Market Recap: 12-16 May 2025

Financial Markets

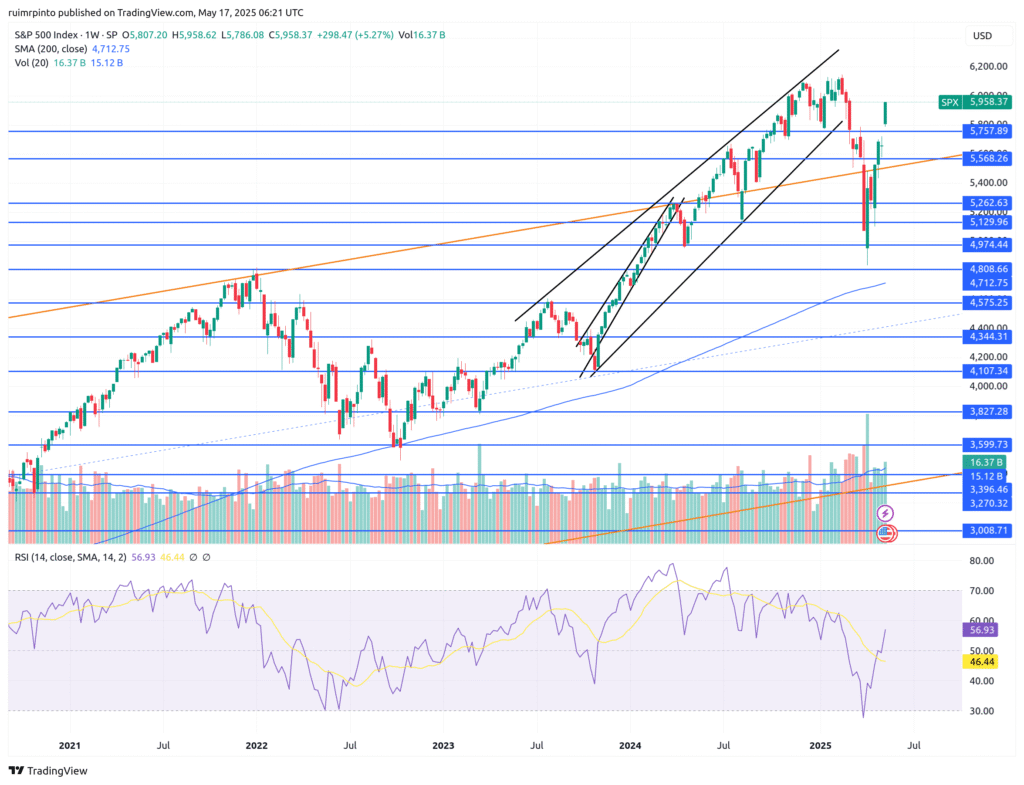

US Stock Market

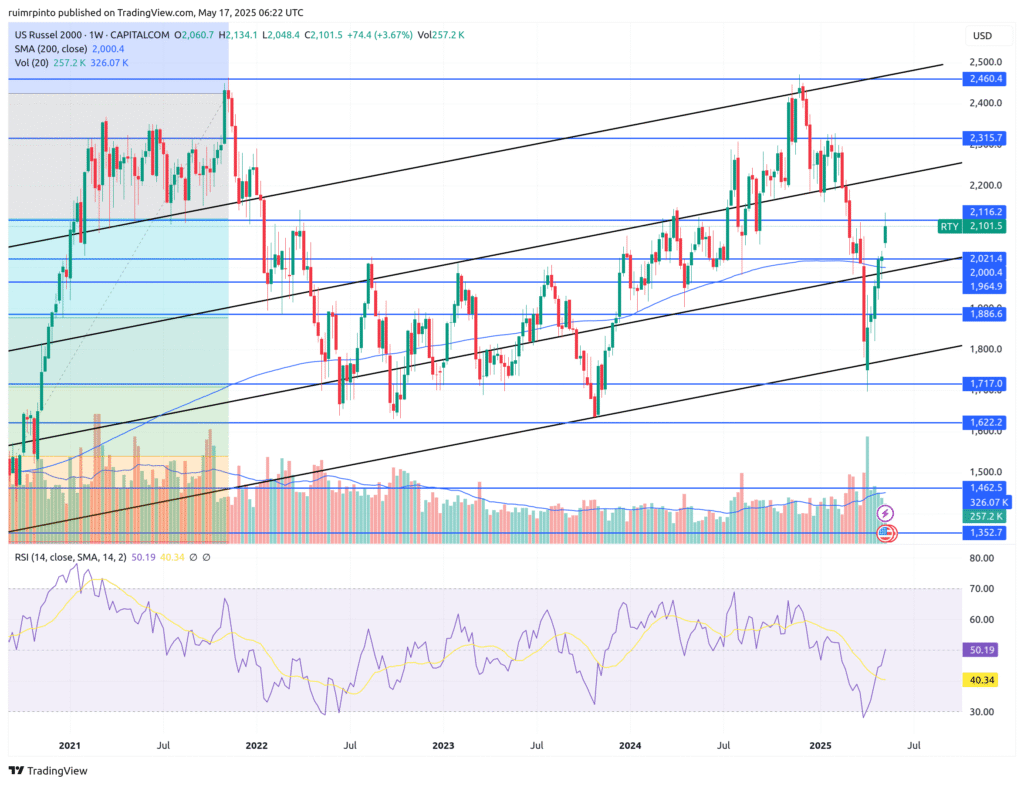

This week the S&P500 and the NASDAQ 100 gaped higher and gained 5.3% and 6.8%, respectively. The small cap index (Russel 2000) was up by 3.7% and should stall around current levels. Trading volumes were average.

