(And What It Means for Markets)

Oil prices have a habit of moving sharply whenever geopolitical tensions rise. Whether it’s wars in the Middle East, sanctions on major producers, or attacks on energy infrastructure, markets tend to react almost immediately.

But why does this happen—and why does it matter so much for the global economy and financial markets?

The Short Answer

Oil prices spike during geopolitical crises because markets fear disruptions to supply. Even the risk of disruption is often enough to push prices higher.

This reaction is amplified by the fact that oil is one of the most globally traded and strategically important commodities in the world.

1. Oil Is Highly Sensitive to Supply Shocks

The global oil market is tightly balanced between supply and demand. Small disruptions can have large price effects.

Geopolitical crises often occur in key producing regions—especially the Middle East, which accounts for a significant share of global oil output.

More importantly, critical transit routes like the Strait of Hormuz handle a large portion of global oil shipments. Any threat to these routes immediately raises concerns about supply shortages.

Recent conflicts highlight this dynamic clearly. In 2026, tensions involving Iran disrupted flows through the region, which carries roughly 20% of global oil supply, pushing prices sharply higher.

2. Markets Price in Risk—Not Just Reality

One of the most important (and often misunderstood) dynamics is that oil prices react not only to actual disruptions, but to expected risks.

Economists often describe two main channels:

- Supply risk channel: fear that future production or transport could be disrupted

- Uncertainty channel: geopolitical instability increases risk premiums in markets

Even before any physical supply is lost, traders begin pricing in the possibility of shortages, which pushes prices up.

This is why oil can spike within hours of geopolitical headlines.

3. Major Historical Oil Price Spikes (Geopolitics-Driven) – the Same Pattern

Oil markets have repeatedly reacted to geopolitical shocks.

3.1. The 1973 Oil Crisis

What happened:

- Arab members of OPEC imposed an oil embargo on the US and allies

- Trigger: support for Israel in the Yom Kippur War

Price impact:

- Oil prices quadrupled (~$3 → $12)

Market impact:

- Massive inflation surge

- Global recession

- Birth of modern energy geopolitics

Key insight:

Supply weaponization → structural, long-lasting shock

3.2. The 1979 Oil Shock

What happened:

- Iranian production collapsed during the Iranian Revolution

- Followed by the Iran–Iraq War

Price impact:

- Oil prices doubled again

Market impact:

- Stagflation (high inflation + low growth)

- Central banks forced into aggressive tightening

Key insight:

Actual supply loss → prolonged inflation shock

3.3. The Gulf War

What happened:

- Iraq invaded Kuwait

- Fear of disruption in the Persian Gulf

Price impact:

- Oil doubled in a few months

- Then dropped after military resolution

Market impact:

- Short-lived recession fears

- Quick normalization after supply stabilized

Key insight:

Fear-driven spike → sharp but temporary

3.4. The 2003 Iraq War

What happened:

- Anticipation of war disrupted expectations

- Not a huge immediate supply shock, but uncertainty surged

Price impact:

- Gradual increase, not a sharp spike

Market impact:

- Oil entered a multi-year bull market (2003–2008)

Key insight:

Geopolitics + strong demand = sustained trend

3.5. The Arab Spring

What happened:

- Political instability across oil-producing regions

- Libya supply disruptions

Price impact:

- Brent moved above $100

Market impact:

- Elevated inflation pressure

- Continued commodity supercycle

Key insight:

Regional instability → persistent risk premium

3.6. The Saudi Aramco drone attacks

What happened:

- Drone strike on Saudi oil facilities

- ~5% of global supply temporarily disrupted

Price impact:

- ~15% spike in a single day (one of the largest ever)

- Short-lived spike

- Rapid normalization after supply restored

Key insight:

Infrastructure shocks → sharp but short-lived moves

3.7. The Russian invasion of Ukraine

What happened:

- Sanctions on a major oil exporter (Russia)

- Massive uncertainty in global energy markets

Price impact:

- Oil surged above $120/barrel

Market impact:

- Global inflation spike

- Aggressive central bank tightening cycle

- Energy crisis in Europe

Key insight:

Large producer disruption → systemic macro impact

Supply vs Fear

- Actual supply disruption → long-lasting price increases

- 1973, 1979, 2022

- Fear/potential disruption → short-term spikes

- 1990, 2019

Geography Matters

Most major oil shocks originate from:

- Middle East

- Russia / Eurasia

Concentration of supply = structural vulnerability

Oil Shocks = Inflation Shocks

Almost every major oil spike led to:

- higher inflation

- central bank tightening

- slower growth

This is why oil is so central to macro.

