1. Introduction

Over the past few decades, passive investing has transformed from a niche strategy into one of the dominant forces in global financial markets. What began as an academic idea has gradually evolved into the default approach for millions of investors across the world.

Yet, while the case in favor of passive investing is widely understood and frequently repeated, the case against its growing dominance is less often explored in depth. This article maintains a balanced perspective by examining both the strengths of passive investing and the structural risks that may emerge as an increasing share of capital adopts this approach.

2. What Are Market Indices?

A market index is a statistical construct designed to track the performance of a defined group of securities. Indices serve as benchmarks for investors, as representations of specific market segments, and as the foundation upon which passive investment products are built.

Most major indices today are constructed using market-capitalization weighting. This means that companies with larger market values exert a greater influence on the index’s performance. As a result, a relatively small number of very large firms can end up driving a significant portion of returns, a point often underappreciated by investors who equate index investing with balanced diversification.

The theoretical foundation of index investing is closely tied to the Efficient Market Hypothesis, most notably associated with Eugene Fama. In its simplest form, the hypothesis states that financial markets rapidly incorporate available information into asset prices, making it extremely difficult for investors to consistently identify undervalued or overvalued securities.

In its stronger interpretations, the Efficient Market Hypothesis suggests that even professional investors, equipped with extensive resources and information, should not expect to systematically outperform the market after costs. This insight leads directly to the logic of passive investing: if markets are broadly efficient, then attempting to beat them may be less effective than simply owning them at minimal cost.

While the hypothesis has been widely debated and is not universally accepted in its strongest form, it has provided the intellectual foundation for the rise of index-based investing.

Read more:

- A Random Walk Down Wall Street by Burton Malkiel

- The Most Important Thing: Uncommon Sense for the Thoughtful Investor by Howard Marks

- S&P Dow Jones Indices methodology papers

- MSCI Global Investable Market Indexes methodology

3. A Brief History of Index Funds and ETFs

The practical implementation of passive investing began in 1976 with the launch of the Vanguard 500 Index Fund, created by John C. Bogle at The Vanguard Group. At the time, the fund was widely criticized and even mocked, as it abandoned the ambition of beating the market.

The ETF revolution followed in 1993 with the launch of the SPDR S&P 500 ETF (SPY) by State Street Global Advisors. This innovation allowed investors to trade an entire index intraday, combining diversification with liquidity.

Suggested reading:

- The Little Book of Common Sense Investing

- The Bogleheads’ Guide to Investing

4. What Are Index Funds and ETFs?

Index funds are mutual funds designed to replicate the performance of a given index and are typically priced once per day at their net asset value. Exchange-traded funds, or ETFs, pursue the same objective but are traded on stock exchanges throughout the day.

