Market Recap: 19-23 May 2025

Financial Markets

US Stock Market

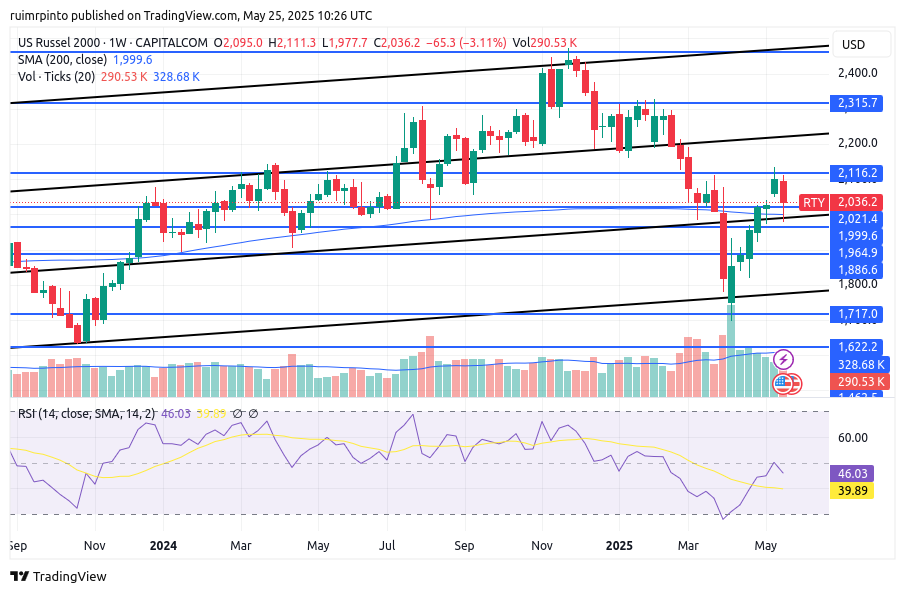

This week the S&P500 and the NASDAQ 100 corrected slightly, losing 2.6% and 2.4%, respectively. The small cap index (Russel 2000) was down by 3.1% and is also around support. Trading volumes were average.

COMMODITIES

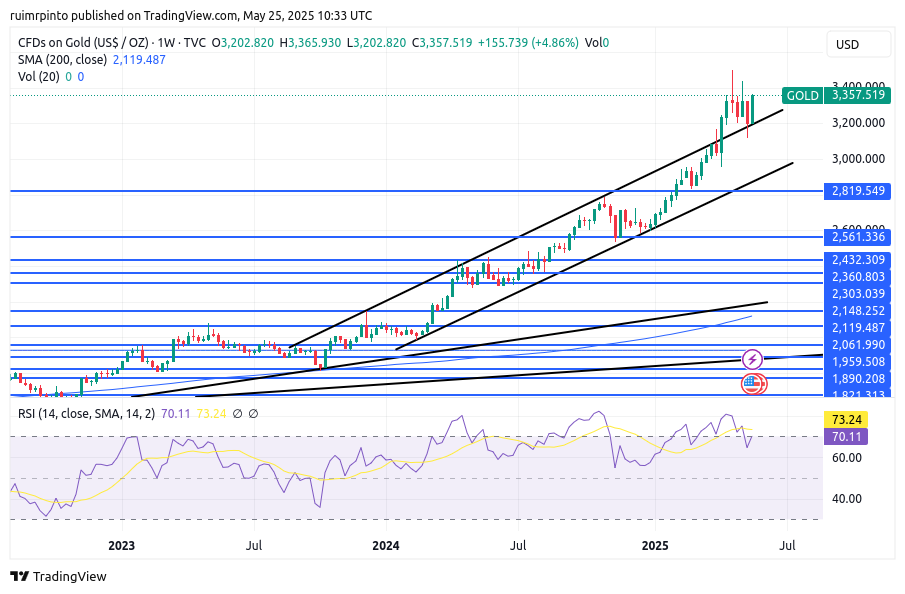

Precious metals held this week. Gold and silver were up by 4.9% and 3.7%, respectively. Gold bounced from the top of the previous trend, but might have difficulty overcoming the recent all-time-highs. Silver closed at ~33.5$/oz, and continues on a lateral trend – it will likely trade in the range 29-35$/oz in the near future.