COMMODITIES

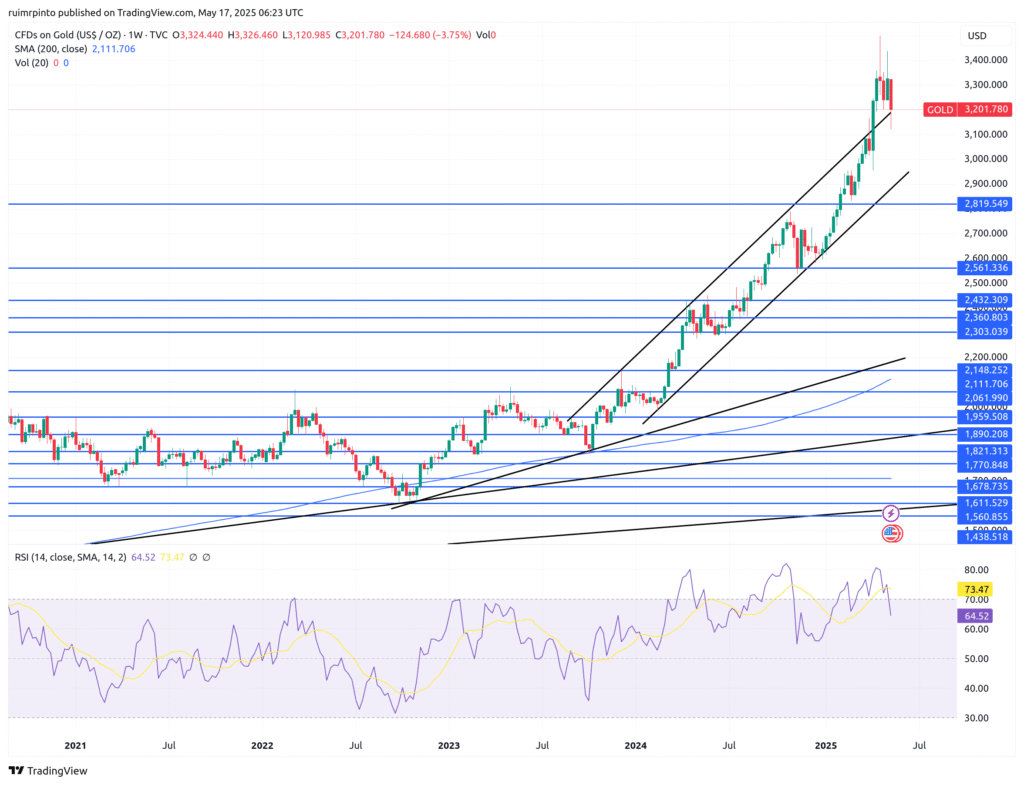

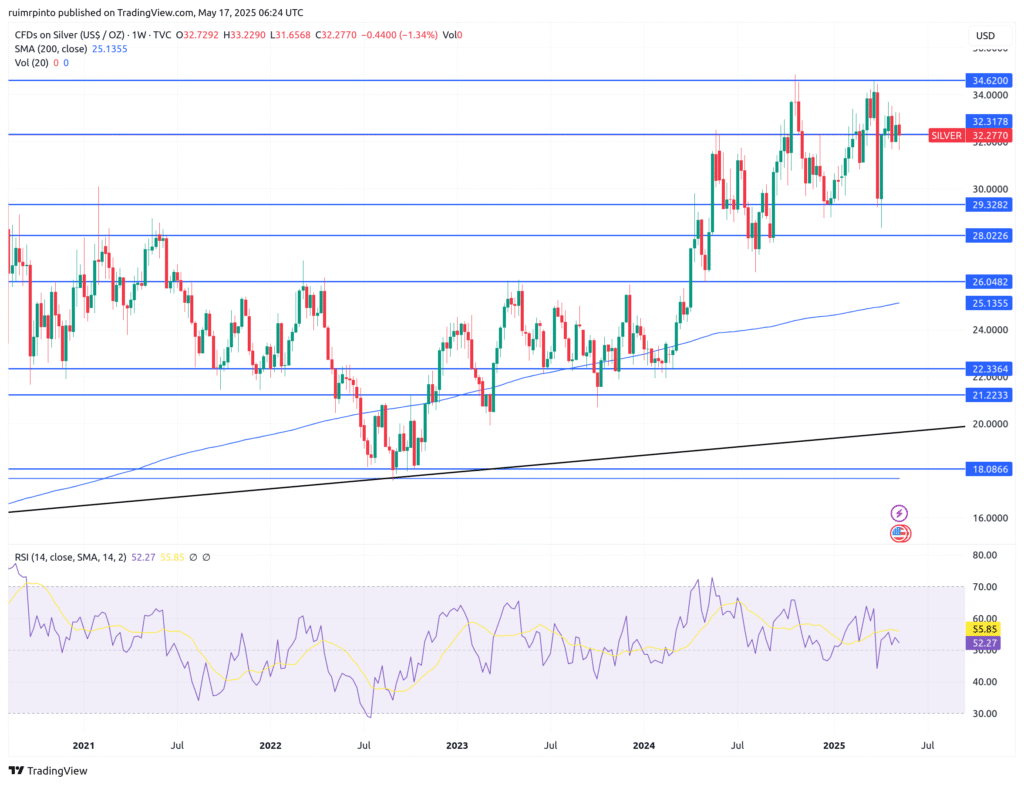

As equities rallied, precious metals lost a bit of appeal this week. Gold and silver were down by 3.8% and 1.3%, respectively. In the near future gold may consolidate around current levels, at the top-end of the previous trend. Silver closed at ~32.3$/oz, and continues on a lateral trend – it seems stuck in the range 29-34$/oz.