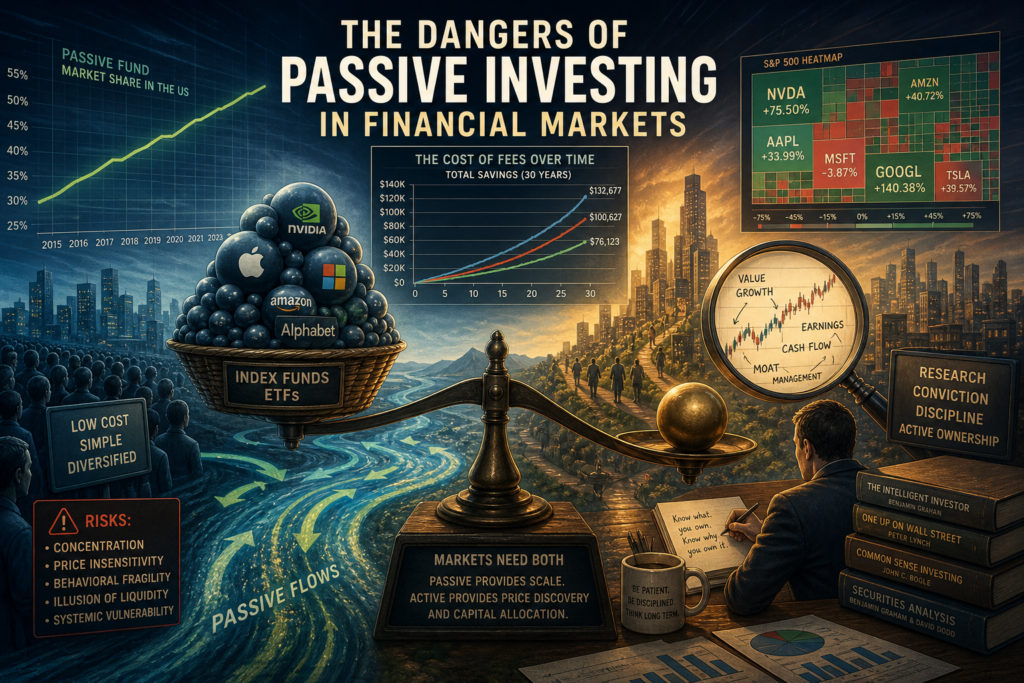

One of their defining features is cost efficiency. A widely used S&P 500 ETF such as VOO typically carries an expense ratio of approximately 0.03 percent per year, while a global developed markets ETF may charge around 0.20 percent. By contrast, actively managed mutual funds often charge between 0.8 and 1.5 percent annually.

Read more:

- Morningstar annual fee studies

- Vanguard cost comparison tools

5. The Advantages of Passive Investing

5.1 Low Costs

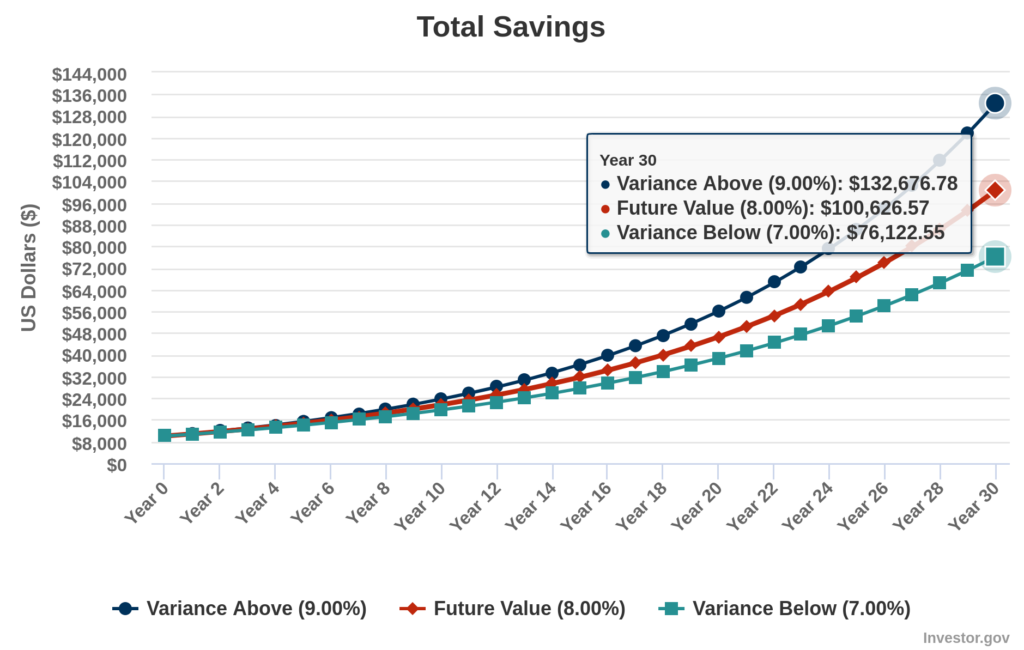

The cost advantage of passive investing is one of its most powerful attributes. Over decades, even small differences in fees can lead to materially different outcomes.

Here’s a simple way to think about it: If you invest $10,000 for 30 years at an 8% annual return, you’d end up with about $100k. If that return is reduced to 7% because of fees, you’d end up with around $76k. That’s a ~24% difference from just a 1% annual fee. Fees compound in reverse.

5.2 Diversification

Index funds provide exposure to a wide array of companies, reducing the risk associated with individual securities.

5.3 Simplicity

Passive investing reduces decision complexity and encourages consistency.

5.4 Strong Advocacy

Prominent investors such as Warren Buffett have repeatedly recommended low-cost index funds for most individuals.

