And Why Banks Matter More Than You Think

Intro

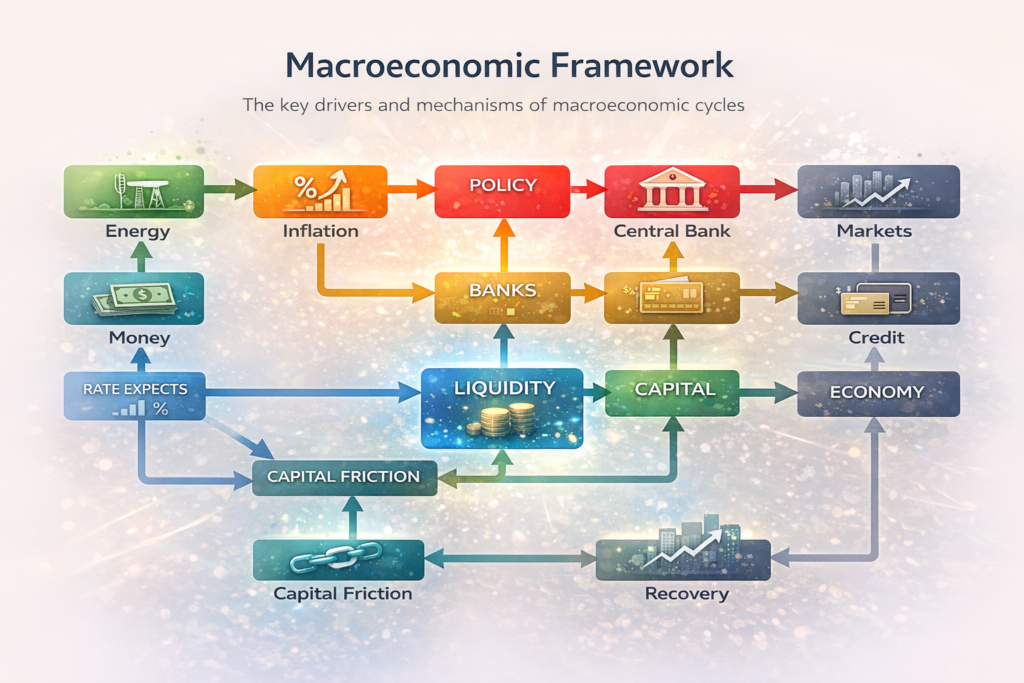

Economic cycles are often described in terms of growth, inflation, and recessions. But underneath these cycles lies a more fundamental mechanism: the cost and availability of credit

At the center of this system are:

- central banks, which set the price of money

- and commercial banks, which decide how much credit is actually created

Understanding how these two interact is key to understanding why booms turn into recessions—and vice versa.

The Core Idea: The Economy Runs on Credit

Modern economies are not just driven by productivity or demand—they are driven by credit creation.

When credit is:

- expanding → growth accelerates

- contracting → the economy slows

And this is where interest rates come in.

Step 1: Central Banks Set the Price of Money

Central banks (like the Federal Reserve or the European Central Bank) control short-term interest rates.

They adjust rates based on two main goals:

- control inflation

- stabilize economic growth

When inflation rises:

- central banks raise rates

When growth weakens:

- central banks cut rates

Step 2: Banks Decide Whether Credit Actually Flows

This is the part many people miss.

Central banks set the price of money, but banks control the supply of credit.

Banks decide:

- who gets a loan

- at what risk

- under what conditions

This is why: “The economy doesn’t run on interest rates alone—it runs on lending.”