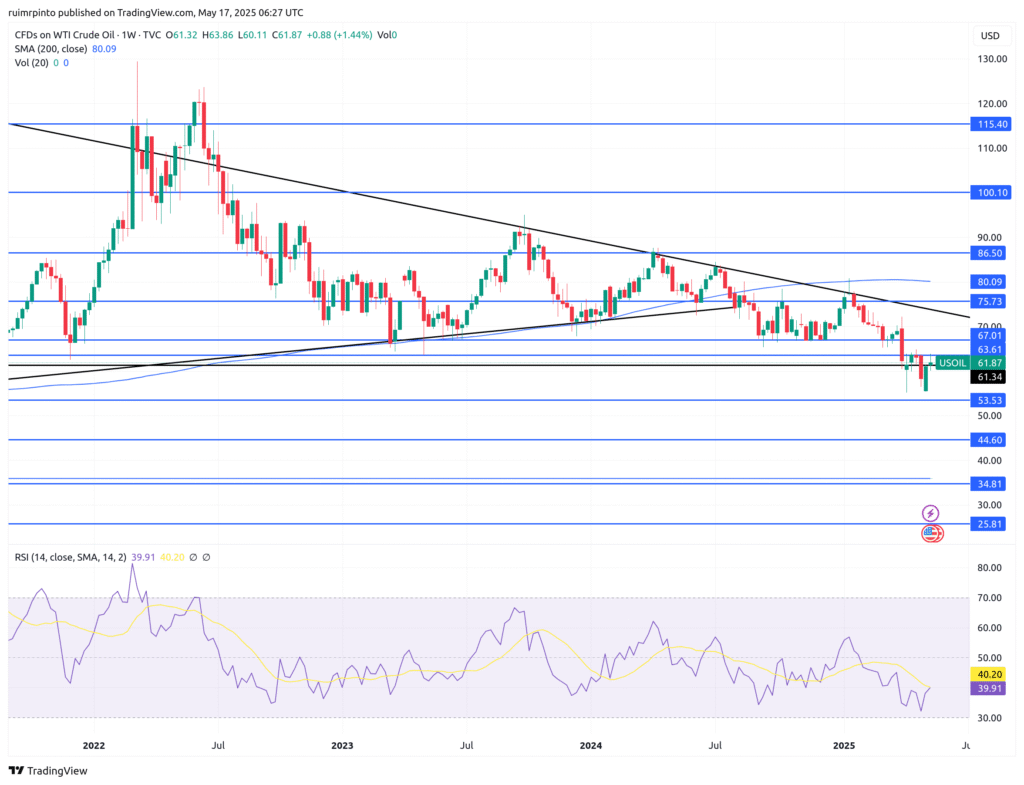

WTI crude oil was little changed this week, closing at 61.9$/bbl. The trading range for the near future seems to be 54-64$/bbl, but oil may be subject to large swings due to wider macroeconomic developments or major oil producer announcements.

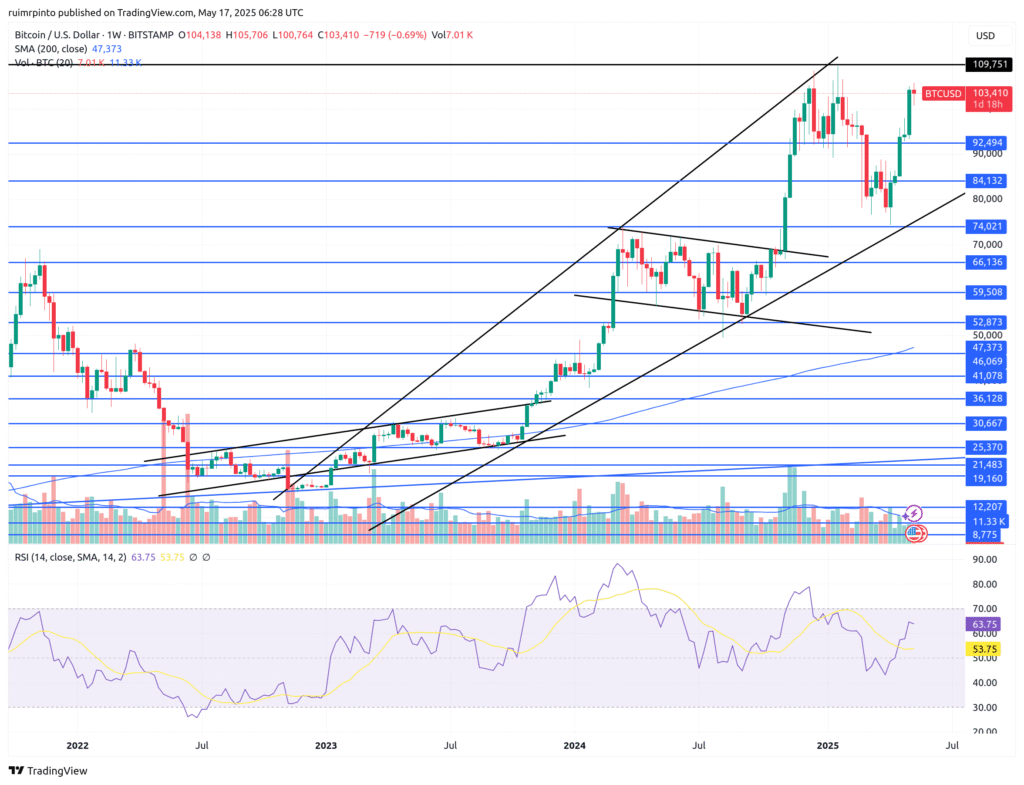

Bitcoin was little changed (-0.7%) and is still close to all-time-highs. The key resistance and support levels on Bitcoin, for the short term, are 109k$ and 92k$, respectively.