6. Who Are Index Funds and ETFs Best For?

Passive investing is particularly well suited for individuals who lack the time or expertise to analyze markets in depth and are satisfied with market-level returns.

However, simplicity at the strategy level does not eliminate complexity at the behavioral level. Investors must still endure volatility and maintain discipline during downturns.

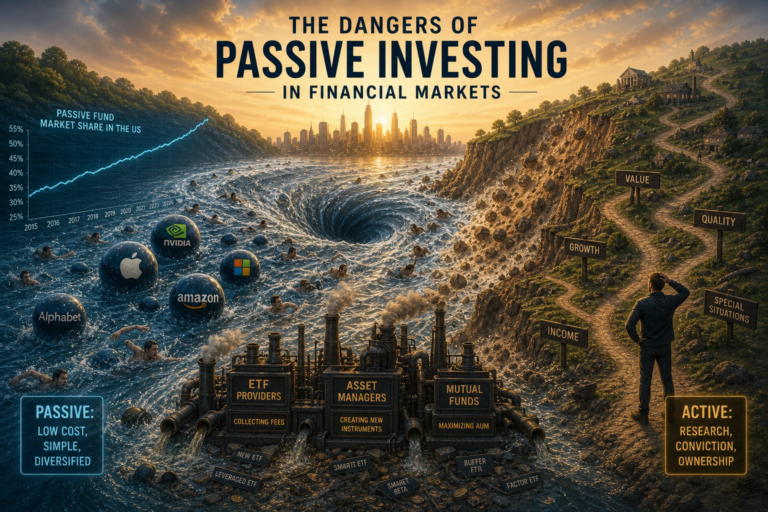

7. The Hidden Risks of Passive Investing

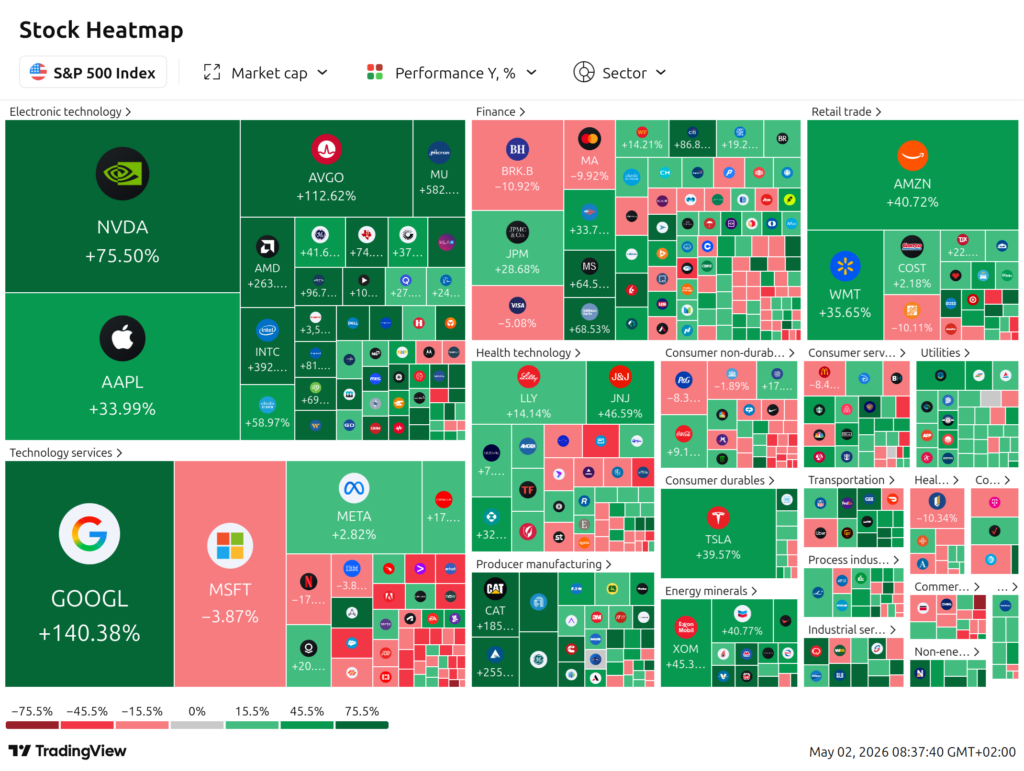

7.1 Concentration Risk Disguised as Diversification

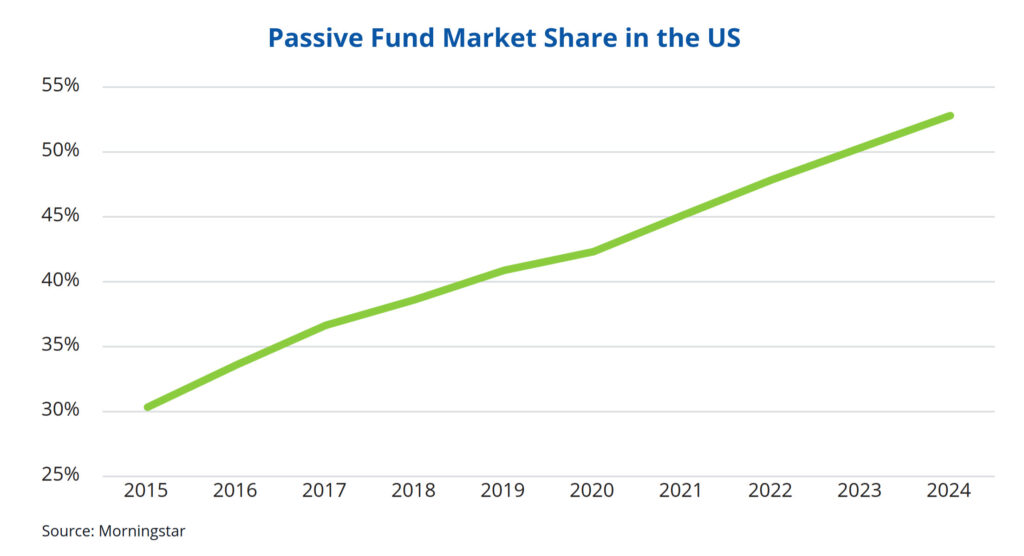

Market-cap weighting can lead to significant concentration in a small number of large companies, reinforcing their dominance through continuous inflows. In the heat-map below, the area is proportional to the weight in the S&P500 index (2nd May 2026):

7.2 Price Formation: Flows vs Fundamentals

Passive investing introduces a structural shift in how prices are formed. Capital is allocated not on the basis of valuation, but according to index weights. As a result, securities that rise in price attract additional inflows, while those that decline receive less capital.

This creates a feedback loop in which flows increasingly influence prices, sometimes independently of underlying fundamentals. In such a framework, valuation can become secondary to momentum and allocation mechanics.

This raises a deeper question: if passive investors do not engage in price discovery, who ensures that prices remain anchored to reality? The answer lies with active participants, whose role becomes more critical as passive investing expands.

Read more:

- Bank for International Settlements reports on market structure

- International Monetary Fund Global Financial Stability Reports

7.3 Investor Apathy and Behavioral Fragility

Passive investing encourages a hands-off approach, which can result in limited engagement with underlying assets. While the strategy is simple in principle, it still requires emotional discipline in practice.

Investors who lack understanding of what they own may be more prone to panic selling during downturns. By contrast, those who follow individual businesses more closely may develop stronger conviction, which can improve their ability to remain invested and avoid panic selling.

This highlights an important distinction: passive investing simplifies decisions, but it does not eliminate behavioral risk.

Read more:

- Thinking, Fast and Slow by Daniel Kahneman

7.4 Time Horizon Mismatch

Passive investing implicitly assumes a long-term horizon, yet many investors behave in a short-term manner. This mismatch often leads to poor realized outcomes, as investors enter and exit at unfavorable times.

In practice, the average investor in an index fund may underperform the fund itself due to timing decisions.

