Market Recap: 26-30 May 2025

Financial Markets

US Stock Market

This week the S&P500 and the NASDAQ 100 recovered slightly, gaining 1.9% and 2%, respectively. The main indices are around support and slightly above the 200-day moving average. The small cap index (Russel 2000) was up by 1.2% and is also around support. Trading volumes were average.

COMMODITIES

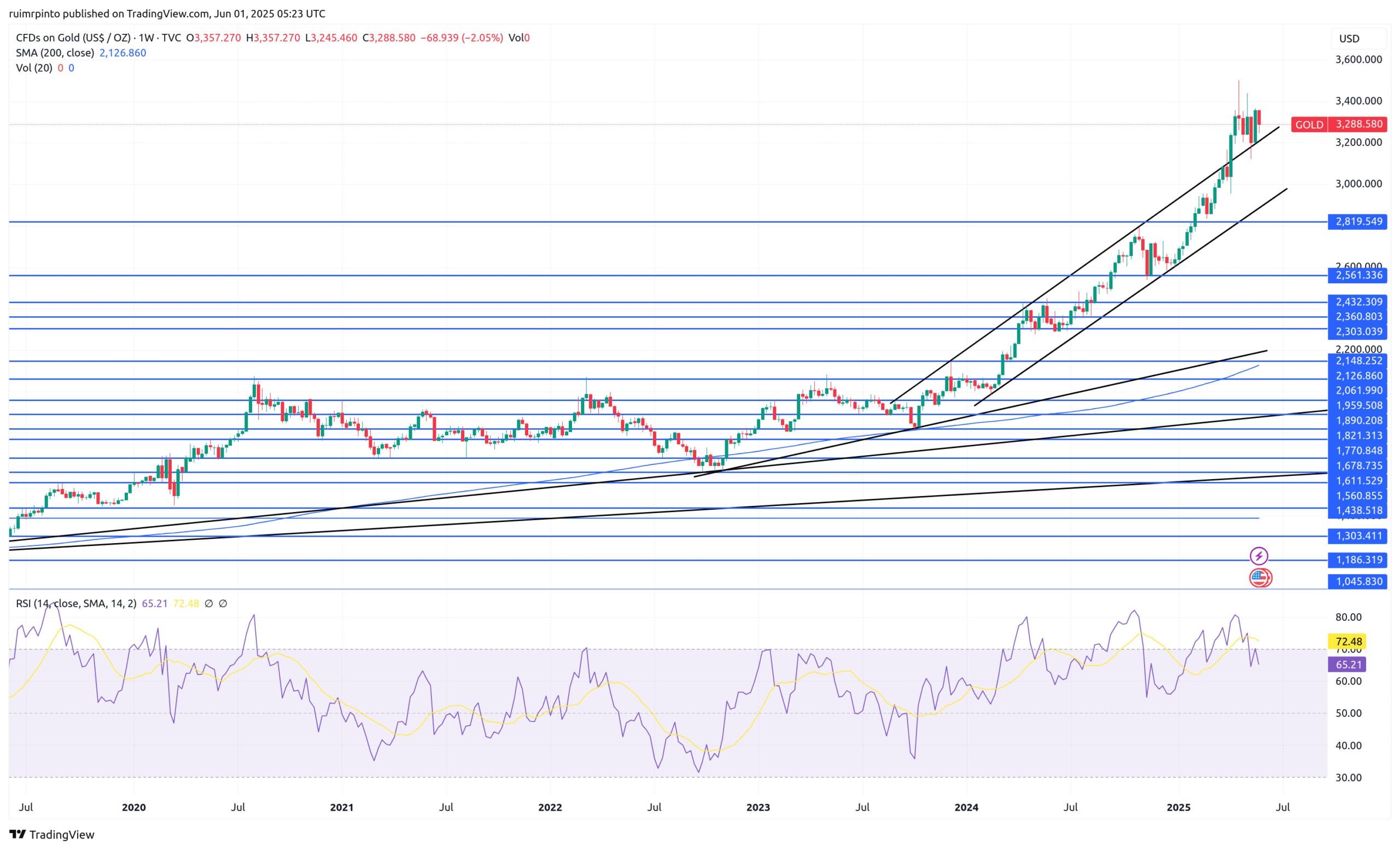