Second-Round Effects Matter More

The initial spike is just the start.

What really matters:

- Do wages rise?

- Do central banks react?

- Does demand collapse?

This determines whether:

- it’s a temporary shock

- or a recession trigger

Markets React Asymmetrically

- Oil ↑ fast on bad news

- Oil ↓ slower when risk fades (because risk premium takes time to unwind)

Examples:

- The 1990 Gulf War caused oil prices to double within months due to fears of supply disruption

- The Russia–Ukraine war (2022) pushed oil above $120 per barrel as sanctions disrupted supply

- Attacks on major facilities (e.g. Saudi infrastructure in 2019) triggered some of the largest single-day price spikes in decades.

- More recently, escalating tensions in the Middle East have again driven prices above $100 per barrel and created significant volatility across energy markets.

4. Why Oil Price Spikes Matter for the Economy

Oil is a core input across the global economy. When prices rise, the effects ripple quickly.

Inflation Rises

Higher oil prices increase:

- transport costs

- manufacturing costs

- energy bills

These costs are passed on to consumers, contributing to inflation.

Growth Slows

Higher energy costs act like a tax on the economy:

- consumers spend less elsewhere

- companies face lower margins

In extreme cases, oil shocks have contributed to recessions (as in the 1970s).

Central Banks React

If inflation rises due to energy prices, central banks may:

- delay rate cuts

- keep interest rates higher

This creates additional pressure on financial markets.

5. Impact on Financial Markets

Oil shocks don’t stay confined to energy markets—they affect nearly all asset classes.

Stocks

- Some equities related to the energy sector may temporarily benefit from elevated oil and gas prices (energy stocks typically outperform).

- However, in the medium term, broad equity markets often fall due to:

- higher costs

- lower growth expectations

Bonds

- Inflation fears push yields higher

- Bond prices may fall

Currencies

- Oil-exporting countries benefit (stronger currencies)

- Oil-importing countries suffer (weaker currencies)

Volatility rises

Geopolitical events increase uncertainty, leading to:

- higher market volatility

- risk-off sentiment

7. The “Fear vs Reality” Dynamic

A key insight: not all oil spikes are equal.

- Short-term spikes are often driven by fear

- Sustained rallies usually require actual supply disruption

Markets tend to overshoot initially, then stabilize once the real impact becomes clearer.

8. What Investors Should Watch

To understand where oil prices may go next, focus on:

- Geopolitical hotspots (Middle East, Russia, major producers)

- Shipping routes (especially chokepoints like Hormuz)

- OPEC+ decisions (supply adjustments)

- Global demand trends (growth vs slowdown)

These factors determine whether a price spike is temporary—or something more structural.

Final Thoughts – Putting it All Together

Oil sits at the intersection of geopolitics and economics. That’s why it reacts so quickly—and so violently—to global events. When geopolitical tensions rise, oil prices often move first. And when oil moves, the rest of the market usually follows. Understanding this chain reaction is essential for anyone trying to make sense of macro trends—and anticipate where markets might go next.

