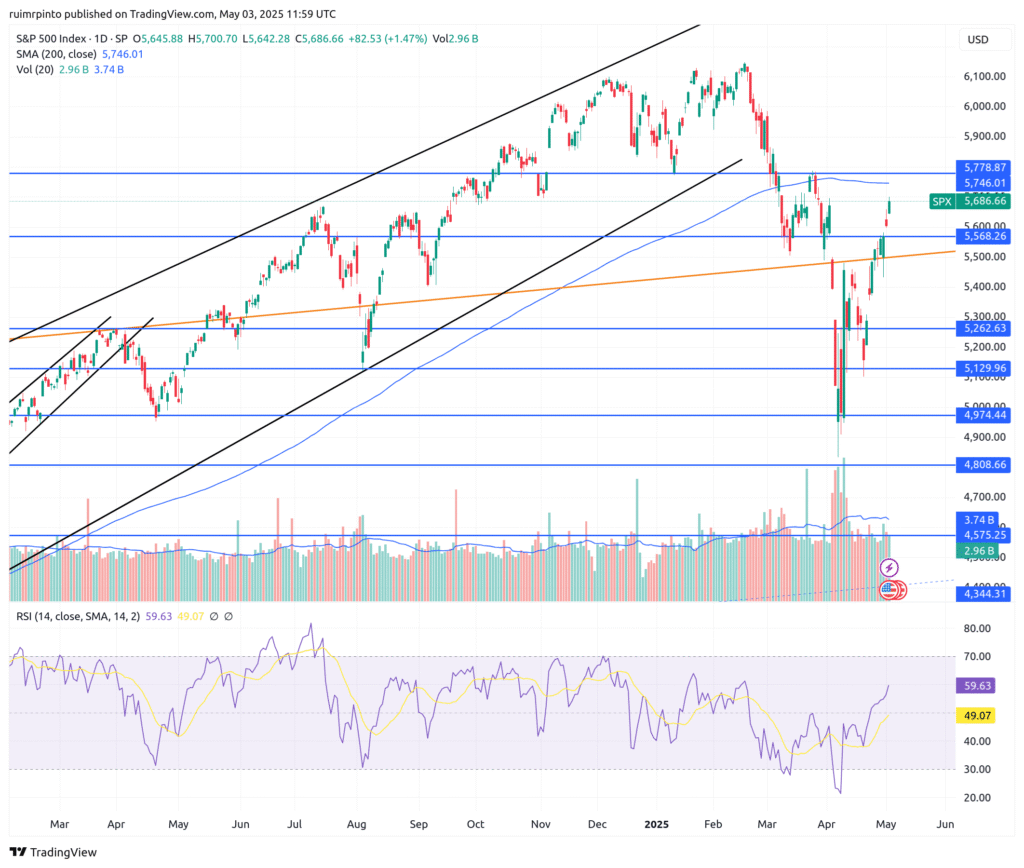

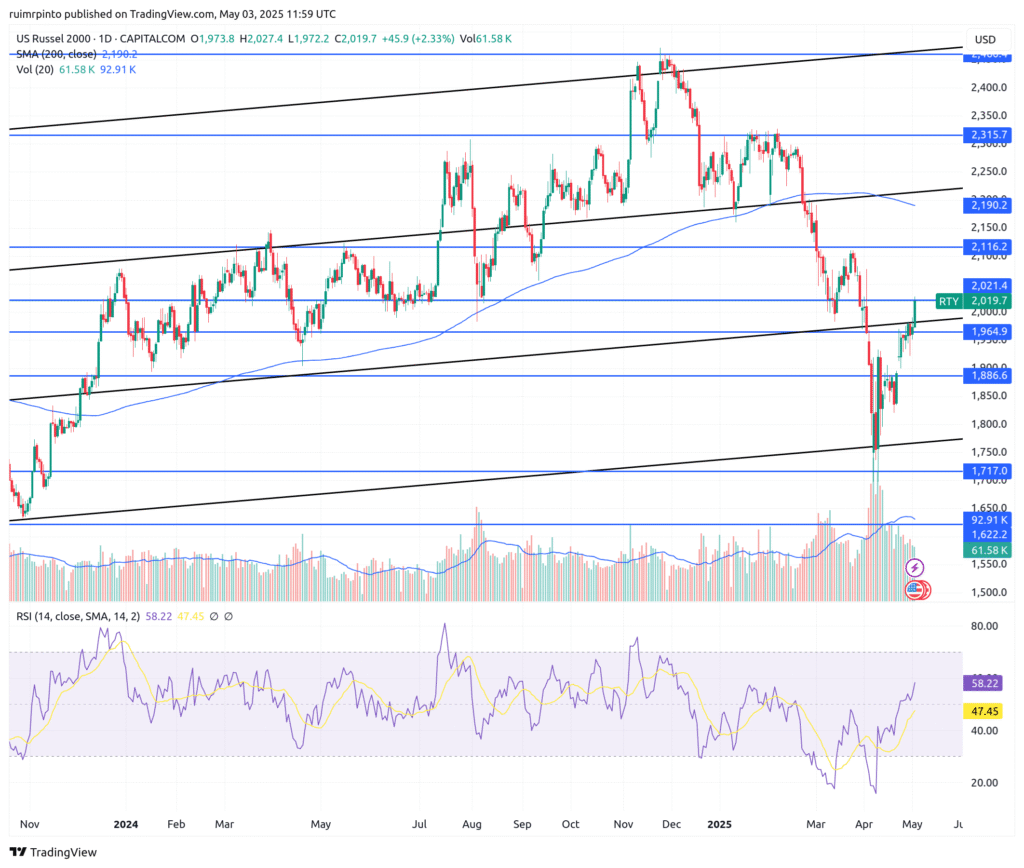

This week the S&P500 and the NASDAQ 100 continued recovering and rose by 2.9% and 3.5%, respectively. On the way up, the S&P may encounter resistance around ~5650. The small cap index (Russel 2000) was up by 3.3%. Trading volumes were average.