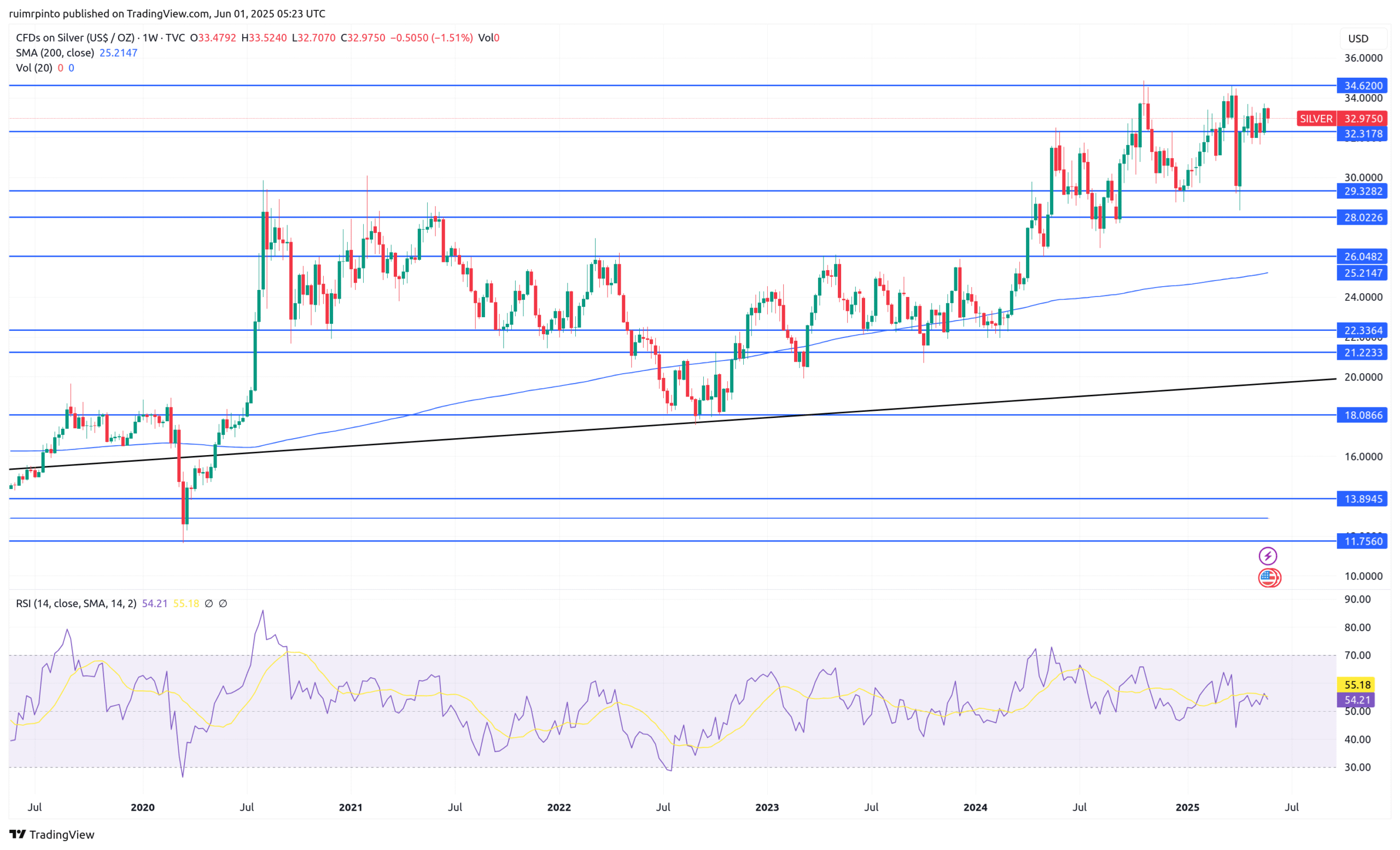

Precious metals held this week. Gold and silver were down by 2.1% and 1.5%, respectively. Gold lost its upward momentum and is either consolidating or getting ready to correct – if a correction occurs, the first target should be around 3000$/oz. Silver closed at ~33$/oz, and continues on a lateral trend – it will likely trade in the range 29-35$/oz in the near future.