US DOLLAR, MONEY SUPPLY

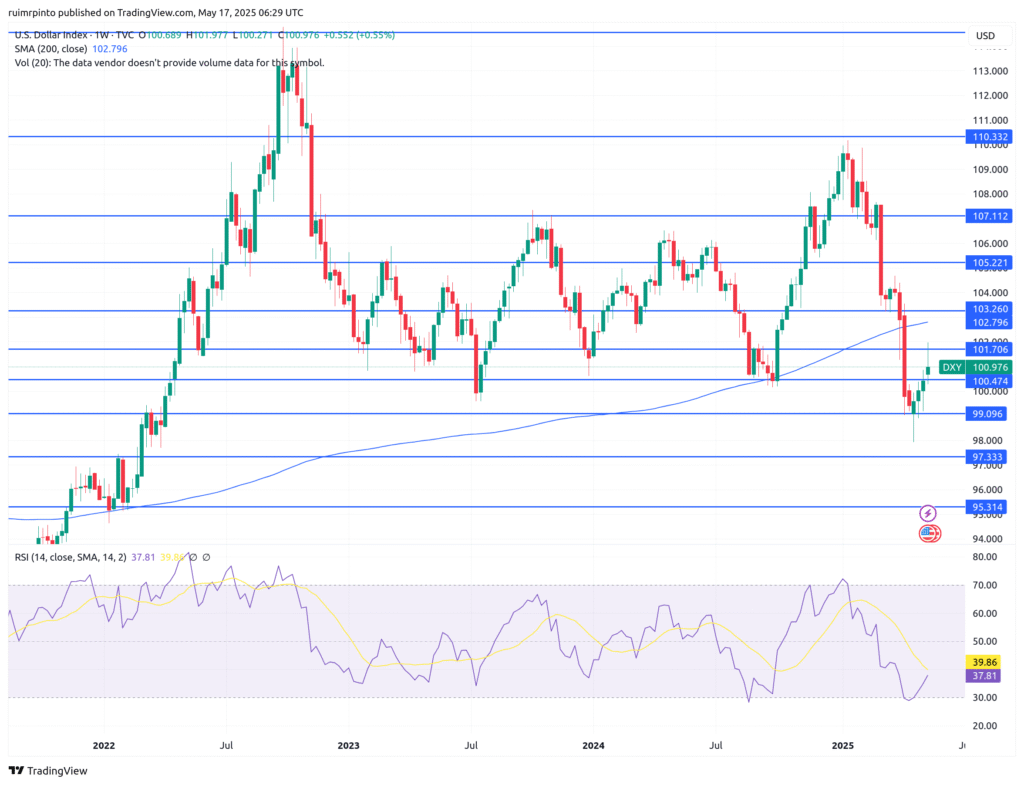

The relative strength of the US dollar (DXY) had a big swing up during the week but closed at ~101, slightly up from the previous week. The EUR/USD is around 1.116$, the GBP/USD is at 1.327$, and the USD/JPY is at 145.69 JPY.