COMMODITIES

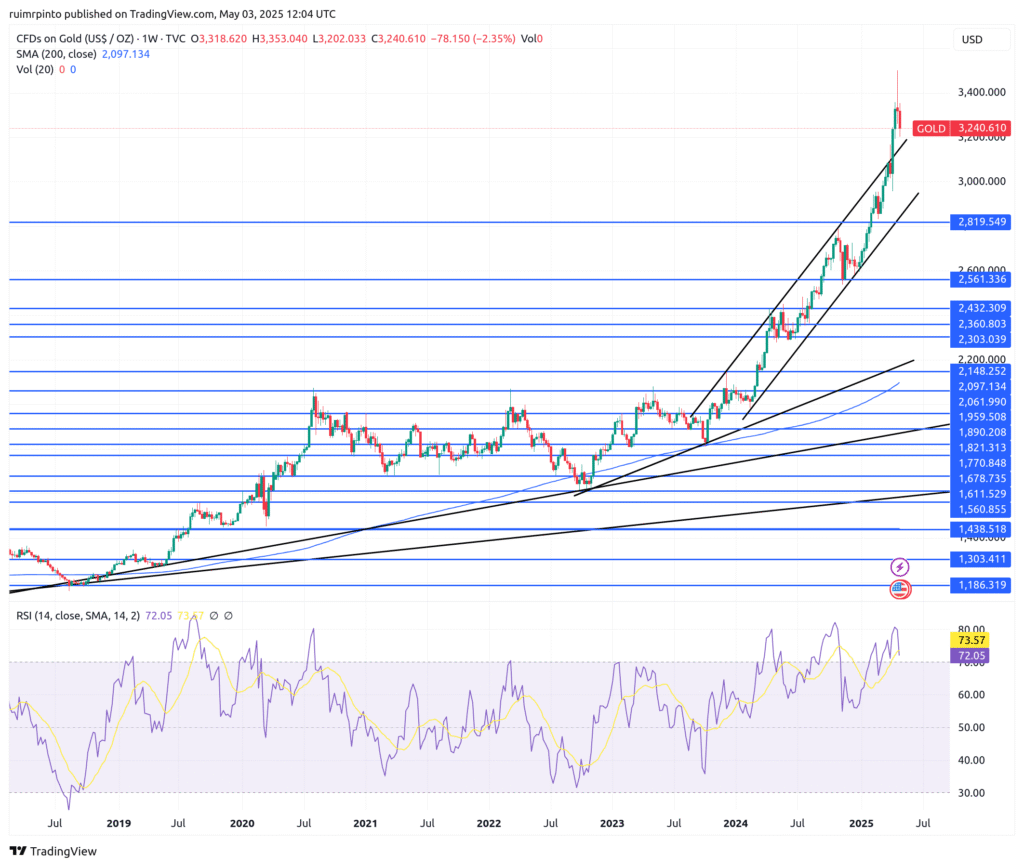

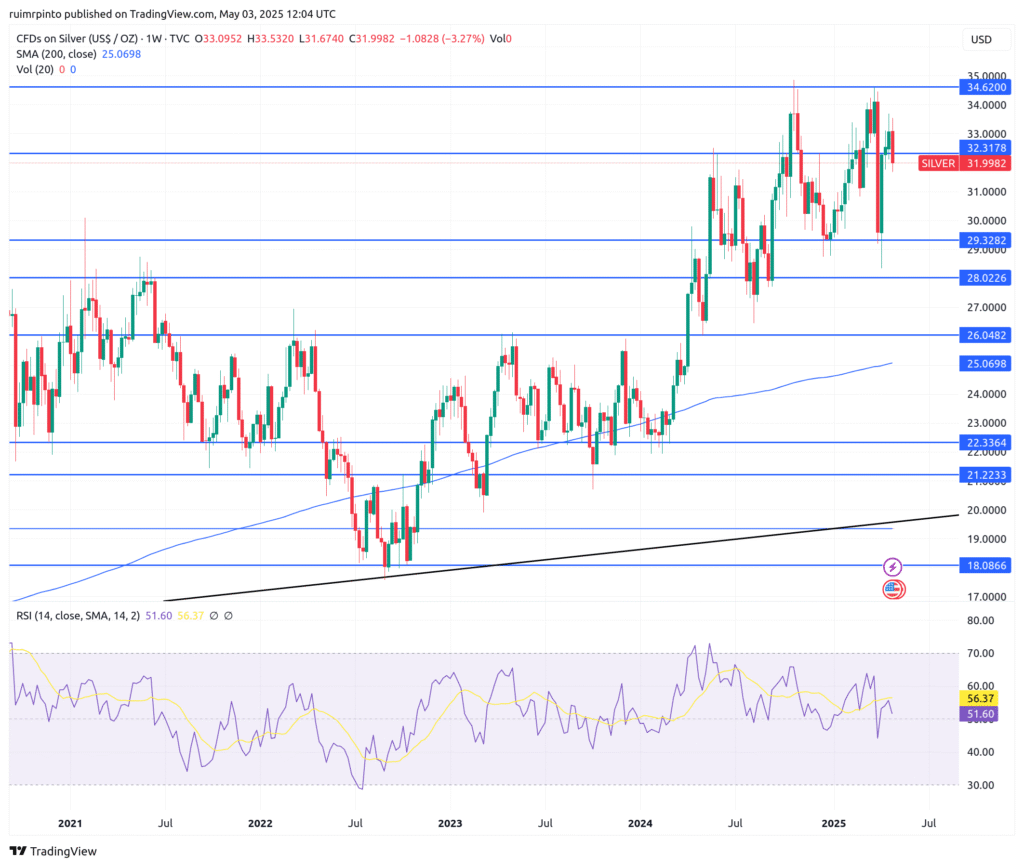

Precious metals corrected this week, with gold and silver dropping by 2.4% and 3.3%, respectively. In the near future gold may retrace back to ~3150$, at the top-end of the previous trend. Silver closed at ~32$/oz, and continues on a lateral trend – it seems stuck in the range 29-34$/oz.