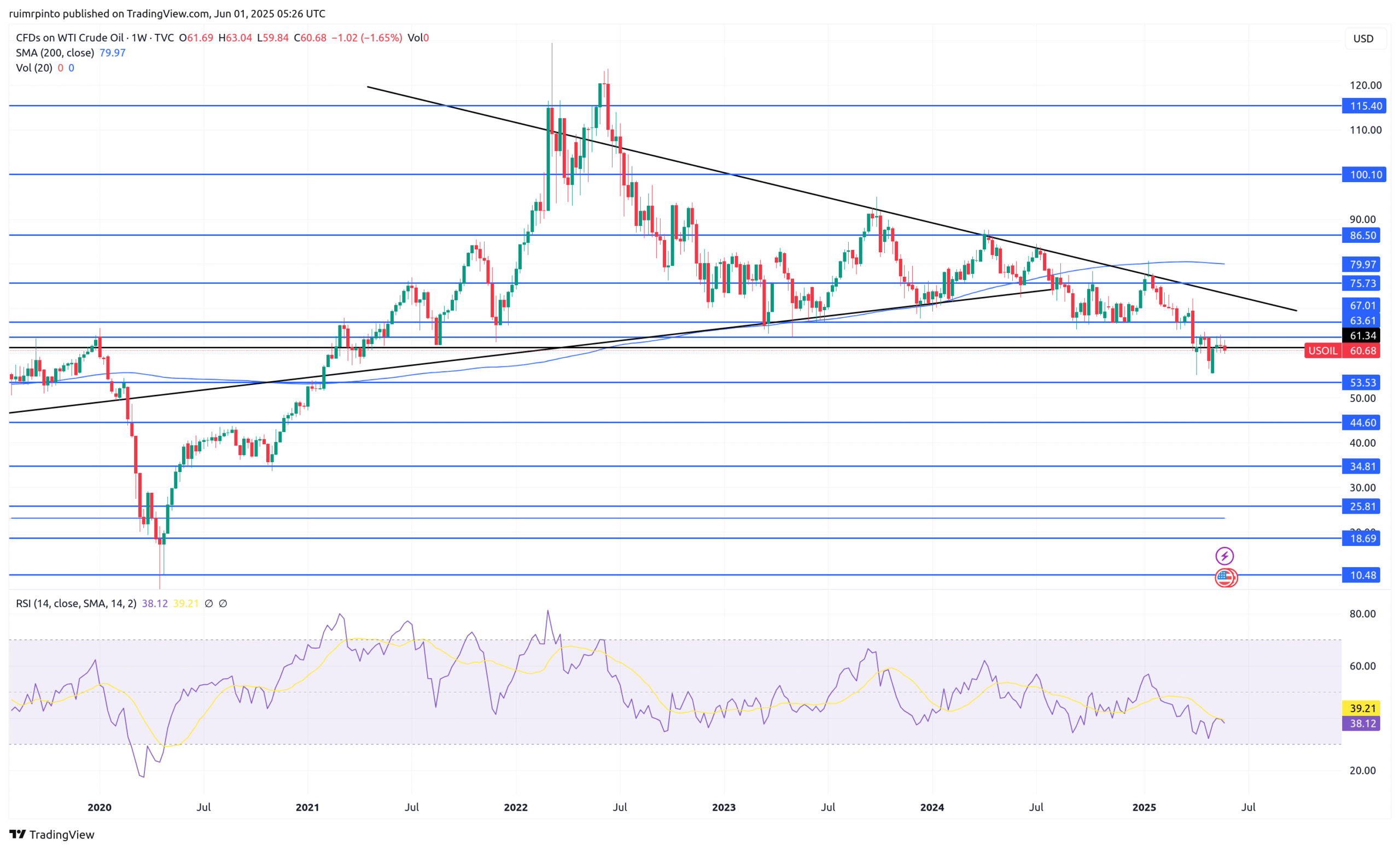

WTI crude oil fell slightly this week, closing at 60.7$/bbl. The trading range in the near future seems to be 54-64$/bbl, but oil may be subject to large swings due to wider macroeconomic developments or major oil producer announcements.