WTI crude oil was little changed this week, closing at 61.7$/bbl. The trading range in the near future seems to be 54-64$/bbl, but oil may be subject to large swings due to wider macroeconomic developments or major oil producer announcements.

Bitcoin reached 112k$ momentarily, but it was little changed (+0.7%) for the week. The key resistance and support levels on Bitcoin, for the short term, are 112k$ and 92k$, respectively.

US DOLLAR, MONEY SUPPLY

The relative strength of the US dollar (DXY) corrected back down to ~99. The EUR/USD is around 1.136$, the GBP/USD is at 1.354$, and the USD/JPY is at 142.47 JPY.

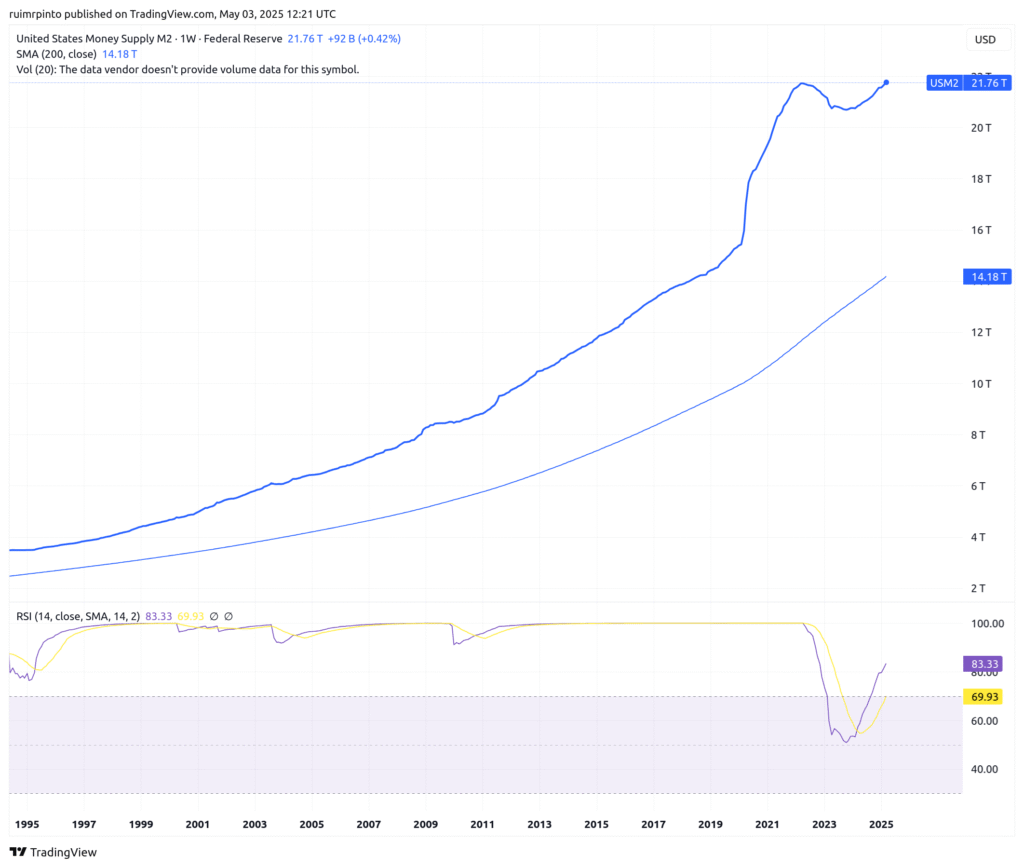

US M2 money supply at the date of 31st March 2025 was up by 0.4%, showing a slow increase over the previous month. If the money supply was going down, it would be another warning sign for the economy and equities.

