Market Recap: 16-20 March 2026

Review of Financial Markets

US Stock Market

The US stock market indices dipped for the third consecutive week. The S&P500 and the NASDAQ 100 lost 1.9% and 2%, respectively. The small cap index (Russel 2000) fell 1%. Trading volumes have been slightly higher than average – but not panic-like. The biggest gainers have been oil and fertilizer producers.

COMMODITIES

Gold fell 10.5% and is now around the 4.5k$/oz level. After peaking around 120$/oz in January 2026, this week silver lost 15.7% and currently hovers around 68$/oz. Under gravity, all that goes up, eventually comes back down! The metals are now correcting after months of a bull run. Liquidity will be king going forward!

WTI crude oil fluctuated between 91-102$ per barrel – way more stable than in the previous week – and closed the week at 98$/bbl. Just 3-4 weeks ago oil was around 67$/bbl!!! US natural gas is stable, but in Europe, the price has doubled since 3 weeks ago.

Bitcoin lost 2.9% for the week and is now around 70.7k$, an area that is likely prone to keep the price stable for a while, unless overall liquidity starts drying up.

US DOLLAR, MONEY SUPPLY

The relative strength of the US dollar (DXY) fell slightly to 99.5. The EUR/USD is around 1.157$, the GBP/USD is at 1.334$, and the USD/JPY is at 159.23 JPY.

US M2 money supply in January was at 22.4T$, still on a growth trend, showing a continuous increase in the money supply since December 2023. Banks didn’t stop lending so far – if the money supply was going down, it would be a warning sign for the economy and equities.

The national financial conditions index (NFCI) released on 9th of March 2026 shows the tightening of financial conditions by 3.1%. Financial conditions will likely continue on a tightening trend as long as the international geopolitical and energy situation is not stabilized. Note that this indicator is delayed by two weeks. Positive numbers in the NFCI mean tighter financial conditions, while negative numbers indicate looser financial conditions.

BONDS AND OPTIONS

US bond yields now sit at 3.907% for the 2-year and 4.384% for the 10-year. Long-term growth and inflation expectations are at ~4.947% (30-year US bonds), slightly higher than a few weeks ago. The yield curve has uninverted since a year ago.

The VIX oscillated less than last week and closed the week again around 27. There is clearly more fear in the markets and selling pressure is increasing. If options sellers believe this is just the beginning of the downturn, then this is not the moment to sell puts, so hold your horses – the time will come! However, if you see any very specific opportunities plus a juicy option premium, go ahead!

Weekly Commentary

The conflict across the Middle East continues, and the path going forward is everything but clear.

President Donald Trump has said he is considering “winding down” the Iran war because the US was “getting very close” to meeting its military objectives. He also said the Strait of Hormuz would have to be guarded by other nations who use it, stating that the US wasn’t one of them. Energy prices have soared since Iran effectively closed the shipping route after the conflict began last month. Iran’s new supreme leader, meanwhile, said the country had dealt “a dizzying blow” to the enemy. Trump has previously indicated the war was almost over, only for it to escalate. The White House this week requested $200bn more in funding for the conflict. More troops and warships are being sent to the region. (https://www.bbc.com/news/articles/cpd5l00z7n6o)