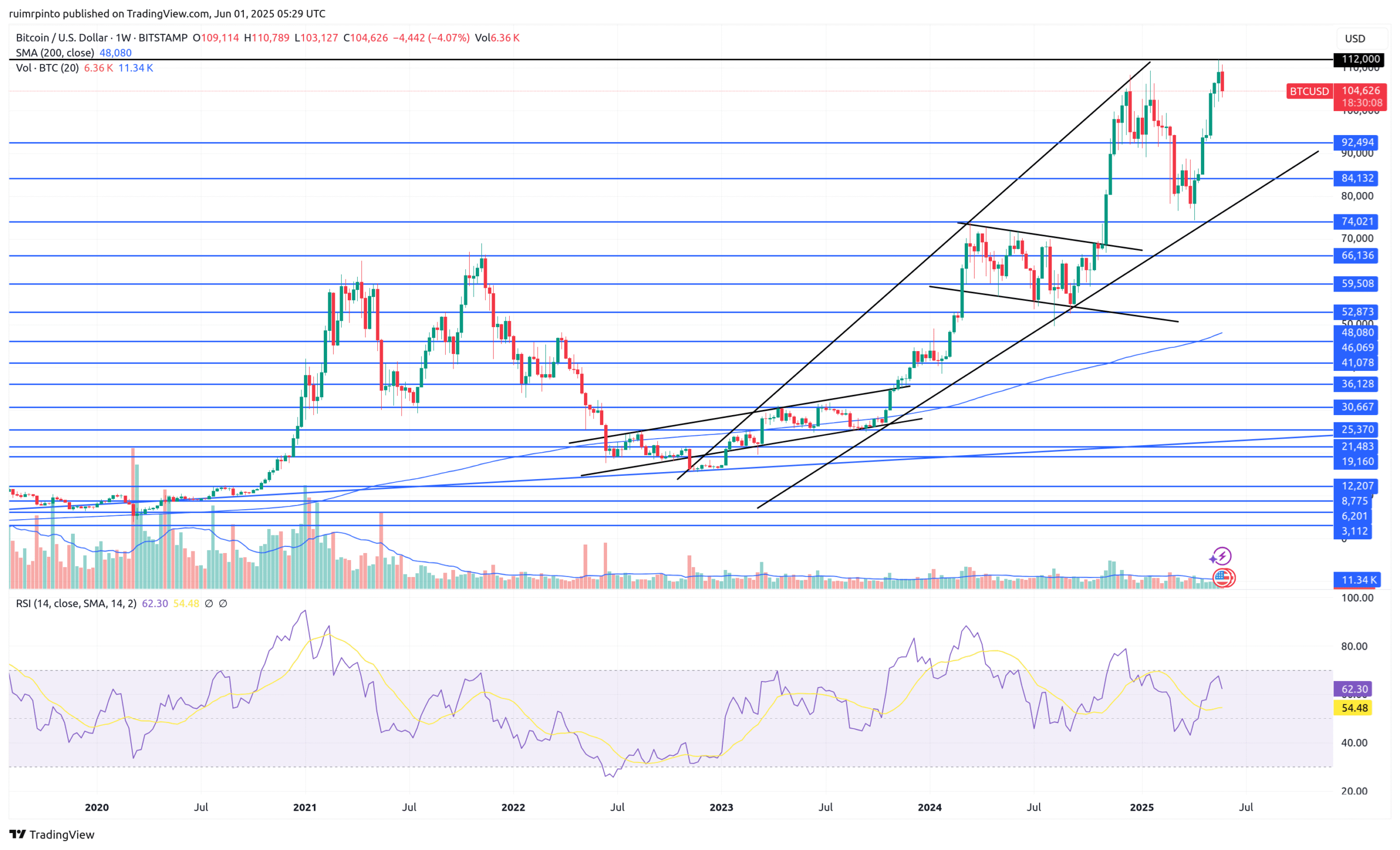

Bitcoin corrected 4.1% after reaching a new all-time-high last week (112k$). If it continues falling, the next target is likely around 102k$. For the next weeks, the key resistance and support levels on Bitcoin, are 112k$ and 92k$, respectively.

