Financial Markets

This week the S&P500 and the NASDAQ 100 held support, gaining 0.5% and 0.3%, respectively. The small cap index (Russel 2000) was up by 1.1%. Trading volumes were average.

Precious metals continued strong this week. Gold reached an all-time-high of 3057$/oz during the week, but receded a bit, closing at 3022$. Silver fell 2.4% after reaching resistance at ~34$/oz.

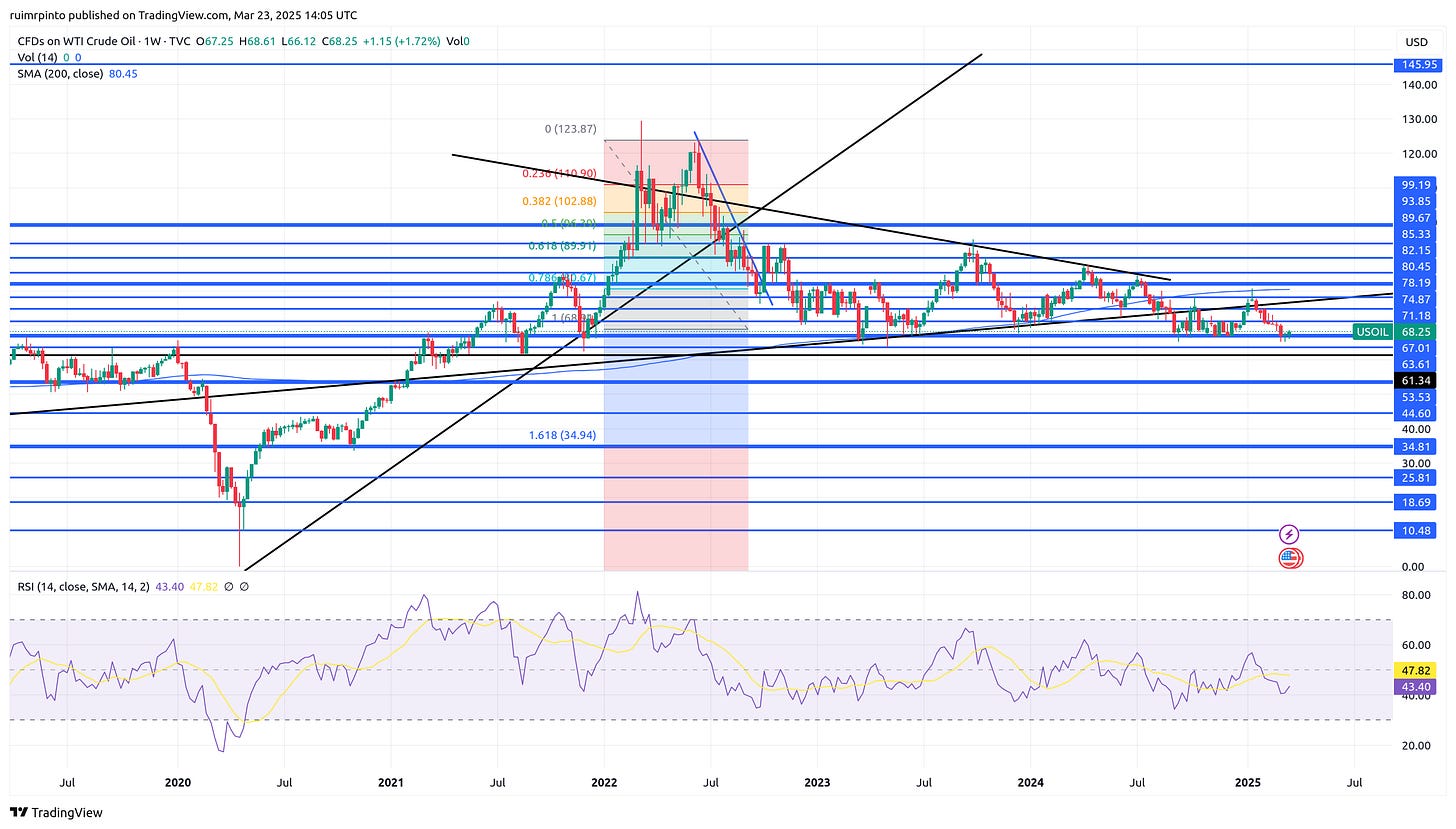

WTI held support and went up by 1.7% to ~68$/bbl. If it continues falling, the next support levels are at 64 and 62$.

Bitcoin recovered 3% after the considerable fall of two weeks ago. The key resistance and support levels on Bitcoin, for the short term, are 92k$ and 72-74k$, respectively.