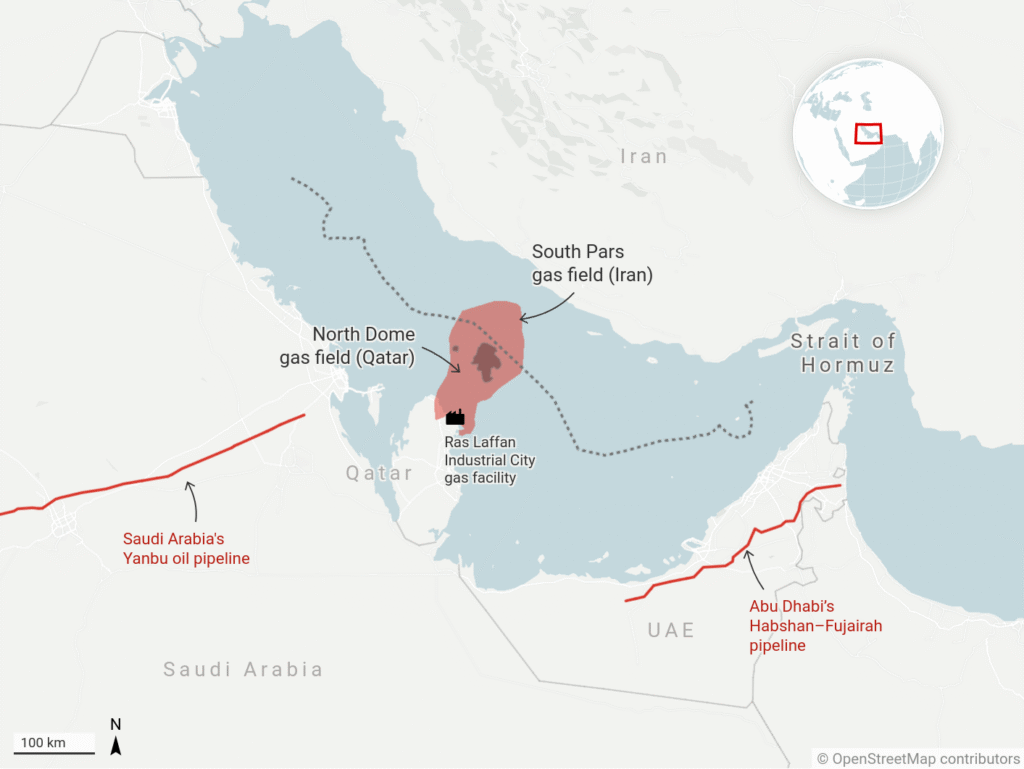

This week, one of the highlights was the Iranian missile attacks on the Ras Laffan Industrial City, Qatar’s main gas facility. “The State of Qatar expresses its strong condemnation and denunciation of the blatant Iranian attack targeting Ras Laffan Industrial City, which caused fires resulting in significant damage to the facility,” Qatar’s Ministry of Foreign Affairs said in a statement on Wednesday. (https://www.aljazeera.com/news/2026/3/18/qatar-says-iran-missile-attack-sparks-fire-causes-damage-at-gas-facility)

On the other hand, earlier this week, Israeli forces bombed the South Pars gas field, a crucial part of Iran’s domestic energy sector. South Pars accounts for about 70% of the country’s total gas production and 90% of its domestic energy use. It’s also a key processing site for Iranian gas exports, which mainly go to Turkey and Iraq. (https://theconversation.com/why-middle-east-gas-field-attacks-could-send-energy-prices-soaring-278777)

Without digging further into details, it seems clear that the multilateral and widespread infrastructure destruction and the closing of the Strait of Hormuz is likely to continue inducing considerable volatility in the energy markets in the weeks and maybe months to come.

This was also FED week! The most recent Federal Open Market Committee (FOMC) meeting underscored the Fed’s stance amid ongoing economic uncertainties. The Federal Reserve’s March meeting was a notably more hawkish affair than many in the market had anticipated. While the headline decision to maintain the target range for the federal funds rate at 3.50% to 3.75% was a near-certainty, the underlying messaging and the updated Summary of Economic Projections suggested a far more aggressive stance. The “dot plot” served as the primary vehicle for this hawkish surprise. Despite a recent labor market report showing a loss of 92,000 jobs, the median projection still signals only one rate cut for the remainder of 2026. What stood out most was that only two committee members remained in the two-cut camp for additional monetary easing. Also, it appears Chair Jerome Powell’s own dot moved higher, signaling a central bank that is far from finished with its battle against inflation. (https://www.forbes.com/sites/garthfriesen/2026/03/18/why-the-march-fed-meeting-was-more-hawkish-than-expected/). Later in the week, the ECB also communicated with a more hawkish tone than expected. (https://think.ing.com/articles/ecb-mar26-meeting-with-presser/).

Surprisingly, central banks are turning hawkish due to worries of persistent inflation as a consequence of higher energy prices. We fear that higher energy costs may have dire consequences for an already flattening economy in the West and across the globe. Could this be the catalyst for the so-awaited recession? Or perhaps the middle-east situation de-escalates quickly and we go back to threading water for a few more years before the credit and market cycle turns downwards…only time will tell.

Next week we will explore the situation of the private credit space, which is starting to generate worries and headlines on a daily basis. Have a nice weekend, and good luck!

Recommended Videos

Video: BREAKING: Market Signals Fed Will RAISE RATES!!

Channel: Rebel Capitalist

Video: The $3.5 Trillion Crisis No One Is Talking About

Channel: Patrick Boyle

Video: If you think about relocating, watch this.

Channel: Rico Go