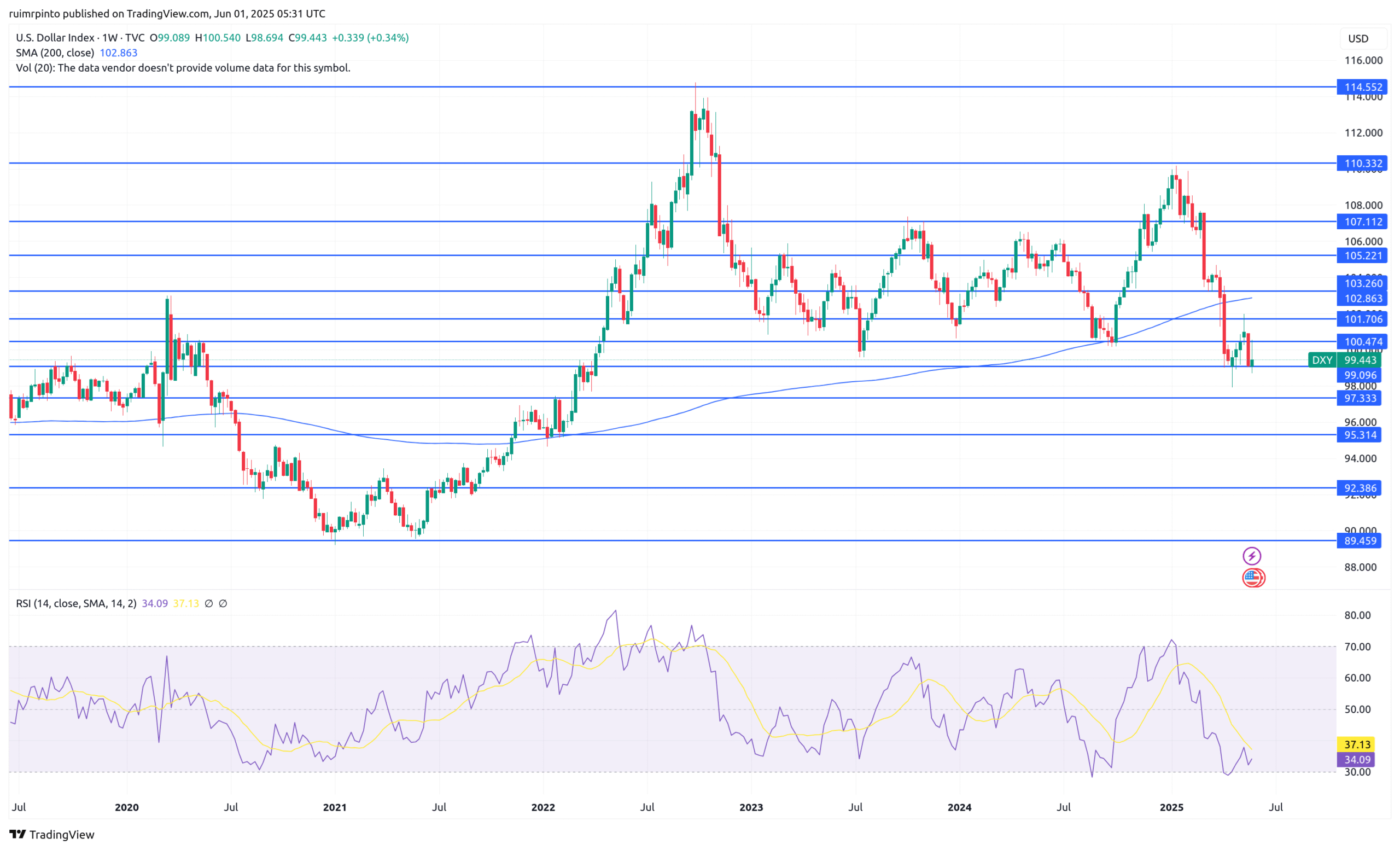

US DOLLAR, MONEY SUPPLY

The relative strength of the US dollar (DXY) was essentially unchanged for the week. The EUR/USD is around 1.135$, the GBP/USD is at 1.346$, and the USD/JPY is at 144.03 JPY.

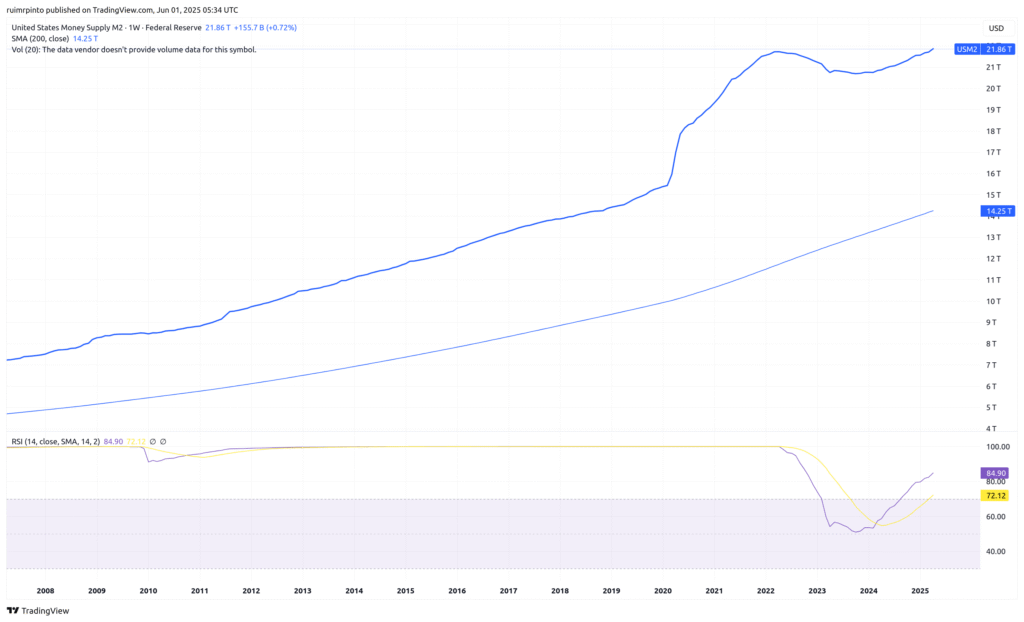

US M2 money supply at the date of 28th April 2025 was up by 0.72%, showing a slow increase over the previous month – credit institutions didn’t stop lending so far. If the money supply was going down, it would be another warning sign for the economy and equities.