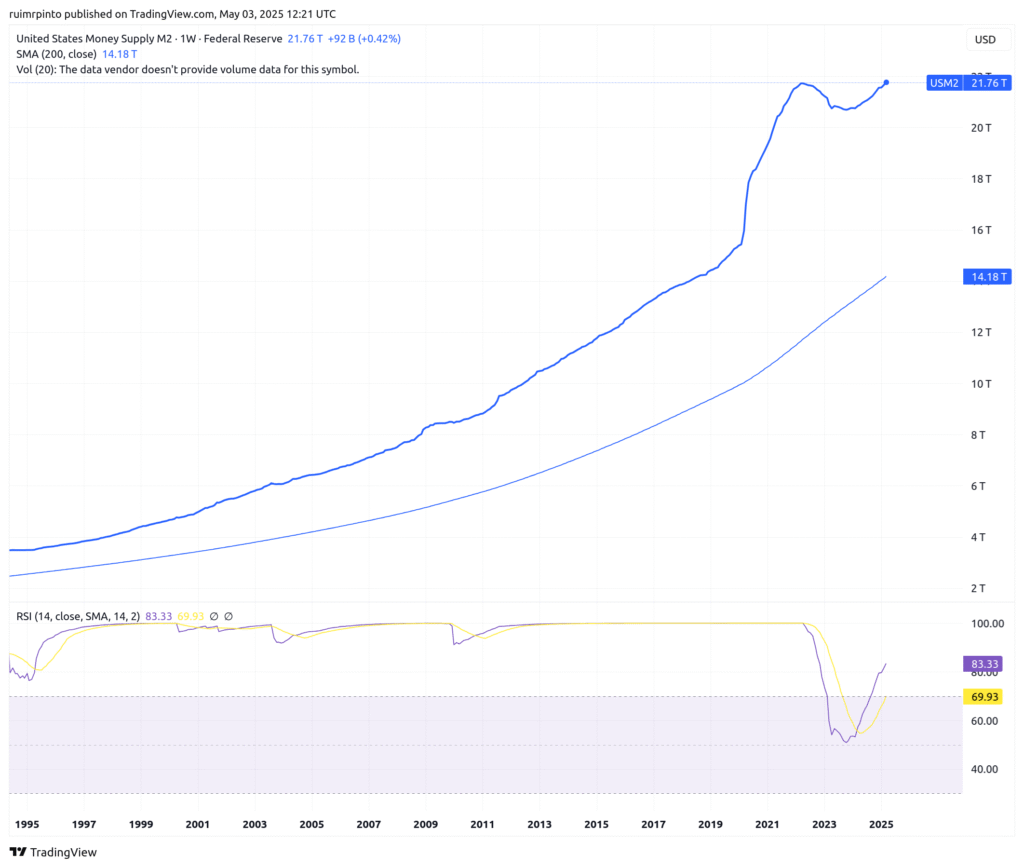

US M2 money supply at the date of 31st March 2025 was up by 0.4%, showing a slow increase over the previous month. If the money supply was going down, it would be another warning sign for the economy and equities.

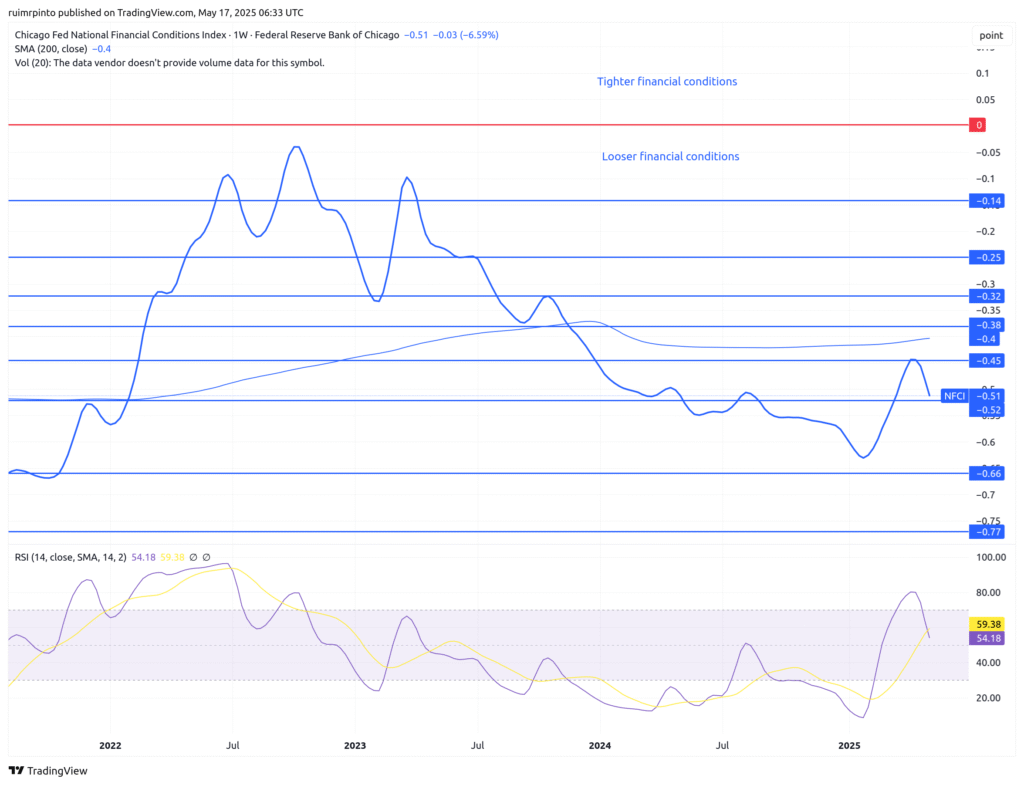

The national financial conditions index (NFCI) released on 5th May 2025 loosened by 6.6%. Note that this indicator is delayed by two weeks. Positive numbers in the NFCI mean tighter financial conditions, while negative numbers indicate looser financial conditions.