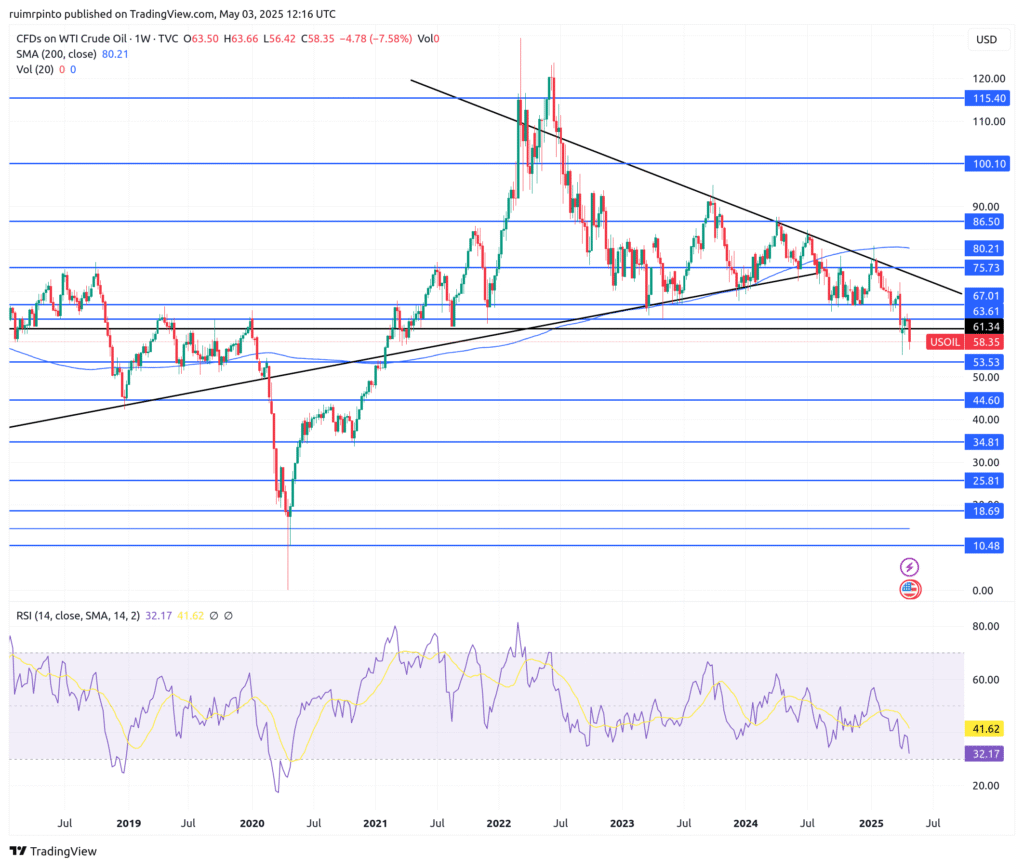

WTI crude oil fell by 7.6% and closed the week at 58.3$/bbl. If it continues falling (the most likely scenario), the next support level is around 54$. On the upside, 62-64$ will likely offer resistance.

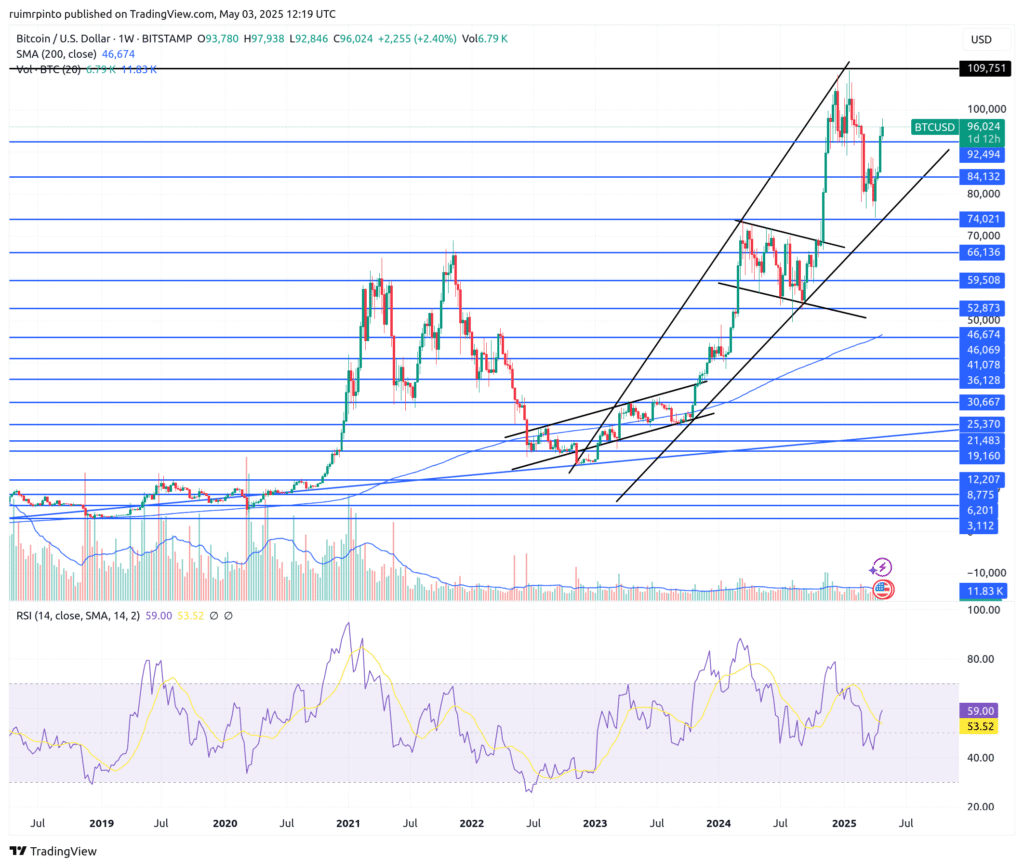

Bitcoin accompanied stocks on the way up, and gained 2.4% this week. It is now around 96k$. The key resistance and support levels on Bitcoin, for the short term, are 109k$ and 92k$, respectively.

