Introduction — Loans Are Not the End of the Story

A mortgage is often perceived as a simple bilateral agreement between a borrower and a bank, yet in modern financial systems this view is incomplete. Loans are not merely originated and held; they are increasingly transformed into financial assets, distributed across investors, and financed through layered funding structures that extend far beyond the initial transaction.

Here we explore how this process works, which is essential to understanding how credit expands, how liquidity propagates through the system, and ultimately how financial markets behave. What begins as a mortgage issued to a household can end up as a security held by a pension fund, financed in short-term funding markets, and influenced by central bank policy.

I. Loan Origination — The Starting Point of Credit Creation

The process begins with loan origination, where a financial institution—typically a commercial bank or a specialized mortgage lender—extends credit to a borrower. In the case of residential mortgages, this involves underwriting the borrower’s income, creditworthiness, and collateral (the property itself), and setting the terms of the loan, including maturity and interest rate.

At this stage, credit is created in its most direct form. The loan appears as an asset on the lender’s balance sheet, while a corresponding deposit is created in the borrower’s account, illustrating the fundamental mechanism through which banks expand the money supply.

However, this is only the first step in a much longer chain.

II. Why Loans Are Sold — Balance Sheets and Capital Recycling

Contrary to common perception, banks and mortgage originators do not typically intend to hold loans until maturity. Instead, they operate within a system that incentivizes the continuous recycling of capital, allowing them to originate new loans without being constrained by their balance sheets.

Holding loans ties up regulatory capital and exposes institutions to interest rate and credit risk. By selling loans into the secondary market, lenders can remove these exposures, free up capital, and generate fee income, effectively transforming lending into a high-turnover activity rather than a long-term investment.

This dynamic is central to modern credit systems: originate, distribute, repeat.

III. The Role of Fannie Mae and Freddie Mac

A critical component of the U.S. mortgage market is the presence of government-sponsored enterprises (GSEs), primarily Fannie Mae and Freddie Mac. These institutions do not originate loans themselves; instead, they purchase mortgages from lenders, guarantee their credit quality, and facilitate their transformation into standardized securities.

By providing guarantees against default, these entities reduce the perceived risk of mortgage-backed securities, making them attractive to a wide range of investors. At the same time, they impose underwriting standards, ensuring a degree of uniformity across the loans that enter the securitization pipeline.

This system allows mortgage originators to sell loans quickly and at scale, thereby sustaining the flow of credit to households.

Sources:

IV. Securitization — Turning Loans into Securities

Once loans are acquired, they are pooled together and transformed into mortgage-backed securities (MBS), which represent claims on the cash flows generated by the underlying mortgages.

To make this process more concrete, consider the following stylized example:

A pool of 1,000 residential mortgages, each with an average balance of $300,000 and an interest rate of 6.5%, results in a total pool size of $300 million. These loans are sold to Fannie Mae, which packages them into an MBS. Investors who purchase this security receive monthly payments derived from homeowners’ principal and interest payments.

In this structure, the mortgage payments made by households are effectively redirected to investors, transforming illiquid loans into tradable financial instruments.

The securitization process increases liquidity in the financial system by allowing loans to be bought and sold, but it also introduces complexity, as the link between borrower and ultimate investor becomes increasingly indirect.

Sources:

- Fannie Mae loan data: https://www.fanniemae.com/data/loan-performance-data

- Freddie Mac datasets: https://www.freddiemac.com/research/datasets

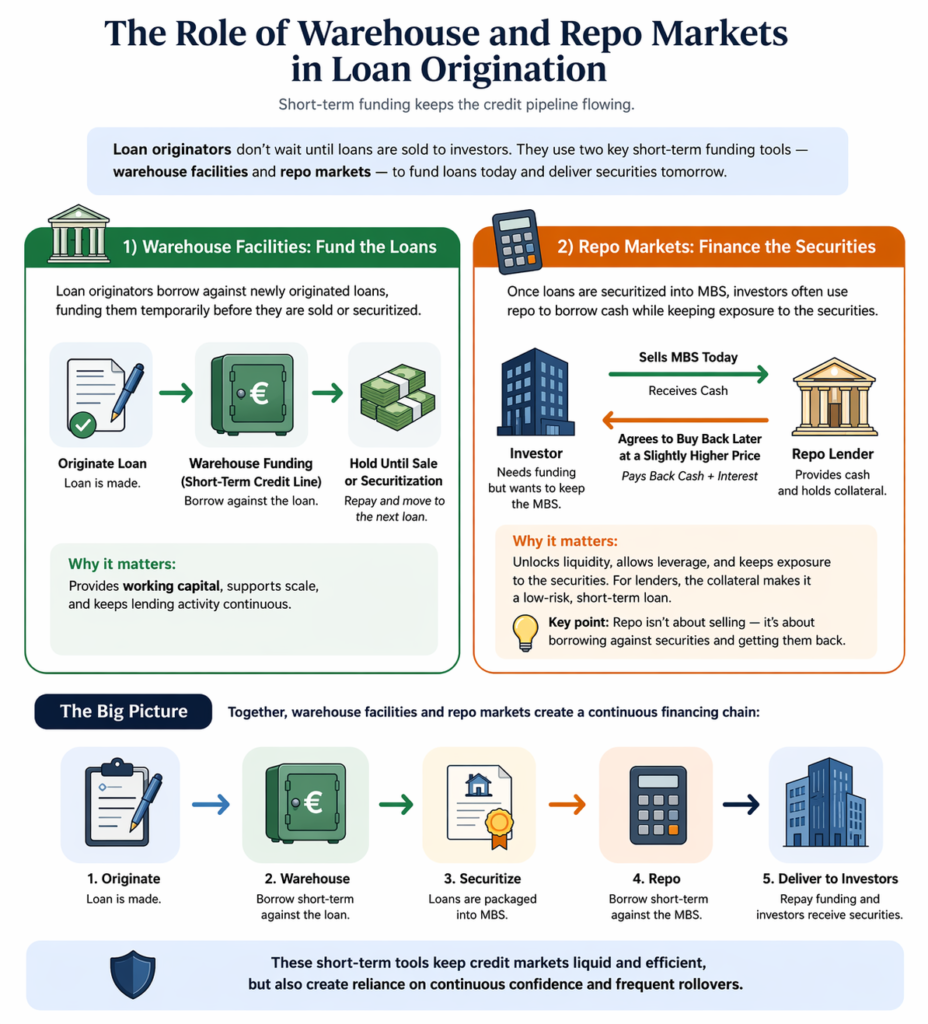

V. Warehouse and Repo Facilities — Financing the Credit Pipeline

Between loan origination and final distribution to investors lies a critical layer of short-term financing that enables the entire system to function at scale. Without it, lenders would be constrained by their own balance sheets, significantly limiting the volume of credit they could extend.

Warehouse Facilities — Funding Loan Origination

When a lender originates a mortgage, it does not typically fund that loan with its own long-term capital. Instead, it relies on warehouse lines of credit, which are short-term borrowing arrangements—usually provided by large banks.

These facilities allow lenders to:

- Fund newly originated loans immediately

- Accumulate a pipeline of mortgages before sale

- Operate with significantly higher throughput

A simplified example:

- A mortgage lender originates €100 million in home loans

- It draws on a warehouse line to fund these loans

- The loans are temporarily held on its balance sheet

- Once sold (e.g., to a securitization channel), the warehouse line is repaid

This structure effectively bridges the time gap between origination and loan sale. It allows lenders to scale origination without tying up large amounts of permanent capital.

However, this funding is short-term and conditional, meaning it must be continuously rolled over. If warehouse funding tightens, loan origination can slow abruptly.

Repo Markets — Financing Securities

Once loans are securitized into mortgage-backed securities (MBS), a different but closely related funding mechanism comes into play: the repurchase agreement (repo) market.

At first glance, a repo transaction looks like a sale. An institution sells a security (such as an MBS) and agrees to buy it back later—often the next day—at a slightly higher price. But economically, this is not really a sale. A repo is best understood as a short-term, collateralized loan.

To see this more clearly, imagine an investor that owns €50 million in MBS but needs cash. Instead of selling the bonds permanently, it enters into a repo: it “sells” the MBS for €49 million and agrees to repurchase them shortly after for €49.01 million. In practice, the investor has borrowed €49 million, paid a small amount of interest, and used the MBS as collateral.

Crucially, the investor intends to get the MBS back. This is not about exiting the position—it is about financing it.

A useful analogy is refinancing a house. You unlock cash from an asset you own, while continuing to benefit from it. The difference is that in repo markets, the lender temporarily holds the asset itself, making the structure safer and easier to enforce.

Why use repo at all?

Repo allows investors to raise cash without selling their assets, maintain exposure to the income generated by those securities, and, in many cases, increase returns by using leverage. By borrowing against their holdings, they can hold larger portfolios than their own capital alone would allow.

At the same time, lenders are willing to provide this funding because they are well protected. They hold the collateral directly, apply a small buffer (a “haircut”), and operate over short maturities, which allows them to reassess risk frequently.