BONDS AND OPTIONS

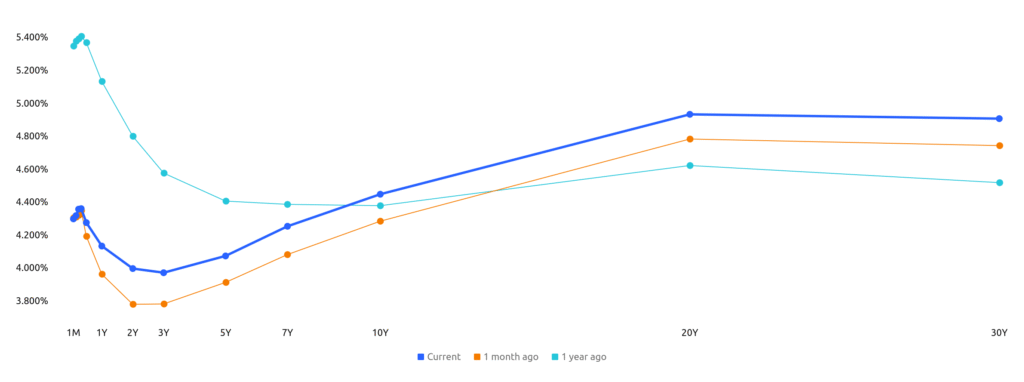

US bond yields rose slightly this week. Yields now sit at 3.993% for the 2-year and 4.445% for the 10-year. As you can see, the yield curve has uninverted since a year ago, and lower yields are expected in the next few years, likely as a consequence of a recession and interest rate cuts. However, long-term growth and inflation expectations are about 4.8%.