US DOLLAR, MONEY SUPPLY

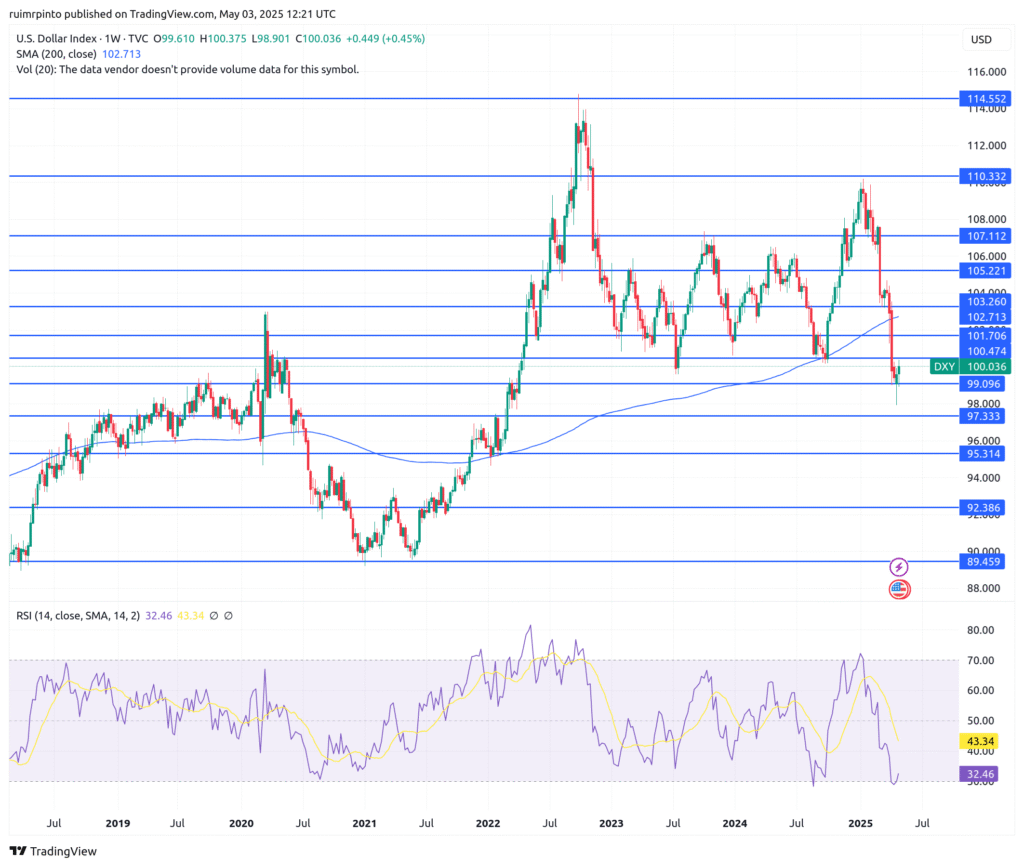

The relative strength of the US dollar (DXY) rose slightly (by 0.45%) during the week but closed essentially unchanged relative to the previous period, at ~100. A weaker dollar may help the US to improve the competitiveness of their exports. The EUR/USD is around 1.129$, the GBP/USD is at 1.327$, and the USD/JPY is at 144.98 JPY.