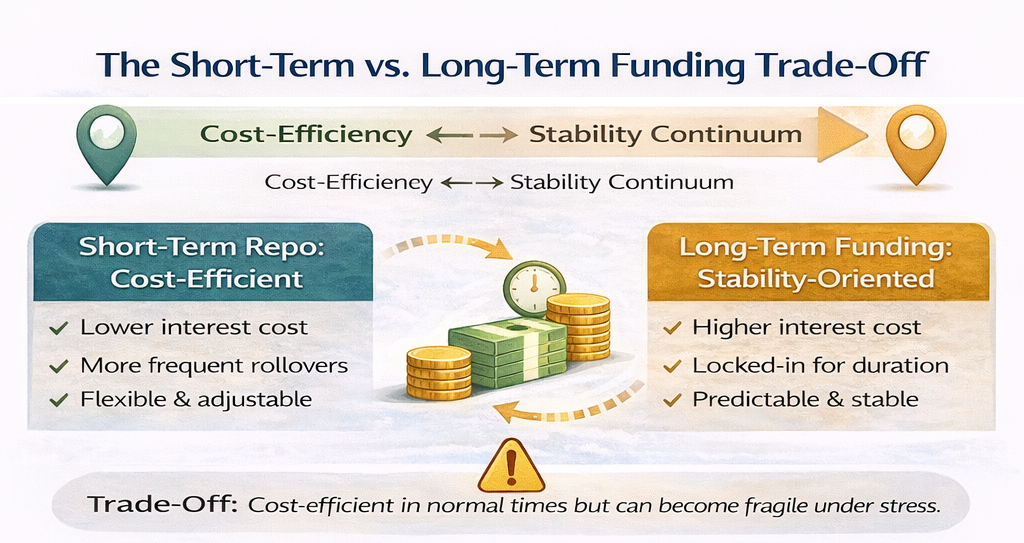

But why is the funding so short-term?

This is where the system becomes more subtle.

At first glance, it might seem more natural to use long-term funding. It would reduce uncertainty and avoid the need to constantly roll over borrowing. Yet in practice, repo markets are overwhelmingly short-term—often overnight.

The reason is that short-term funding benefits both sides of the transaction, even if it introduces some fragility.

For lenders, short maturities provide control. By lending overnight, they can continuously reassess the borrower and the value of the collateral. If conditions deteriorate, they can demand better terms (such as higher haircuts) or withdraw funding altogether. This flexibility is a key reason why repo markets can offer relatively low interest rates.

For borrowers, the trade-off is cost. Short-term funding is typically cheaper than long-term borrowing, especially when backed by high-quality collateral like MBS. By rolling over short-term repo, investors can finance their positions at lower rates, improving returns.

In other words, the system implicitly trades stability for efficiency:

- Long-term funding → more stable, but more expensive

- Short-term funding → cheaper, but must be continuously renewed

Most market participants choose the latter.

The trade-off: efficiency vs fragility

This reliance on short-term funding works smoothly in normal conditions. But it introduces a key vulnerability.

Because repo borrowing must be rolled over frequently, the system depends on continuous confidence. If lenders suddenly become cautious, they can refuse to renew funding or demand stricter terms. When that happens, borrowers may be forced to sell assets quickly to raise cash.

This dynamic was a central feature of the Global Financial Crisis: funding did not disappear gradually—it stopped rolling.

Repo is not about selling securities—it is about borrowing against them, using short-term funding that is efficient in normal times but can become fragile under stress.

A Continuous Funding Chain

Together, warehouse and repo facilities form a continuous financing chain:

- Warehouse funding supports loan origination

- Loans are sold and securitized

- Resulting securities are funded in repo markets

This creates a system where credit is:

- Originated with short-term funding

- Transformed into long-term assets

- Financed again with short-term liquidity

Liquidity and Fragility

While highly efficient, this structure introduces systemic risk.

Both warehouse lines and repo funding depend on:

- Counterparty confidence

- Collateral quality

- Market liquidity

If confidence deteriorates:

- Warehouse lenders may reduce or withdraw credit lines

- Repo lenders may demand higher haircuts or refuse to roll funding

- Forced deleveraging can occur rapidly

This dynamic was clearly visible during the 2008 Global Financial Crisis, when disruptions in short-term funding markets amplified stress across the entire financial system.

Why It Matters

Warehouse and repo facilities are not just technical details—they are core infrastructure of modern credit markets. They determine:

- How quickly loans can be originated

- How cheaply securities can be financed

- How resilient (or fragile) the system is under stress

In essence, they are the hidden plumbing that connects loan creation to global liquidity.