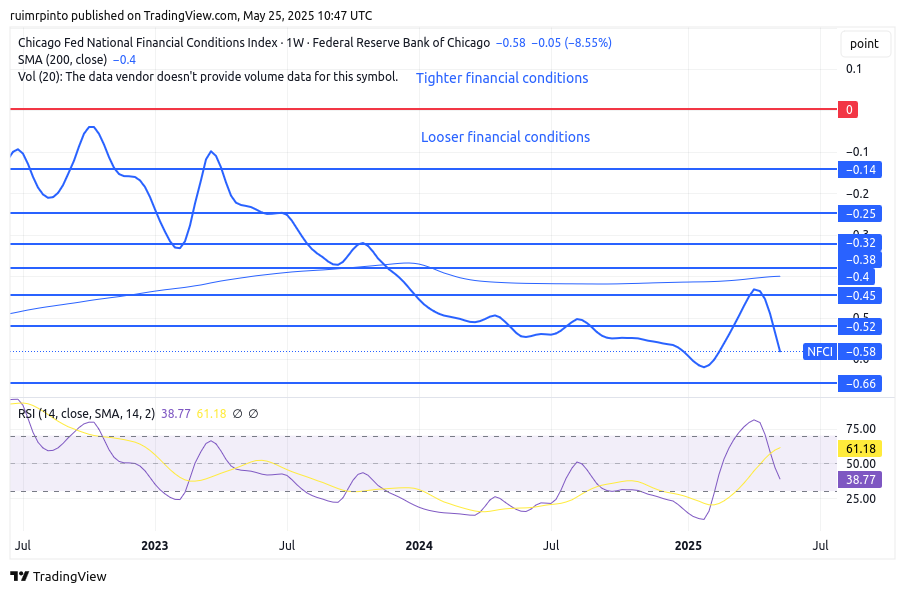

The national financial conditions index (NFCI) released on 12th May 2025 loosened by 8.6%. Note that this indicator is delayed by two weeks. Positive numbers in the NFCI mean tighter financial conditions, while negative numbers indicate looser financial conditions.

BONDS AND OPTIONS

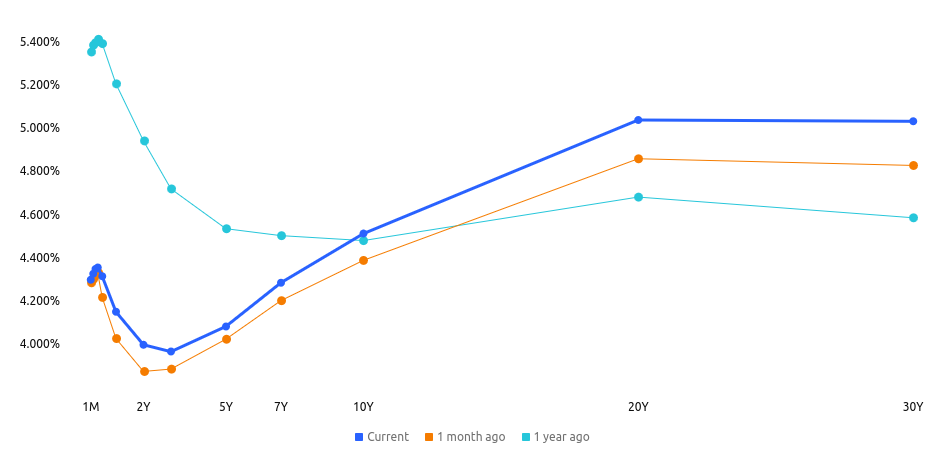

US bond yields rose slightly this week. Yields now sit at 3.993% for the 2-year and 4.509% for the 10-year. As you can see, the yield curve has uninverted since a year ago, and lower yields are expected in the next few years, likely as a consequence of a recession and interest rate cuts. However, long-term growth and inflation expectations are about 5%.