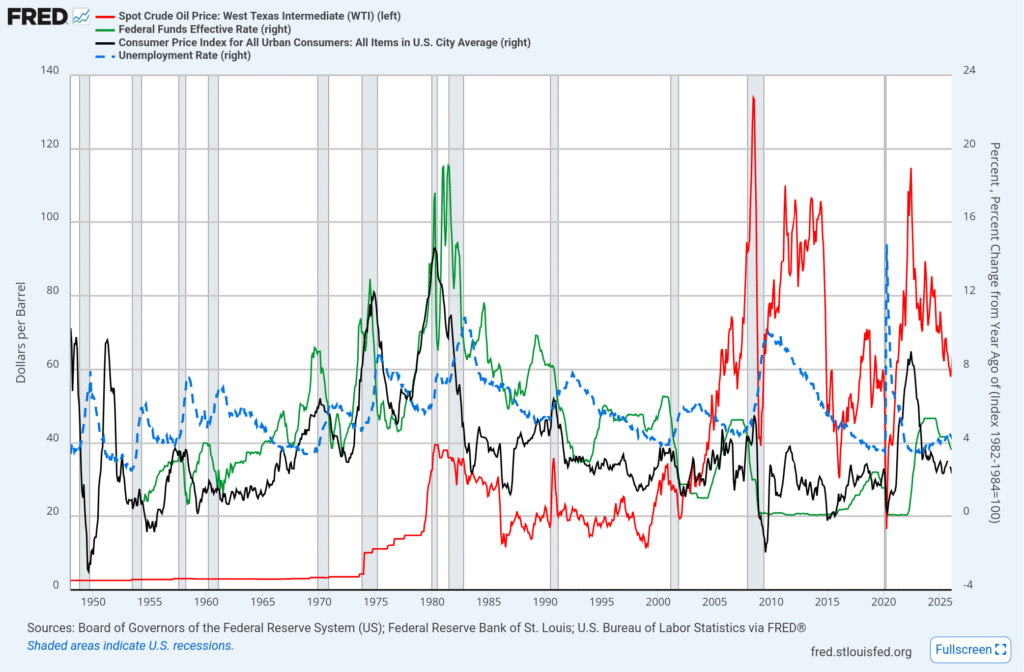

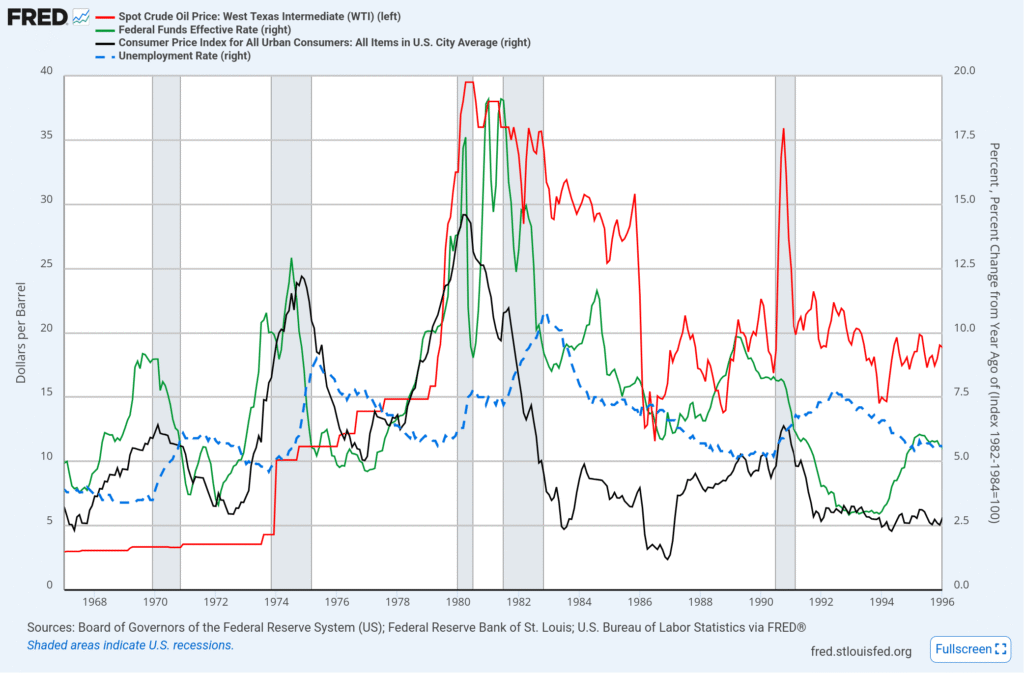

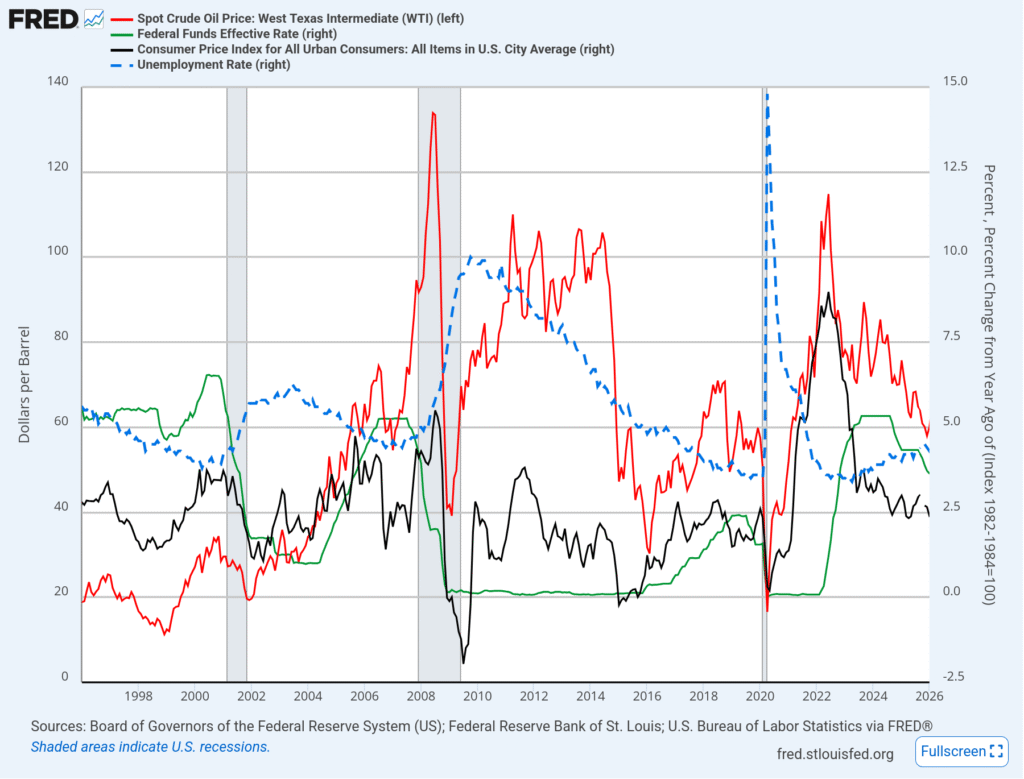

We have created a set of charts dating back to the 1950s, containing the oil price, the consumer price index (CPI), Federal funds rate and the unemployment rate.

Although each market cycle is different in terms of the FED timing and the exact catalyst that pushes markets into a downturn, we can clearly observe:

- Oil (red line) is highly correlated with the consumer price index change year-over-year, that is, the annualized inflation rate (black line)

- The FED funds rate is rising or has been higher than in the previous years right before a recession period (1956,1969,1973,1981,1989,2000, 2007, 2019, 2026)

- The rise in FED funds rate has an overlap with the rise in inflation (1976-1980) or a delay of a few months relative to the beginning of an inflation increase (eg. 2004, 2022)

- The unemployment rate is usually low before a recessionary period and takes a few months into a recession to meaningful increase (>1%). The unemployment rate is a lagging indicator, thus, it is just a confirmation of the recession.

Looking into the most recent macroeconomic trends and indicators, we see a confluence of factors, including higher interest rates and low unemployment in the past years, which typically correspond with the top of a credit and market cycle.

Taking this information together with the recent oil price spikes due to the Middle East conflict between the US and Iran in March 2026, we would be tempted to predict an imminent recession.

Subscribe below to be notified each time we publish new material!