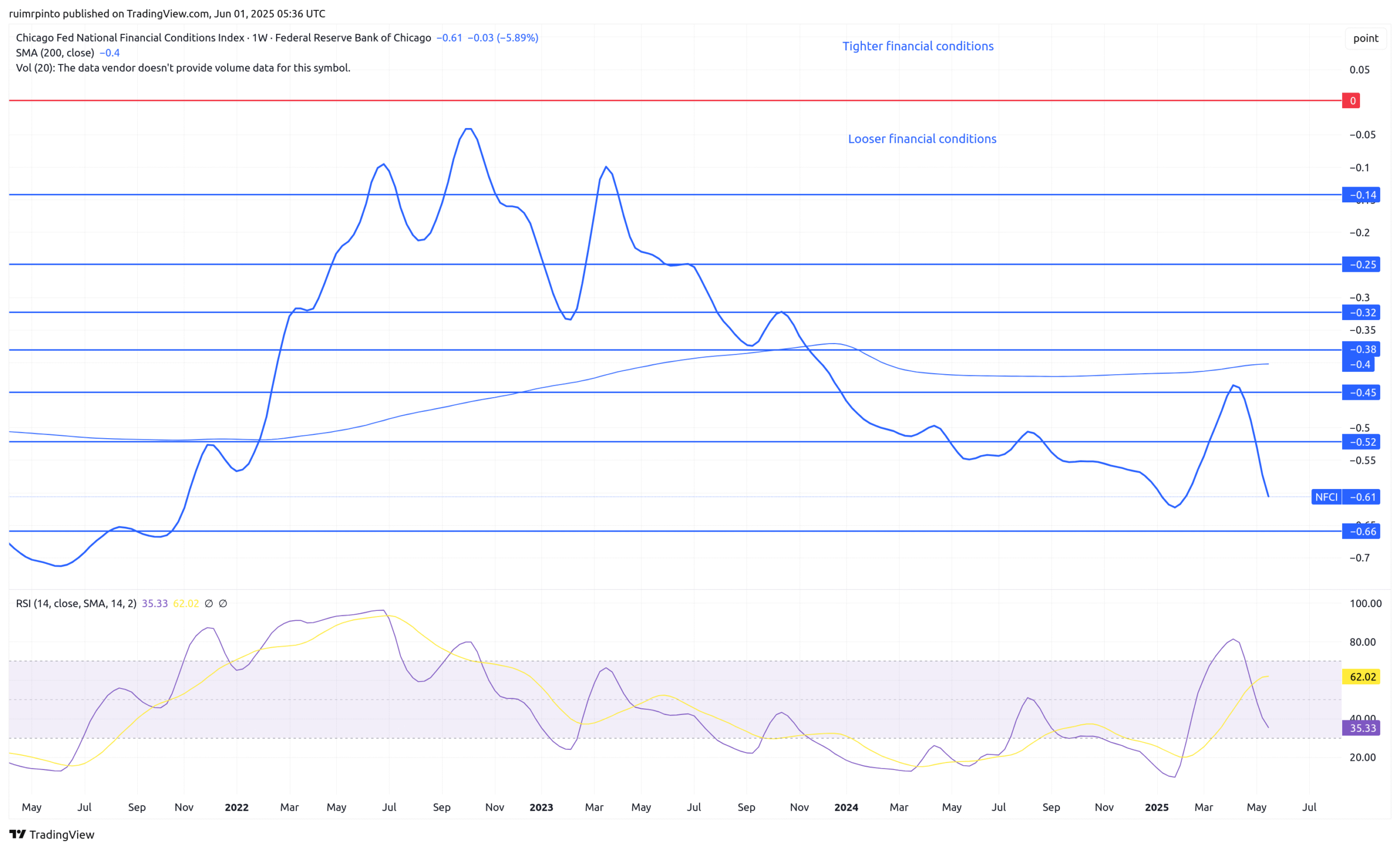

The national financial conditions index (NFCI) released on 19th May 2025 loosened by 5.9%. Note that this indicator is delayed by two weeks. Positive numbers in the NFCI mean tighter financial conditions, while negative numbers indicate looser financial conditions.