The relative strength of the US dollar (DXY) increased slightly to 104.1. The EUR/USD is around 1.081$, the GBP/USD is at 1.291$, and the USD/JPY is at 149.29 JPY.

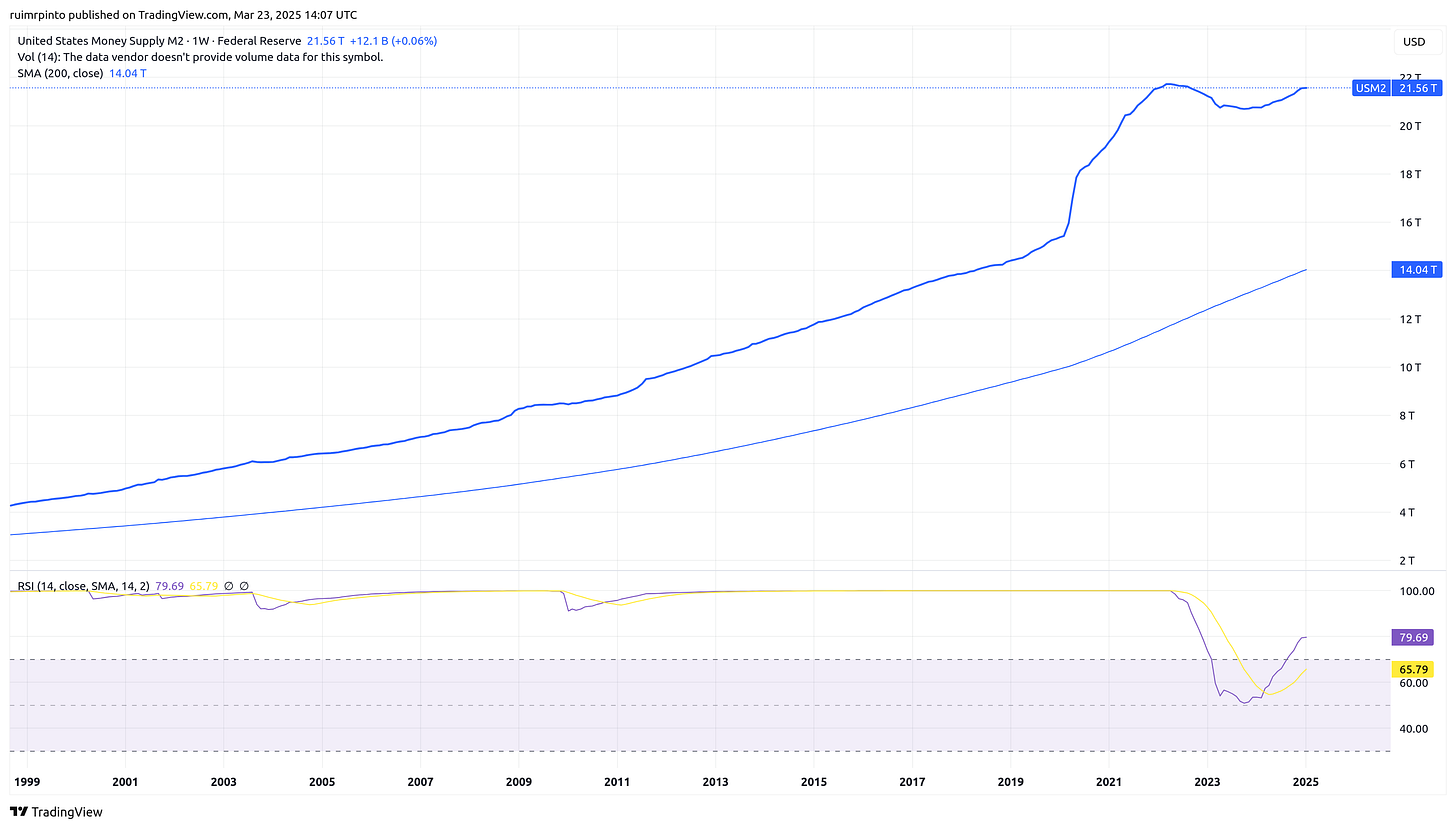

US M2 money supply at the date of 27th January 2025 was flat, which could be a bearish sign, together with the recent selloffs.

