Market Recap: 30 March – 1 April 2026

Review of Financial Markets

US Stock Market

The business week was shorter due to Good Friday and the US stock markets being closed. The US stock market indices rebounded this week, to keep the bulls in good spirits! The S&P500 and the NASDAQ 100 recovered 3.4% and 4%, respectively. The small cap index (Russell 2000) was up by 3.2%. Trading volumes were slightly below average.

Commodities

Gold and Silver recovered 4.1% and 4.7%, and sit around 4670$/oz and 73$/oz, respectively. After months of a bull run, the metals are now correcting and consolidating. As in any tumultuous period, liquidity is king!

WTI crude oil fluctuated between 96$ and 114$ per barrel – another turbulent week – and closed around 112$/bbl. In February, WTI traded around $65/bbl — a sharp contrast!!! Natural gas fell around 10% both in the US and Europe.

Bitcoin was essentially unchanged for the week and continues around 67k$, a level that should act as a short term support, unless overall liquidity starts to tighten.

US Dollar, Money Supply

The relative strength of the US dollar (DXY) was unchanged, closing at 100.2. The EUR/USD is around 1.151$, the GBP/USD is at 1.32$, and the USD/JPY is at 159.63 JPY.

US M2 money supply in February was at 22.67T$, still on a growth trend, showing a continuous expansion in the money supply since December 2023. If the money supply starts to contract, it will be a confirmation of the credit cycle reaching a turning point.

The national financial conditions index (NFCI) released on 23rd of March 2026 shows a 4.5% tightening in financial conditions. Financial conditions will likely continue on a tightening trend as long as the international geopolitical and energy situation remains unstable. Note that this indicator is delayed by two weeks. Positive numbers in the NFCI mean tighter financial conditions, while negative numbers indicate looser financial conditions.

Bonds and Options

US bond yields fell slightly, and now sit at 3.805% for the 2-year and 4.309% for the 10-year. Long-term growth and inflation expectations are at 4.880% (30-year US bonds). The yield curve has uninverted since a year ago – a typical sign of an impending recession.

The VIX fell massively and closed the week at 24 as the market rose. If options sellers believe this is just the beginning of a bigger correction, then this is not the moment to sell puts – the time will come! However, if you see any very specific opportunities plus a juicy option premium, go ahead!

Weekly Commentary

The conflict across the Middle East continues and we fear war escalation moving toward a broader regional conflict:

- The conflict between the U.S.–Israel alliance and Iran continues to intensify, with new strikes on strategic infrastructure (including petrochemical and possibly nuclear-related sites).

- Israel is reportedly preparing further attacks on Iran’s energy sector, potentially a major next step.

- Iran has rejected a U.S. ultimatum and continues retaliatory missile/drone attacks across the region.

- Iran may easily disturb traffic in the Strait of Hormuz by laying mines (How Iran Can Stop Shipping With Mines, From the Arabian Gulf to the Red Sea).

Asia is facing a dual energy crisis marked by both soaring prices and physical supply disruptions as the war in the Middle East constrains flows through the Strait of Hormuz. A new report by Morningstar DBRS highlights that roughly one-fifth of global crude oil and LNG supply has been affected by disruptions at the critical chokepoint, with Asia absorbing the majority of the impact due to its heavy dependence on imported hydrocarbons. About 83% of oil and LNG shipments passing through Hormuz are destined for Asian markets, amplifying the region’s exposure.

The oil price spiking due to the recent war may be the last “straw that broke the camel’s back” – in this case, the back of the economy. At this point we would suggest the readers to increase reserves, and to prepare for rough times. Any crisis will bring opportunities, but we must be prepared to take advantage of them.

We don’t predict markets — we track liquidity, risk, and the forces shaping the cycle.

Good luck, stay prepared and happy Easter.

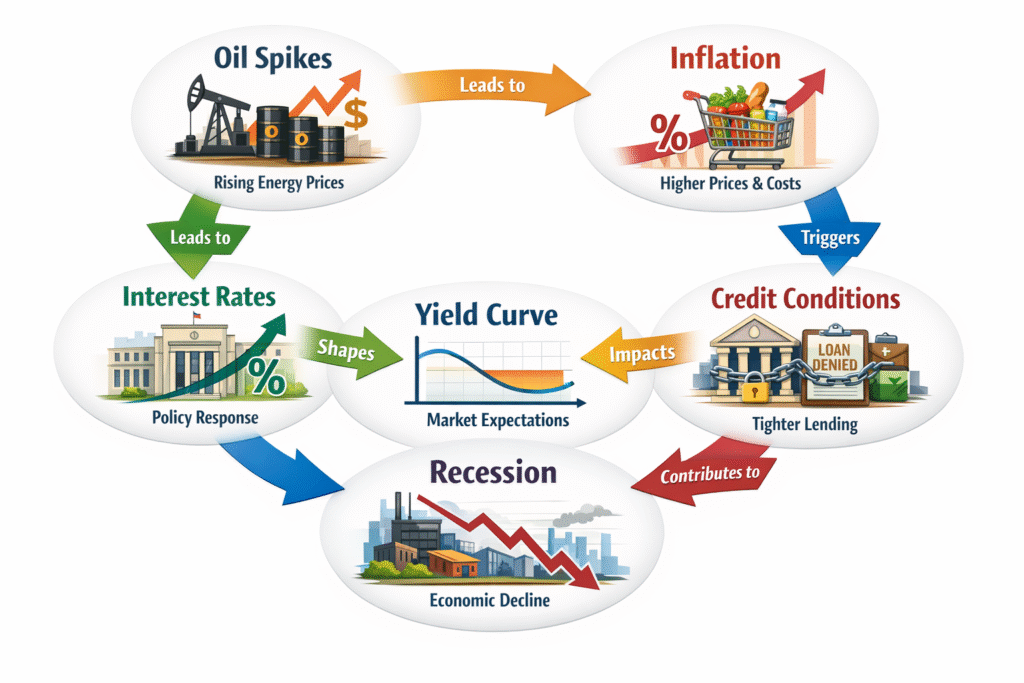

Macro briefs Strategic View

Read our articles explaining macro interactions and the business cycle

- Oil spikes → inflation

- What causes inflation? → A deep dive into prices, money and the economy

- Inflation expectations: how much they really matter? → Central bank narratives

- Interest rates → policy response

- Yield curve → market expectations

- Credit conditions → transmission mechanism

- Recession → economic outcome

Weekly Recommended Videos

Video: Ken McElroy and Grant Cardone Breaking Down the 2026 Debt Crisis

Channel: Ken McElroy

Video: 9 Habits That Build Quiet Wealth (No Luck, No Stress)

Channel: The Mindset Mentor Podcast

Video: The Financial Freedom STRATEGY Nobody Teaches (Infinity Investing)

Channel: Toby Mathis Esq | Tax Planning & Asset Protection