BONDS AND OPTIONS

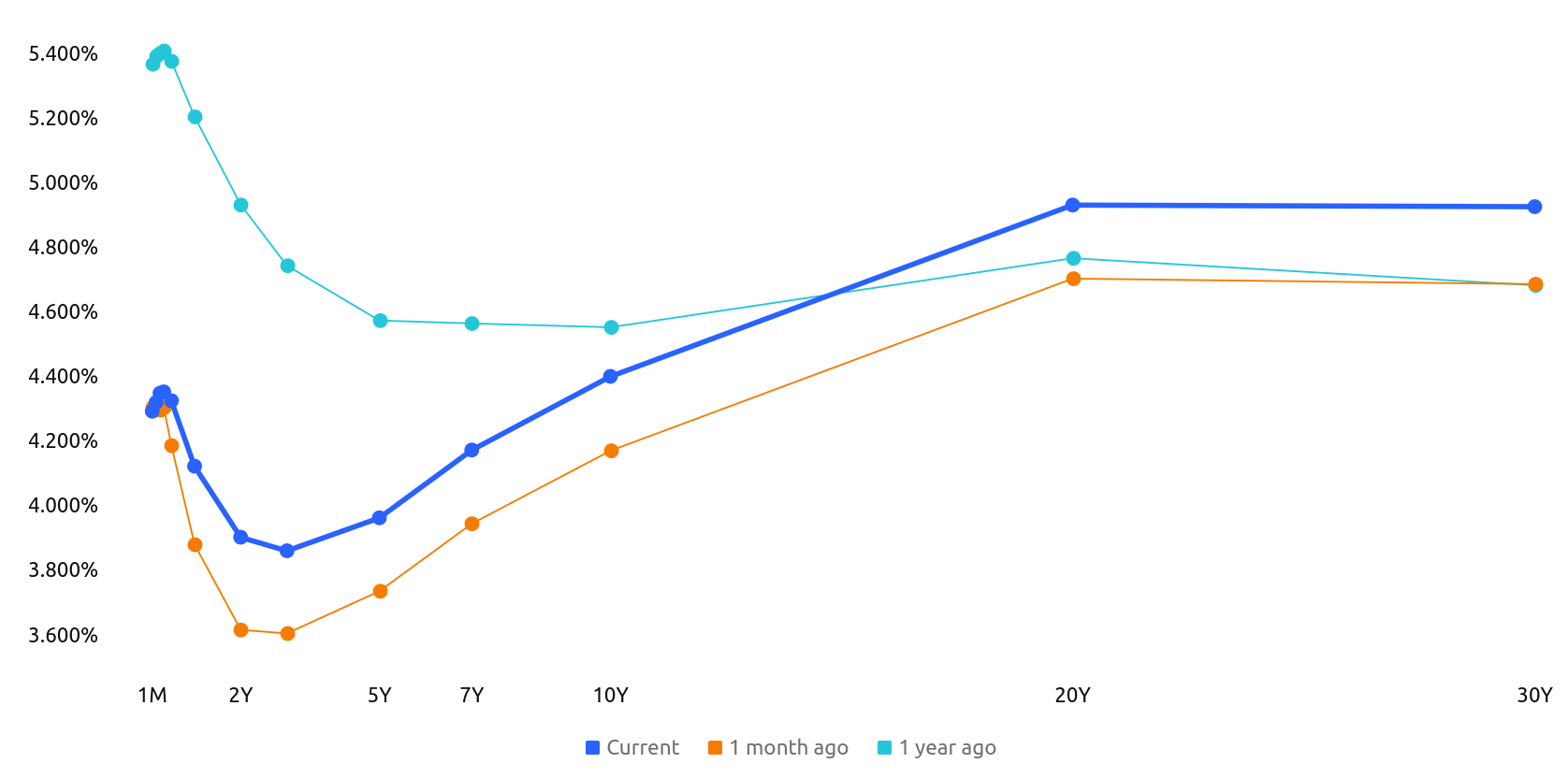

US bond yields fell slightly this week. Yields now sit at 3.900% for the 2-year and 4.398% for the 10-year. As you can see, the yield curve has uninverted since a year ago, and lower yields are expected in the next few years, likely as a consequence of a recession and interest rate cuts. However, long-term growth and inflation expectations are about 5%.

The VIX closed the week at ~18.6, a slight decrease relative to the previous period. Risk premiums in the options market are moderate. Similarly to previous weeks, it is our opinion that the overall risk in the stock market (high valuations in the big caps) and uncertainty about the US and worldwide economy is considerable. Thus, any equity purchases must be strategic and opportunistic!