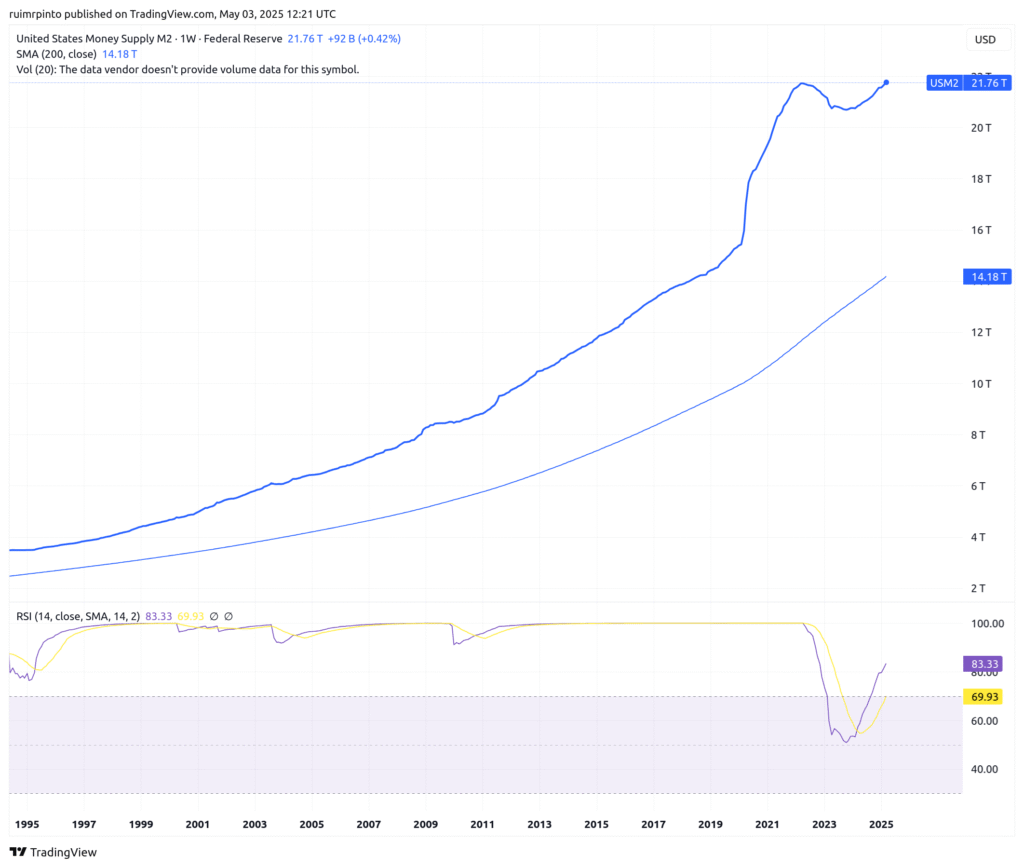

US M2 money supply at the date of 31st March 2025 was up by 0.4%, showing a slow increase over the previous month. If the money supply was going down, it would be another warning sign for the economy and equities. If financial stress in the banking system continues piling up, we will probably see a decrease of the money supply…

