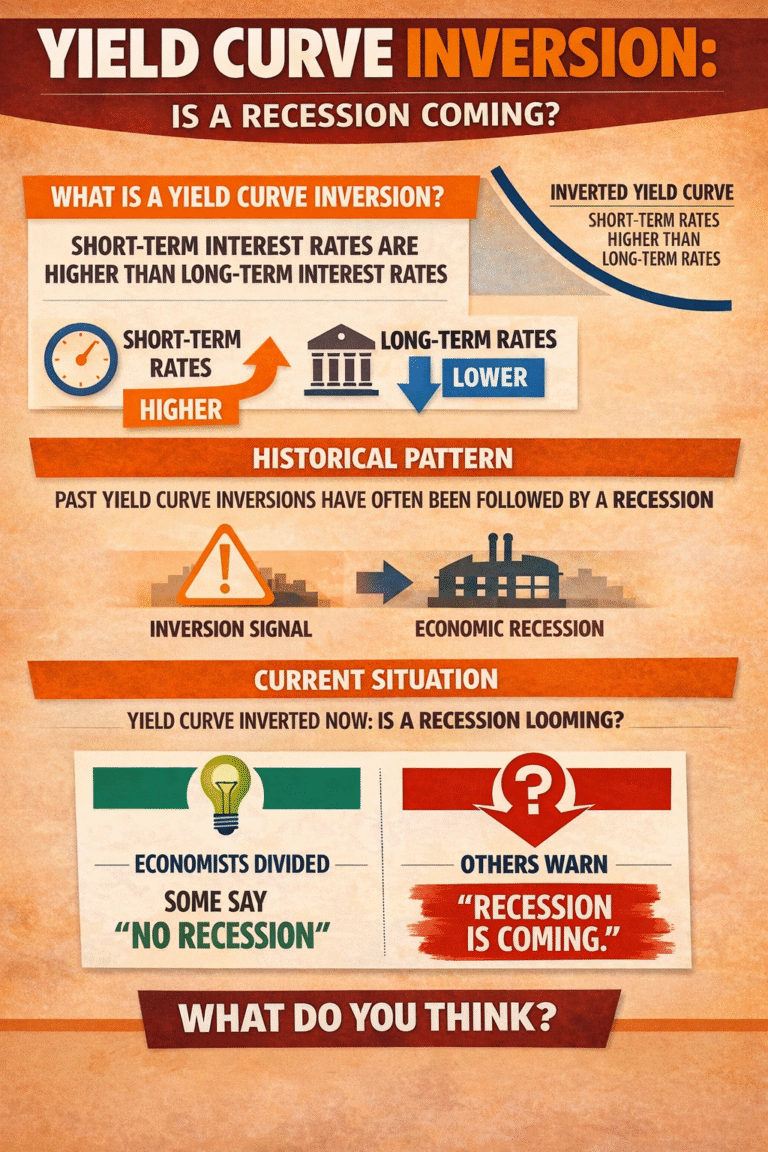

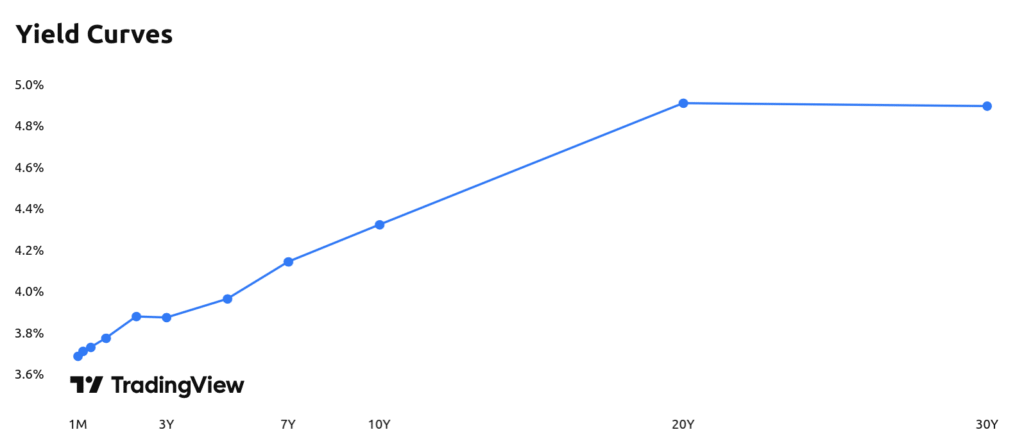

What is the yield curve?

The yield curve shows the relationship between interest rates (yields) and time to maturity for government bonds—typically U.S. Treasuries.