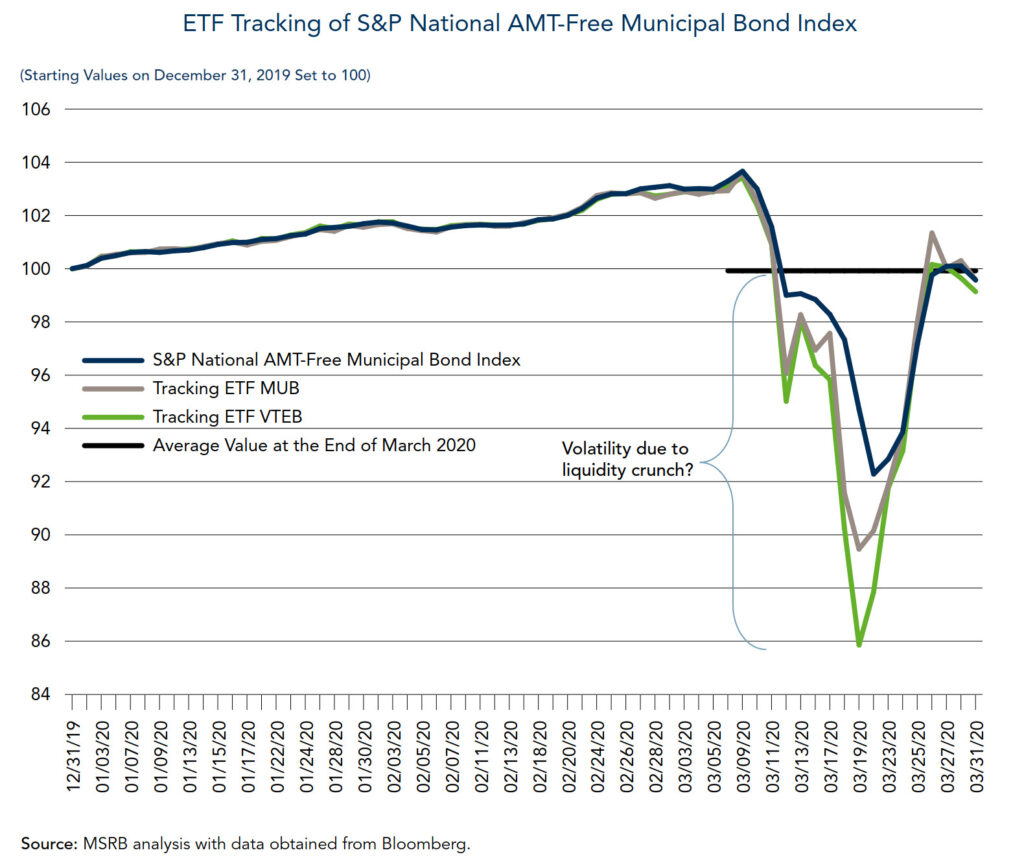

7.5 The Illusion of Liquidity

ETFs offer intraday liquidity, but this liquidity is, in part, a function of the underlying assets. In segments such as corporate bonds or less liquid equities, there may be a mismatch between the liquidity of the ETF and that of its holdings.

During periods of stress, this mismatch can manifest in wider spreads and deviations between market price and net asset value, as observed during episodes such as the market dislocation of March 2020, as shown in the example below (source).

7.6 Systemic Risks

As passive investing grows, it may contribute to higher correlations between assets and amplify the impact of capital flows. These dynamics can increase fragility, particularly in environments characterized by rapid inflows or outflows.

8. Active Investing: The Other Side of the Equation

8.1 Why Active Investing Often Underperforms

Active investing faces structural headwinds, including higher fees, intense competition, and the rapid dissemination of information.

Empirical evidence strongly supports this conclusion. The SPIVA Scorecards published by S&P Dow Jones Indices consistently show that a majority of active managers underperform their benchmarks over long periods, particularly after fees. Academic studies on mutual fund performance reach similar conclusions, often finding little persistence in outperformance.

Read more:

- SPIVA U.S. and Europe Scorecards

- Common Sense on Mutual Funds

8.2 Why Active Investing Still Matters

Active investors play a critical role in price discovery and capital allocation. By analyzing companies and making valuation-based decisions, they help ensure that prices reflect underlying fundamentals.

Markets, in this sense, rely on active participants as a form of intellectual infrastructure.

8.3 Market Efficiency Across Regions

Market efficiency is not uniform across geographies. While large-cap U.S. equities are highly researched and relatively efficient, other segments—such as small-cap stocks or emerging markets—may offer greater opportunities for active investors.

This suggests that the effectiveness of active strategies may depend on where they are applied.