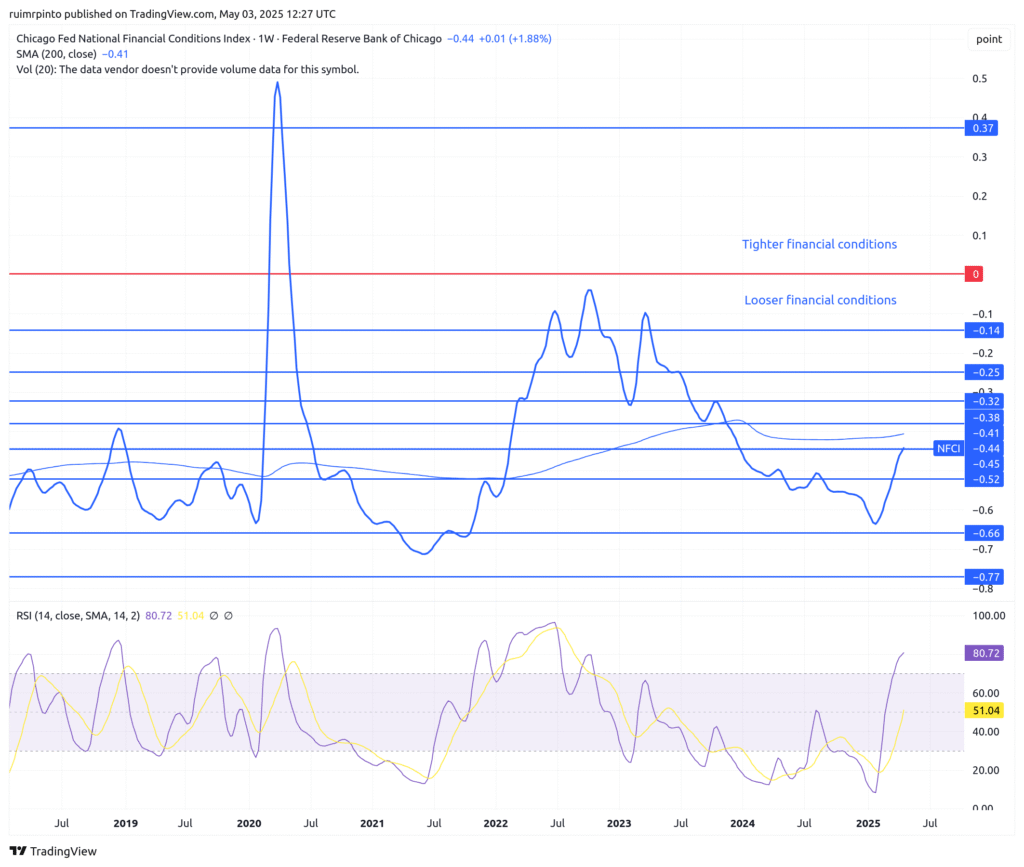

The national financial conditions index (NFCI) released on the 21st April 2025 tightened by 1.9%. Note that this indicator is delayed by two weeks.