Under normal conditions:

- Long-term bonds (10-year) have higher yields

- Short-term bonds (2-year) have lower yields

This reflects:

- inflation expectations

- economic growth expectations

- risk premium over time

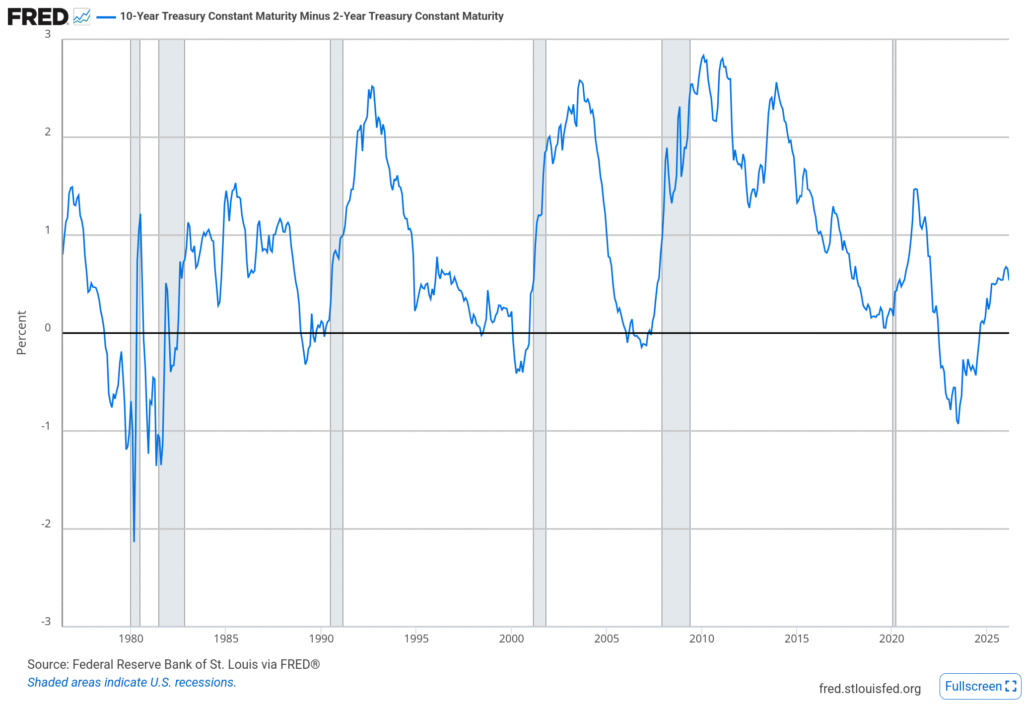

What is a yield curve inversion?

A yield curve inversion occurs when:

- short-term rates > long-term rates

In practice, the most commonly watched measure is:

- 2-year vs 10-year Treasury spread

👉 When this spread turns negative, the curve is inverted. Check the plot below!

Why does the yield curve invert?

There are two forces at play:

1. Central banks raise short-term rates

To fight inflation, central banks increase policy rates.

→ Short-term yields rise quickly

2. Markets expect slower growth ahead

Investors anticipate:

- weaker growth

- lower future inflation

- eventual rate cuts

→ Long-term yields stop rising or fall

👉 The result:

Short-term rates > long-term rates

→ inversion

Why does it predict recessions?

An inverted yield curve signals that:

- monetary policy is tight

- financial conditions are restrictive

- markets expect a slowdown

This leads to:

- reduced lending profitability for banks

- tighter credit conditions

- slower investment and consumption

👉 Which eventually leads to a recession.

Historical examples of yield curve inversions

Here are the most important recent cycles:

🔹 1989 Inversion → 1990 Recession

- Inversion: late 1988 – early 1989

- Recession: July 1990 – March 1991

👉 Lag: ~12–18 months

🔹 2000 Inversion → Dot-com Recession

- Inversion: 2000

- Recession: March 2001 – November 2001

👉 Trigger: tech bubble burst

🔹 2006–2007 Inversion → Global Financial Crisis

- Inversion: mid-2006 → mid-2007

- Recession: December 2007 – June 2009

👉 One of the clearest signals in modern history

🔹 2019 Inversion → Pandemic Recession

- Inversion: August 2019

- Recession: February 2020 – April 2020

👉 Special case: shock-driven recession (COVID), but signal still valid

🔹 2022–2024 Inversion → ? (ongoing cycle)

- Inversion began: mid-2022

- Deepest inversion: 2023–2024

👉 Still being debated:

- delayed recession?

- or structural changes?

What about “uninversion”?

This is where it gets really interesting—and often misunderstood.

What is uninversion?

The yield curve returns to normal shape:

- long-term rates > short-term rates again

But this usually happens because:

- central banks start cutting rates

- short-term yields fall quickly

Why uninversion matters more than inversion

Historically:

👉 Recessions often begin after the curve steepens again, not at the moment of inversion.

Examples:

- 2000: curve steepened → recession followed

- 2007: steepening preceded the crisis

- 2020: steepening before COVID recession

“The inversion is the warning. The steepening is often the trigger.”

Limitations of the yield curve

No indicator is perfect. Check here a related article on recession indicators.

1. Timing is uncertain

- Lag can vary from 6 to 24 months

2. False signals (rare but possible)

- Some inversions did not lead to immediate recessions

3. Structural changes

- QE, global demand for bonds, and central bank policies may distort signals

How to use it in practice

The yield curve works best when combined with:

- interest rate trends

- credit conditions

- labor market data

Subscribe below to be notified each time we publish new material!