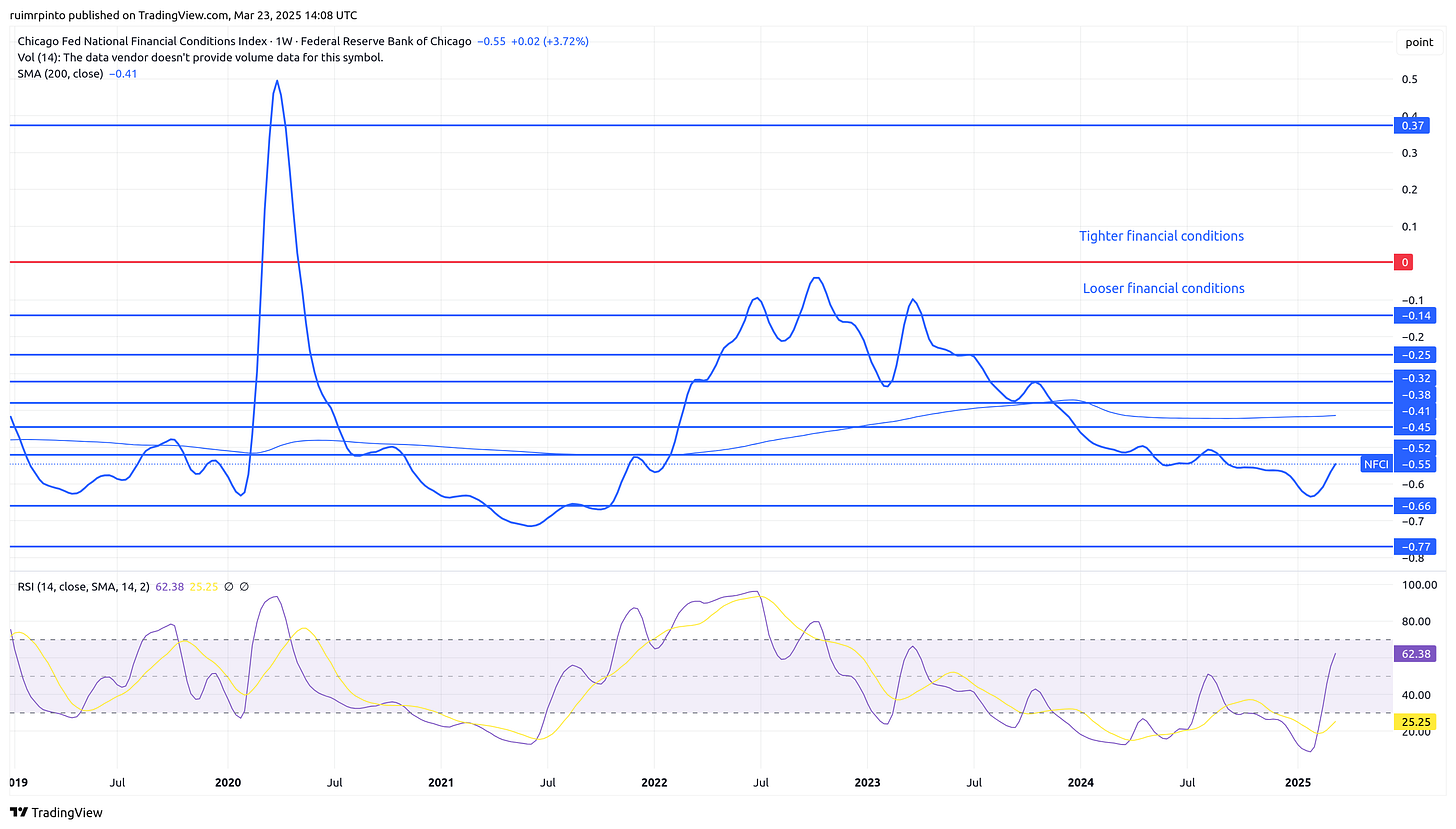

The national financial conditions index (NFCI) for the week of 10th March 2025 tightened by 3.7%, a bearish sign which coincided with the equity market action on previous weeks. Note that this indicator is delayed by a week.