Comment Section

The US equity markets are holding for the moment and financial conditions are not tight. A market lateralization could continue for the next few weeks.

The Trump trade war drama was quite active this week. On Wednesday, a US trade court halted the tariffs. But on Thursday, the United States Court of Appeals for the Federal Circuit in Washington said it was pausing the lower court’s ruling to consider the government’s appeal, and ordered the plaintiffs in the cases to respond by June 5 and the administration by June 9 – Trump’s tariffs remain in effect, for now.

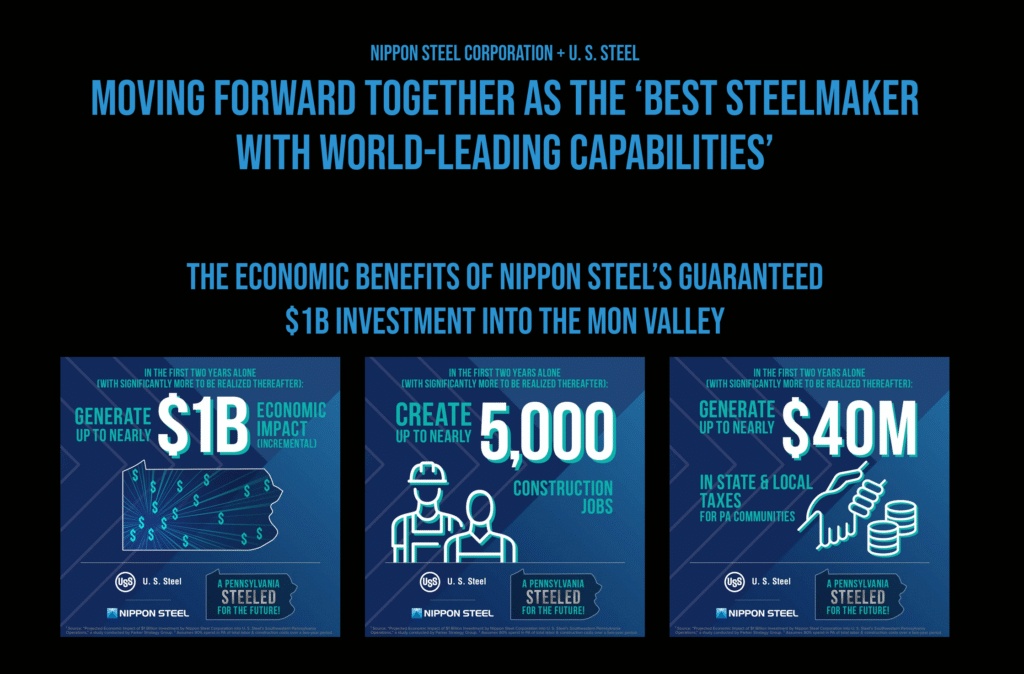

The Unites States Steel Corporation (USS) and Nippon Steel deal is on the news again. This deal is kind of delicate as if falls under a strategic sector for the US administration (raw materials for the re-industrialization of America). Although the deal has been announced as a positive for the US, we didn’t analyze it in detail at this point and will not comment further .

The increase on steel tariffs (to 50%) by the US is not helping the negotiations with the EU, which ‘strongly’ regrets US plan to double steel tariffs.

In the US, GDP growth rate (estimate) is at around -0.2% quarter-over-quarter, showing a contraction in the economy. Imports of goods and services soared 42.6% as businesses and consumers rushed to stockpile goods in anticipation of higher prices following a series of tariff announcements by the Trump administration. Additionally, consumer spending growth slowed to 1.2%, the weakest pace since Q2 2023, while federal government spending dropped 4.6%, the steepest decline since Q1 2022. In contrast, fixed investment rose by 7.8%, the strongest gain since mid-2023, and exports increased 2.4%. PCE price index came at 0.1% month-over-month and 2.1% year-over-year.

This week, the France year-over-year (YoY) inflation rate came at 0.7%, lower than anticipated, while in Spain it sits at 1.7% and in Germany it is around 2.1%. In Germany, unemployment is stable at around 6.3%.

As we have been saying, some damage to the economic activity was done in April-May 2025 and that will be reflected in the next earnings season (Q2 2025). If we had to forecast, we would say this year we will likely see a sideways equity market, with alternating waves of optimism and pessimism. Real economic growth will not be great, and things can turn sour at any moment if a recession is confirmed towards the third or fourth quarters of 2025.

Have a nice weekend, and good luck!!!