BONDS AND OPTIONS

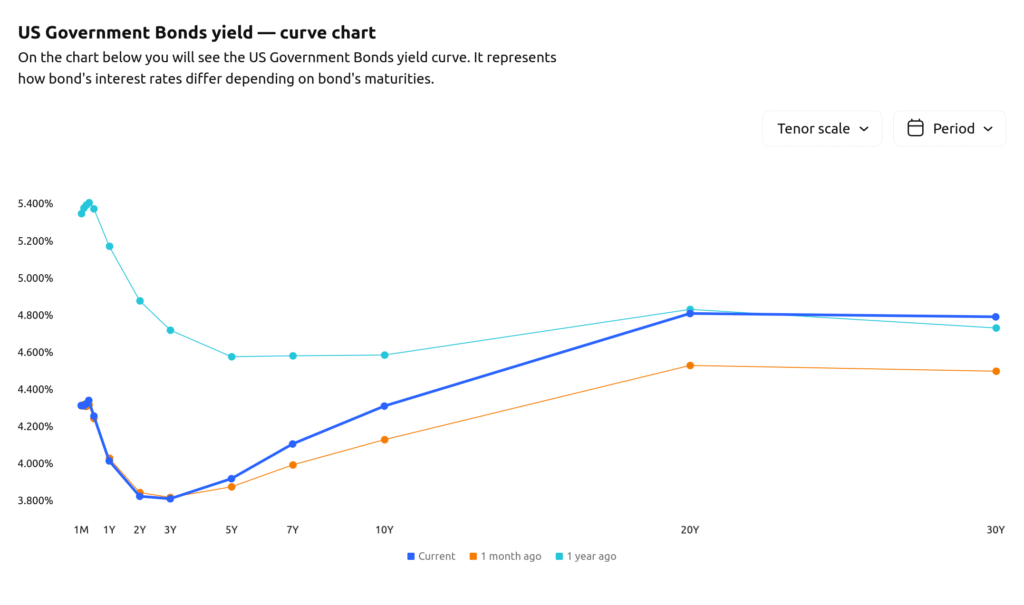

US bond yields rose slightly this week. Yields now sit at 3.822% for the 2-year and 4.308% for the 10-year.

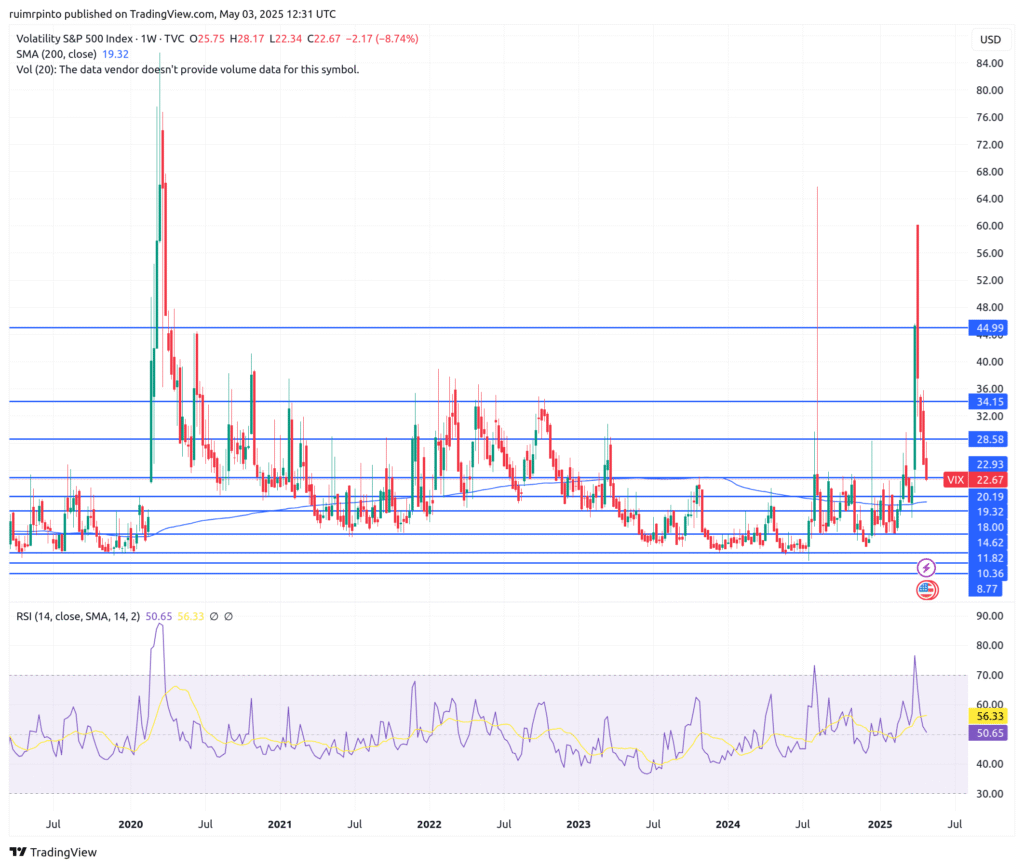

The VIX closed the week at ~23, showing a decreasing risk perception in the options market. Soon, we will enter again into complacency territory. In our opinion, the overall systemic risk in the stock market and uncertainty about the US economy is too high to be fully allocated to stocks on the long side. At this point, we wouldn’t recommend selling puts unless you are really comfortable buying the underlying asset (cash-secured puts)!

Macroeconomic Indicators

The ISM Manufacturing PMI for the U.S. slipped to 48.7 in April 2025 from 49.0 in March, slightly above market expectations of 48. The reading signaled a second consecutive month of contraction in the manufacturing sector as output shrank more sharply (44.0 vs. 48.3) and prices rose further (69.8 vs. 69.4). A PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining.

China PMI indicators came out close to 50, indicating neither expansion nor contraction.