9. How Much Diversification Is Ideal for Stock Pickers?

For active investors, diversification must be balanced against conviction. Excessive diversification can dilute the impact of well-researched ideas, while insufficient diversification increases risk.

A portfolio of ten to thirty companies is often considered a reasonable balance.

10. Beyond Stocks: Diversification and Staying Power

10.1 The Role of an Emergency Fund

A crucial but often overlooked aspect of investing is the ability to remain invested during adverse conditions. Investors without sufficient liquidity may be forced to sell at unfavorable times.

An emergency fund provides stability and increases the likelihood of maintaining a long-term strategy.

10.2 Dry Powder and Opportunity

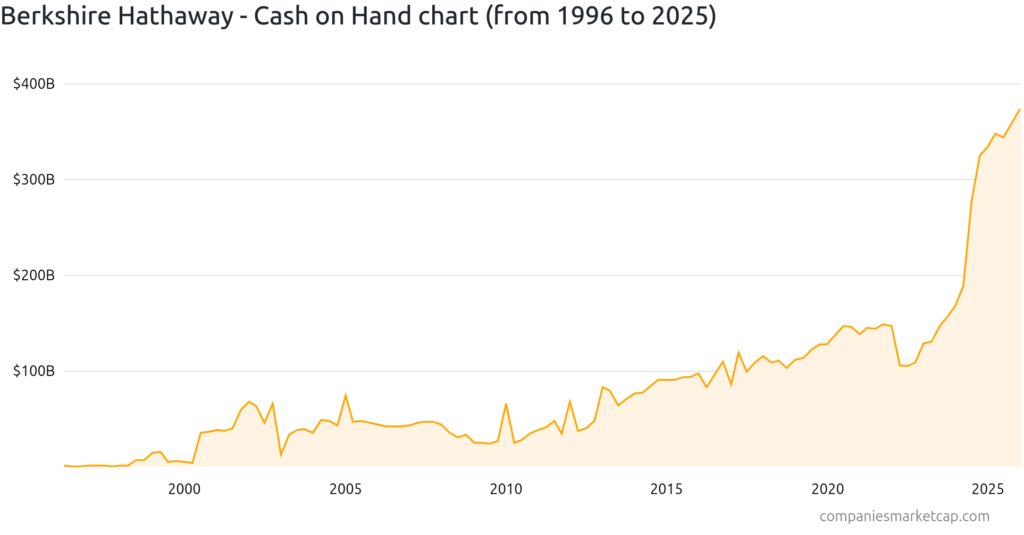

Periods of market stress often create opportunities to acquire high-quality assets at discounted prices. Investors with available capital are better positioned to take advantage of such situations.

This principle is exemplified by Berkshire Hathaway, which has historically maintained substantial cash reserves, allowing it to act decisively during periods of dislocation.

11. The Passive–Active Balance

Financial markets rely on a balance between passive and active participants. Passive investors provide efficiency and cost advantages, while active investors ensure that prices remain connected to fundamentals.

If passive investing becomes too dominant, the burden of maintaining market efficiency shifts to a shrinking group of active participants.

12. Corporate Governance and the Concentration of Ownership

An often-overlooked consequence of passive investing is the concentration of ownership in the hands of a few large asset managers. Firms such as Vanguard, BlackRock, and State Street collectively hold significant stakes in a large proportion of publicly listed companies.

Although these institutions are “passive” in their investment approach, they actively exercise voting rights on corporate matters. This creates a structural tension: decision-making power is concentrated in entities that do not actively select investments based on conviction.

The implications for corporate governance are complex. On one hand, these institutions can promote stability and long-term thinking. On the other, the concentration of voting power raises questions about accountability, incentives, and the extent to which corporate decisions reflect the interests of underlying investors.

13. Conclusion

Passive investing represents one of the most significant financial innovations of the modern era. It has lowered costs, simplified investing, and broadened access to financial markets.

However, its success also introduces second-order effects, including concentration risk, altered price formation, behavioral vulnerabilities, and potential systemic fragility.

At the individual level, passive investing can be highly effective when combined with discipline, knowledge, and sufficient liquidity. At the system level, its continued expansion raises important questions about how markets will function in the future.

Passive investing works best in a world where others remain active. Its long-term success may ultimately depend on not becoming too successful.