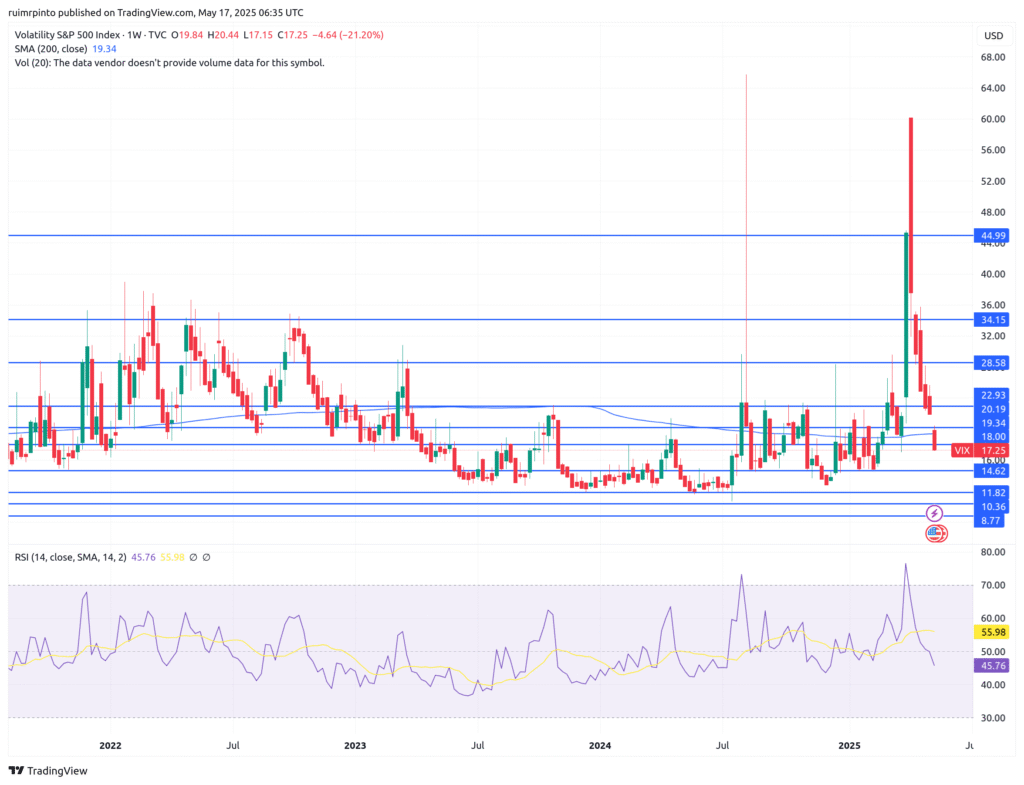

The VIX closed the week at ~17.3, showing a continuing decrease in risk perception in the options market. Soon, we will enter again into complacency territory. In our opinion, the overall risk in the stock market (high valuations) and uncertainty about the US economy is still too high to be fully allocated to stocks on the long side – it’s better to have some liquid reserves. Regarding options, at this point, we wouldn’t recommend selling puts unless you are really comfortable buying the underlying asset (using cash-secured puts)!

Comment Section

This week was highly positive for the stock markets, due to the trade tariff halt between the US and China. Later in the week, positive inflation numbers were released.

On Tuesday, the US Consumer Price Index (CPI) numbers came at 0.2% month-over-month in April 2025, following a 0.1% decline in March and falling short of market expectations for a 0.3% increase. The year-over-year number came at 2.3%, also lower than anticipated. For now, inflation numbers remain “well anchored”, as Powell would say.

More surprisingly, US producer prices fell by 0.5% in April 2025, following a revised flat reading in March and defying market expectations of a 0.2% increase. This was the first decline in the PPI since October 2023 and the sharpest drop since April 2020, during the early aftermath of the COVID-19 outbreak. The decline was largely driven by a 0.7% fall in service costs.

The University of Michigan consumer sentiment for the US dropped sharply to 50.8 in May 2025, the fifth consecutive monthly decline. Current assessments of personal finances sank nearly 10% on the basis of weakening incomes. Tariffs were spontaneously mentioned by nearly three-quarters of consumers, up from almost 60% in April; uncertainty over trade policy continues to dominate consumers’ thinking about the economy. On the price front, inflation expectations for the year ahead surged to 7.3%…