Sources:

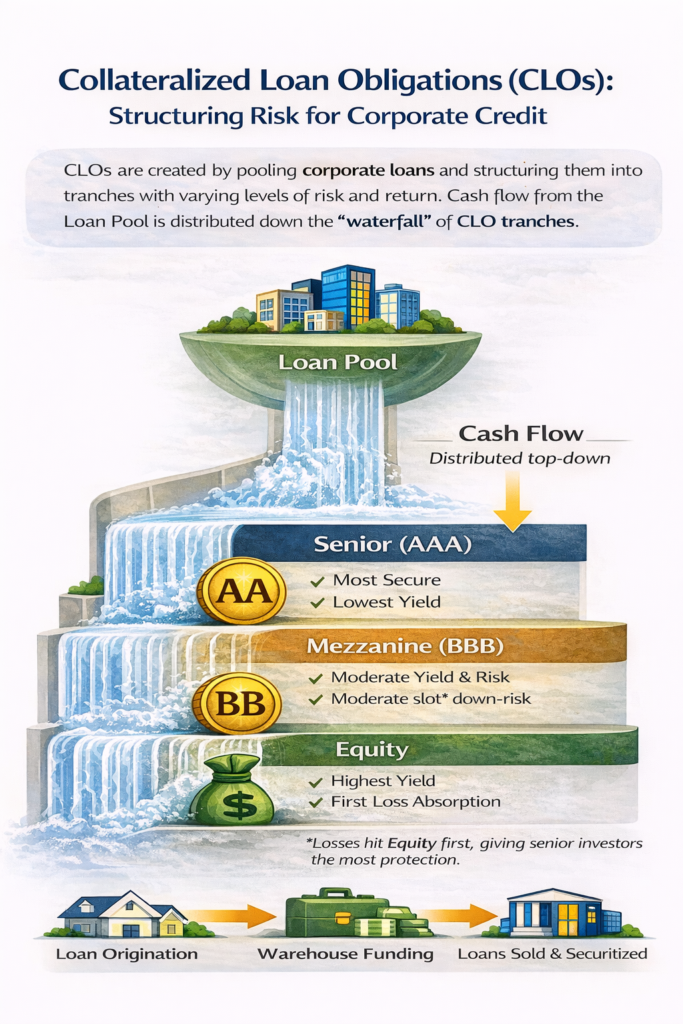

VI. Collateralized Loan Obligations — Extending the Model

The securitization model extends beyond mortgages into corporate credit through instruments such as a Collateralized Loan Obligation (CLO). While structurally similar to MBS, CLOs are backed by pools of leveraged loans made to corporations rather than by residential mortgages.

A simplified example illustrates the structure:

A CLO may consist of $500 million in corporate loans, which are pooled and divided into tranches with different levels of risk and return:

- Senior tranche (AAA): $300M, lower yield, highest protection

- Mezzanine tranche (BBB): $100M, moderate yield and risk

- Equity tranche: $100M, highest yield, first to absorb losses

Losses are absorbed from the bottom up, meaning that equity investors bear the first losses, while senior investors are protected unless defaults exceed certain thresholds.

This process, known as tranching, redistributes risk across investors with different risk appetites, making it possible to finance a broader range of borrowers.

Sources:

- https://www.sifma.org/resources/research/

- CLO trustee reports (e.g., Wells Fargo, U.S. Bank)

VII. Why This System Exists — Liquidity, Scale, and Efficiency

The transformation of loans into securities serves several purposes. It increases liquidity by converting illiquid assets into tradable instruments, lowers borrowing costs by broadening the investor base, and allows financial institutions to scale their lending activities.

At the same time, it introduces new layers of complexity and interdependence. Risk is not eliminated but redistributed, often in ways that are difficult to fully observe. The system becomes more efficient, but also more opaque.

VIII. When the System Breaks — Lessons from the Global Financial Crisis

The vulnerabilities of this system became evident during the Global Financial Crisis, when a combination of weak underwriting standards, excessive leverage, and mispriced risk led to a collapse in mortgage-backed securities markets.

As defaults rose, the value of structured products declined sharply, triggering losses across financial institutions and disrupting funding markets, particularly the repo market. Liquidity evaporated, and assets that were previously considered safe became difficult to trade.

This episode highlighted a fundamental risk: when confidence in the underlying assets deteriorates, the entire structure can unravel rapidly.

IX. From Loans to Liquidity — A System-Level Perspective

Viewed through a macro lens, the mortgage and securitization system is not merely a financial innovation, but a mechanism for amplifying and distributing liquidity.

Loans are originated using bank credit, financed through short-term funding, transformed into securities, and ultimately held by investors across the global financial system. At each stage, liquidity plays a critical role, enabling the system to function smoothly—or, in times of stress, to seize up.

This process connects directly to broader macro dynamics, linking household borrowing to capital markets, and local lending decisions to global financial conditions.

Conclusion — Credit as a Manufactured Product

Modern credit systems are not static; they are dynamic, layered, and deeply interconnected. Mortgages, corporate loans, and other forms of credit are not simply created and held, but manufactured, transformed, and distributed across institutions and markets.

Understanding this process provides a deeper insight into how liquidity is created, how risk is allocated, and how financial systems evolve over time. It also reinforces a broader point: to understand markets, one must look not only at outcomes, but at the mechanisms that produce them.