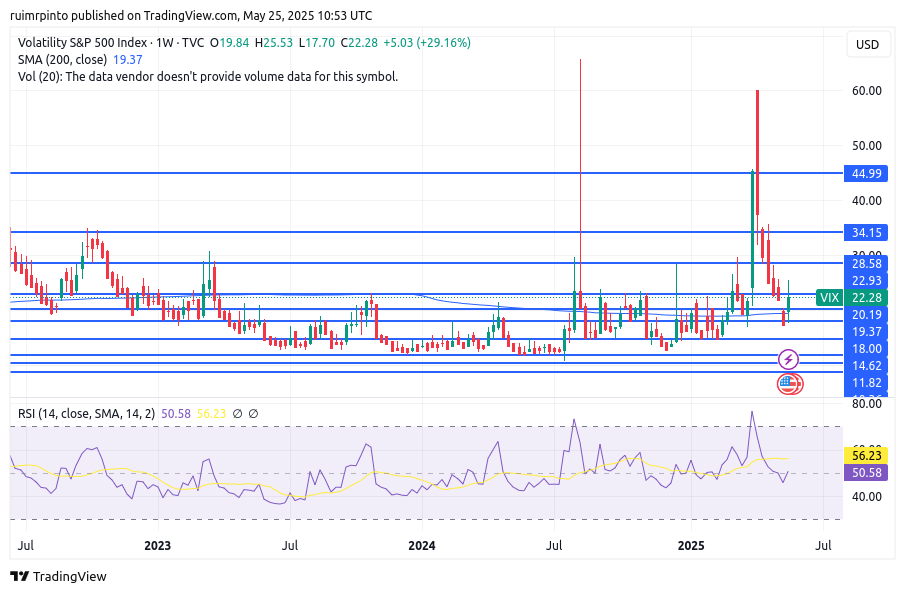

The VIX closed the week at ~22.3, a slight increase which will likely be accompanied by higher risk premiums in the options market. Similarly to previous weeks, it is our opinion that the overall risk in the stock market (high valuations) and uncertainty about the US economy is considerable. Thus, any equity purchases must be strategic!

Comment Section

This week was slightly negative for the stock markets, as a consequence of long-term yields creeping up. The US credit rating downgrade didn’t cause any financial panic yet.

On a different note, the US government passed their “One, Big, Beautiful Bill” through the house of representatives. This bill, if approved, will represent considerable tax cuts for Americans. The next step is the congress approval (or not) of the the bill. The bill is too big to analyze here, but here are some of the consequences:

This week, the S&P Global Manufacturing and Services PMI numbers were released – the figures were slightly above 50 for the US, indicating a slight growth in business activity. However, in the EU, PMI numbers came below 50, signalling business contraction.

Year-over-year inflation rate numbers came at 3.5% in the UK, 1.7% in Canada, and 3.6% in Japan. Overall, inflation is under control, and monetary base expansion has not been observed.

On the trade war front, attentions turn to the US-EU relationships. Trump now threatens a 50% tariff on the EU! The US imposed a 20% “reciprocal” rate on most EU goods from the 2nd of April, but halved them a week later to allow for trade talks. It has kept 25% import taxes on steel, aluminum and vehicle parts in place and has threatened similar moves on pharmaceuticals, semiconductors and other goods. In the same press conference, Trump said he might add a 25% levy on all Apple and Samsung phones bought by US customers. That would be in place at the end of June, he said. His comments triggered falls in leading US stock indexes and European shares, Associated Press reported.

As more trade tariff agreements are likely put in place, we expect some normality and less pessimism from individuals and businesses. However, some damage to the economic activity was done in April-May and that will be reflected in the next earnings season (Q2 2025). If we had to forecast, we would say this year we will likely see a sideways equity market, with alternating optimism and panic waves. Real economic growth will not be great, and things can turn sour at any moment if a recession is confirmed towards the third or fourth quarters of 2025.

Have a nice weekend, and good luck!!!

Sources:

https://www.tradingeconomics.com

https://www.bbc.com/news/articles/c5yg0kgg2njo

https://www.whitehouse.gov/articles/2025/05/what-they-are-saying-one-big-beautiful-bill-clears-house