US job openings in the United States fell by 288,000 to 7.192 million in March 2025, the lowest in six months and well below market expectations of 7.48 million. In the United States, job openings refer to all positions that are open (not filled) on the last business day of the month. Job openings are part of the Job Openings and Labor Turnover Survey (JOLTS). The survey collects data from around 16400 nonfarm establishments including retailers and manufacturers, as well as federal, state, and local government entities in the 50 states and the District of Columbia. The JOLTS assesses the unmet demand for labor in the U.S. labor market.

However, on Friday, the strong jobs report helped alleviate concerns about the potential for a sustained economic downturn. US Non Farm Payrolls showed that the U.S. economy added 177,000 jobs in April 2025, a slowdown from the downwardly revised 185,000 in March, but significantly surpassing market expectations of 130,000. This figure aligns closely with the average monthly gain of 152,000 over the past 12 months, despite growing uncertainty surrounding President Donald Trump’s aggressive tariff policies. Job growth was primarily seen in sectors such as health care (+51,000), transportation and warehousing (+29,000), financial activities (+14,000), and social assistance (+8,000), while federal government employment experienced a decline (-9,000).

Initial jobless claims in the United States rose by 18,000 to 241,000 in the week ending April 26, the highest since February and well above market expectations of 224,000. US Unemployment rate (4.2%), average hourly earnings (0.2% MoM) and participation rate (62.6%) are stable and were within expectations.

In the United States, the personal consumption expenditure (PCE) price index was unchanged in March from February 2025, the least in ten months, and following a 0.4% rise in each of the previous two months, in line with expectations. The annual PCE rate decreased to 2.3%, the lowest in five months, and the annual core PCE inflation also eased to 2.6%. The Personal Consumption Expenditure Price Index provides a measure of the prices paid for domestic purchases of goods and services. While the Consumer Price Index assumes a fixed basket of goods and uses expenditure weights that do not change over time for several years, the Personal Consumption Expenditure Price Index uses a chain index and resorts on expenditure data from the current period and the preceding period (known as Fisher Price Index). Chain indexes, like the PCE, use weights from both the current and preceding periods (Fisher Index) to better reflect how consumers change their spending patterns in response to price changes.

Comment Section

This week was positive for the equity markets, especially on Friday, after the release of the jobs report, fueling shares of numerous companies in the travel industry . United Airlines Holdings (UAL) shares lifted 7.1%, while Delta Air Lines (DAL) shares advanced 6.6%. Shares of cruise operator Norwegian Cruise Line Holdings (NCLH) were up 6.8%.

This week, Amazon, Apple, and Meta (members of the “Magnificent Seven”) reported earnings and exceeded EPS expectations for Q1 2025.

Amazon (AMZN) reported EPS (Q1 2025) of $1.59, a change of +62% from Q1 2024 (up from $0.98). Online store sales increased by 6%, and advertising revenue grew by 19%. However, Amazon Web Services (AWS) growth slowed to 17%, slightly under analyst expectations. The company provided a cautious outlook for Q2, citing uncertainties around consumer demand and potential impacts from U.S. tariff policies.

Apple (AAPL) delivered EPS of $2.40 (Q1 2025), up 10% relative to Q1 2024 (up from $2.18). The Services segment saw significant growth, with revenue reaching $26.3 billion, up 14% year-over-year. Despite these gains, iPhone sales remained flat, and revenue in Greater China declined by 11%, reflecting challenges in that market.

Meta Platforms (META) showed EPS of $6.43 (Q1 2025), up 35% when compared to Q1 2024 (up from $4.76). Meta reported a 35% increase in net income, reaching $16.64 billion, driven by robust advertising revenue across Facebook, Instagram, and WhatsApp. The company highlighted progress in AI initiatives, including AI glasses and the Meta AI platform, which now has nearly 1 billion monthly active users. Despite these positive results, Meta faces regulatory challenges in the EU and concerns over high capital expenditures, which are projected to reach $64–72 billion in 2025.

Regarding Tariffs, there was a development aimed at softening the impact of new auto tariffs: US automakers will receive credits equivalent to 15% of the value of vehicles assembled in the US. These credits can be used to offset the cost of imported parts, according to Reuters. The credits are intended to help automakers shift their supply chains back to the US.

Next week, we should pay attention to potential tariff negotiations between the U.S. and China, the Federal Reserve’s interest rate decision, and subsequent remarks from Fed officials.

Recapping: the fundamentals of the worldwide economy didn’t improve, especially in the west. Most US and European companies are not reporting outstanding revenue. The latest weakness on oil is worrying and signals weaker demand from a slowing economy. However, the official numbers are holding and unemployment has not increased yet. If we had to guess, we would say we are entering a period of stagnation, with a possibility of a recession. We need to be extra careful in tumultuous times like this. If the risks of recession increase, equities will correct again.

Have a nice weekend, and good luck!!!

Pingback: White House Trade Deal with UK, Bitcoin Explodes, Markets Flat-line - Macro Briefs