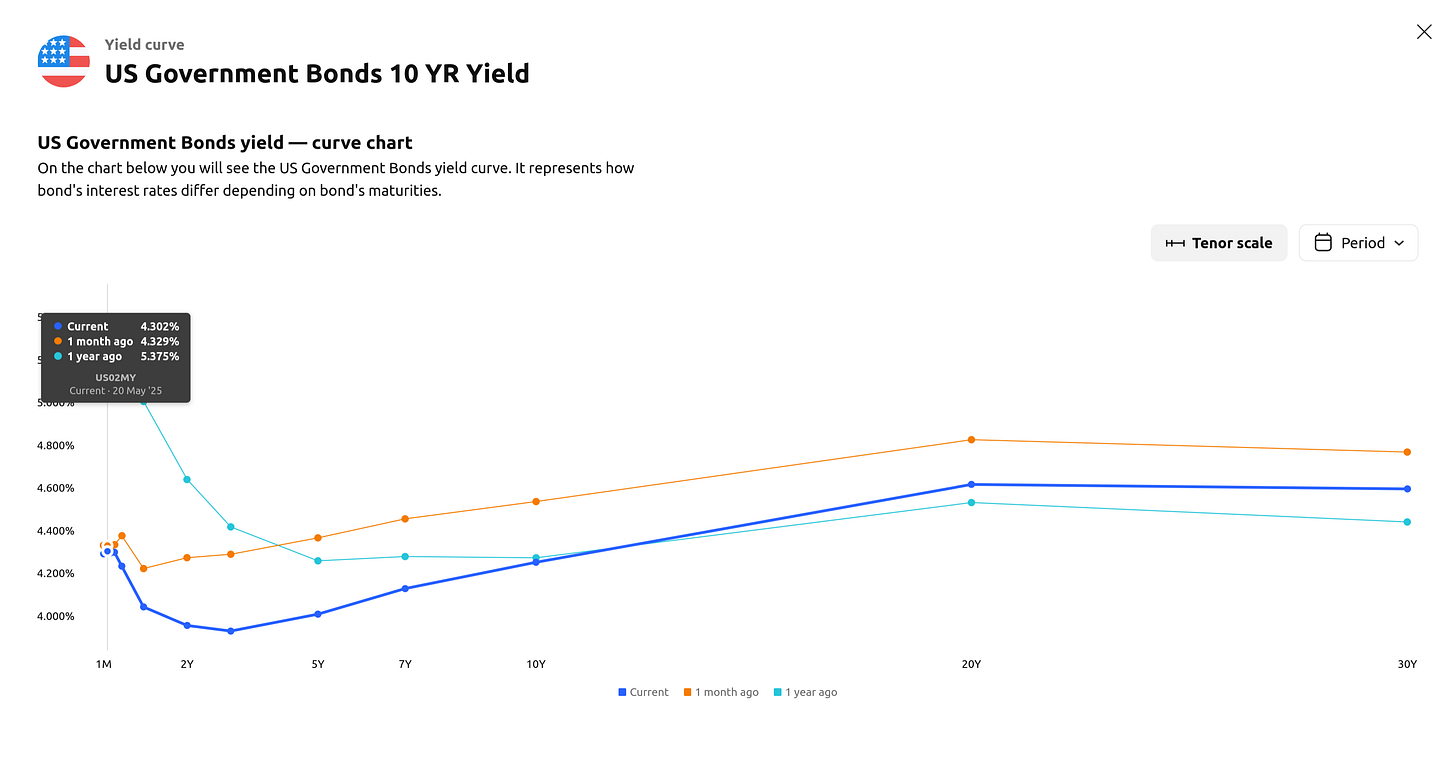

US bond yields fell slightly this week, and now sit at 3.954% for the 2-year and 4.250% for the 10-year. These are below the current FED funds rate, showing that investor expectations favor a decrease in interest rates and lower inflation.