After last week’s trade deal with the UK, this week, during the Geneva summit, the U.S. agreed to cut the extra tariffs it imposed on Chinese imports last month to 30% from 145% for the next 90 days, while China committed to cutting duties on U.S. imports to 10% from 125%. Finally bots sides are collaborating and ending the theatrical situation of escalating trade tariffs which would bring worldwide trade to a halt.

Regarding the peace negotiations between Ukraine and Russia, in Istanbul, it was mostly unsuccessful, with no ceasefire agreement and there were no signs of a major breakthrough – a Ukrainian source said that the Russian delegation demanded that Kyiv give up land under its control. Neither Ukrainian President Volodymyr Zelensky or Russian President Vladimir Putin attended the meeting.

Finally, to end the week, Moody’s downgraded the U.S. sovereign credit rating on Friday due to concerns about the nation’s $36 trillion debt pile, in a move that could complicate President Donald Trump’s efforts to cut taxes and send ripples through global markets. Moody’s first gave the United States its pristine “Aaa” rating in 1919 and is the last of the three major credit agencies to downgrade it. We wouldn’t worry excessively about this credit downgrade as treasuries remain a highly liquid asset – who trusts credit agencies anyways? They are either too late, or biased…

As more trade tariff agreements are likely put in place, we expect some normality and less pessimism from individuals and businesses. However, some damage to the economic activity was done in April-May and that will be reflected in the next earnings season (Q2 2025). If we had to forecast, we would say this year we will likely see a sideways equity market, with alternating optimism and panic waves. Real economic growth will not be great, and things can turn sour at any moment if a recession is confirmed towards the third or fourth quarters of 2025.

Have a nice weekend, and good luck!!!

Sources:

https://www.tradingeconomics.com

https://www.reuters.com/markets/us/moodys-downgrades-us-aa1-rating-2025-05-16

https://edition.cnn.com/world/live-news/russia-ukraine-peace-talks-intl-05-16-25