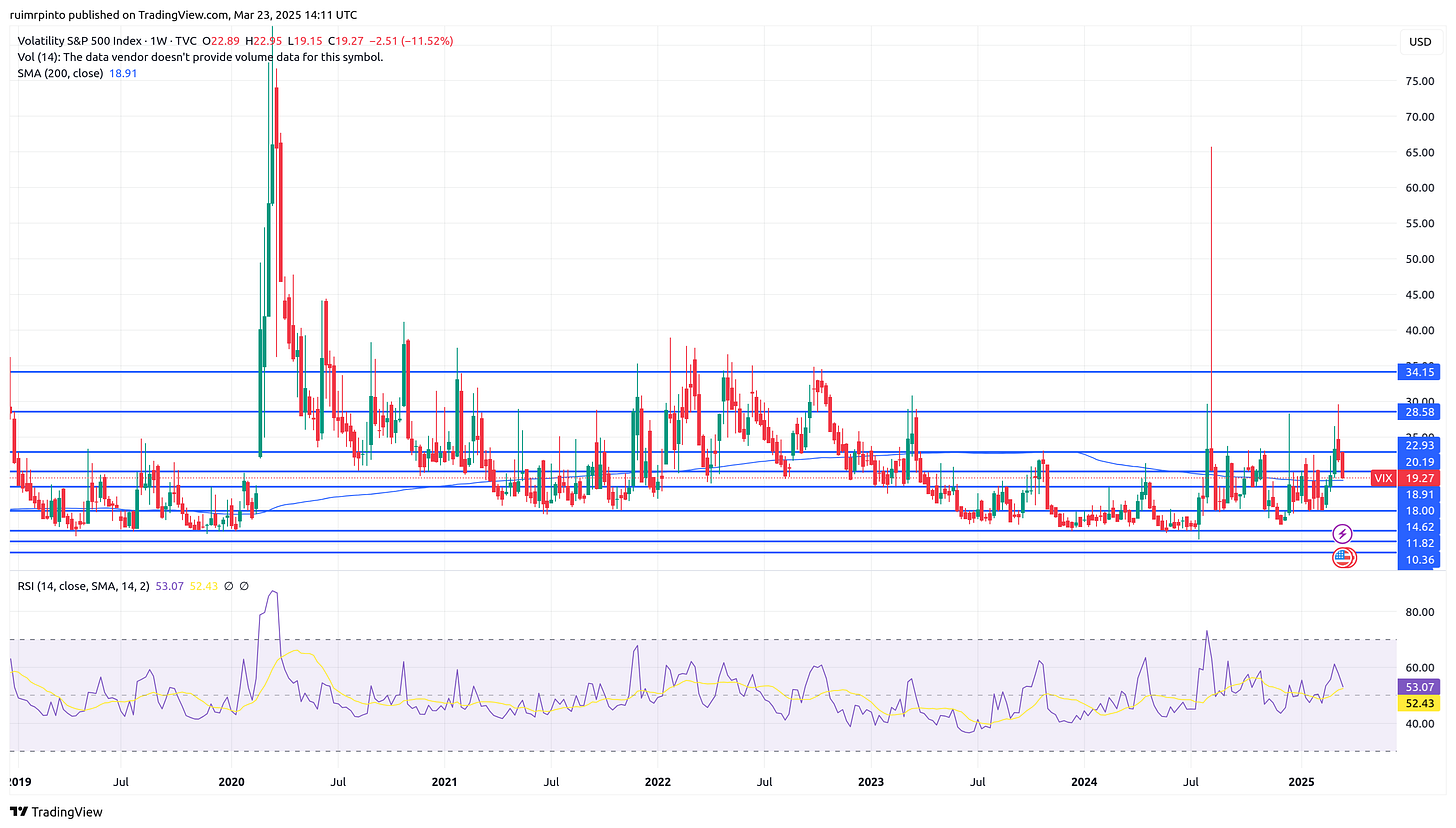

The VIX fell to 19.2, due to the pause in the market selloff and less panic this week. Option sellers need to be strategic and try to sell their put options when the premiums are highest and the risk of assignment lowest (typically after a fall, close to a support level). Currently, risk premium is reasonable.

Comment Section

The US equity markets seem to be holding around current levels, but it might be just a short-term consolidation. The overall sentiment is not clearly bearish, but it is not bullish either. Looking at the current uncertainty, we predict a sideways market for the coming months, unless Trump tariffs are cancelled or other major positive news arise.

This week, the FED kept interest rates unchanged, and the FOMC still predicts only two rate cuts in 2025. The US GDP growth outlook was reduced to 1.7% (it’s like saying…expect no growth in 2025!). During the press conference, Jerome Powell highlighted over and over again the “uncertainty” and the possibility of “transitory” inflation due to the Tariffs/Trade Wars. The FED is waiting for hard data to show further economy deterioration before they get desperate and finally cut rates. On the other hand, Trump has been yelling for some time that interest rates are too high, and will blame the FED for the upcoming recession – it’s a nice play.

Indeed, high interest rates are weighing heavily on the profit margins of many companies, which have been refinancing at 7% or 8% interest rates instead of 3% or 4%, for example. Going from a low interest rate environment to a high interest rate environment is traumatic for highly leveraged companies and the economy in general. To cut costs, increasing layouts is a serious possibility, which will reduce consumer spending even more and deepen the recession – a negative spiral that is accompanied by the bottom of the stock market and interest rates – that is the time to buy assets.

As we have been saying for the past weeks:

“Historically, the beginning of the last recessions has

coincided with the time the FED starts cutting rates. The FED has

started cutting a few months ago, and should cut more in 2025.”

Recommended Videos

Video: Nastiest Warning Yet: What Jerome Powell (Fed) JUST Said.

Channel: Meet Kevin

Video: How He Built A $200 Million/Year Security Company

Channel: School of Hard Knocks

Video: How Can You Be Broke When You Can Just Do This?

Channel: Tai Lopez