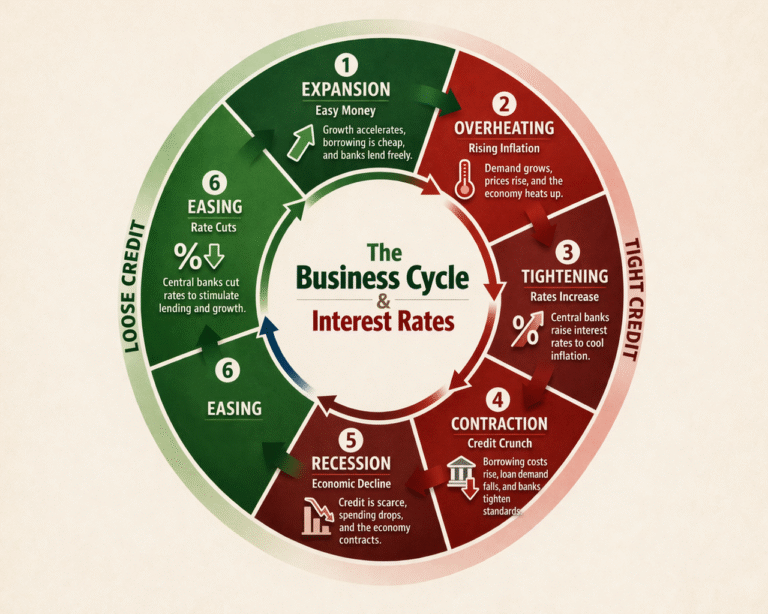

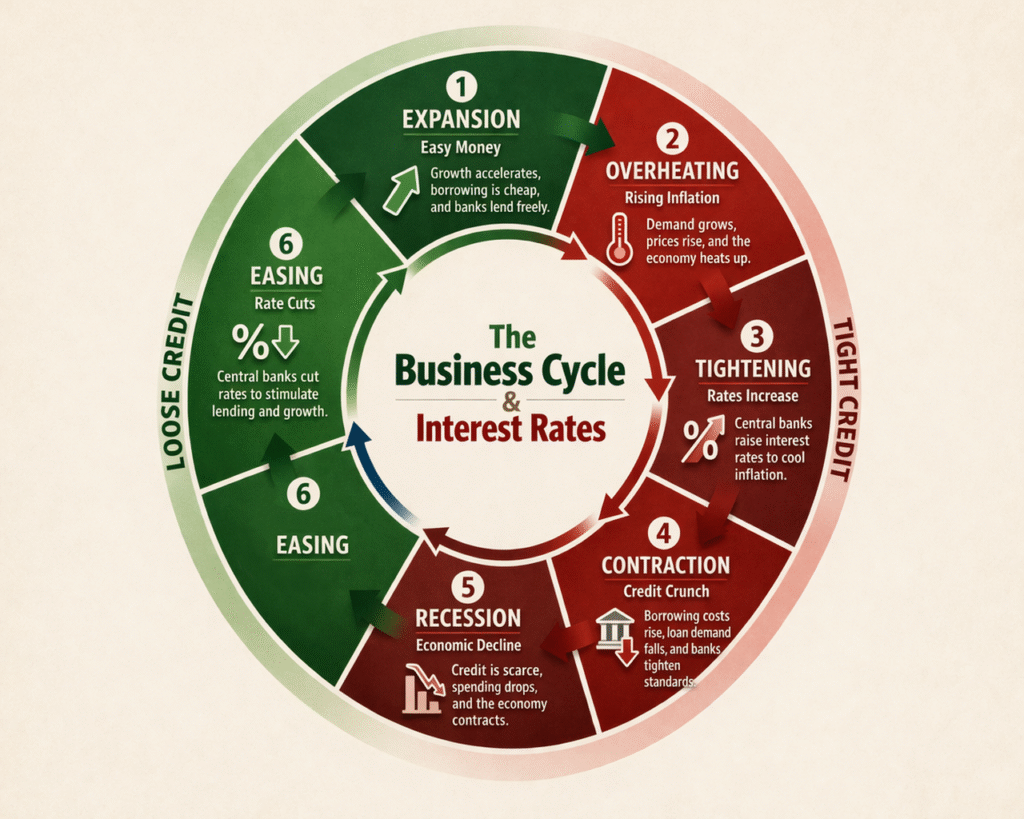

The Business Cycle Through Credit

Let’s walk through the full cycle.

🟢 Phase 1: Easy Money (Expansion)

- Interest rates are low

- Credit is cheap

- Banks are willing to lend

This leads to:

- rising investment

- higher consumption

- asset price increases

Growth accelerates

🔴 Phase 2: Overheating & Inflation

As the economy expands:

- demand increases

- inflation rises

Central banks respond by:

- raising interest rates

🟠 Phase 3: Monetary Tightening

Higher rates begin to bite:

- borrowing costs increase

- loan demand declines

- banks become more cautious

This is where things start to change:

👉 Credit growth slows

🔻 Phase 4: Credit Contraction

This is the critical turning point.

- banks tighten lending standards

- risk appetite drops

- refinancing becomes harder

This affects:

- businesses (investment slows)

- households (spending declines)

👉 Economic activity weakens

⚫ Phase 5: Recession

At this stage:

- credit is constrained

- demand falls

- unemployment rises

This is where the labor market indicator kicks in (lagging indicator).

🔵 Phase 6: Policy Response (Easing)

Central banks react by:

- cutting interest rates

- trying to stimulate lending

In some cases, they also use tools like:

- asset purchases (QE)

- liquidity support

👉 The goal: restart the credit cycle

Why Banks Are the Transmission Mechanism

Interest rates don’t directly control the economy. Instead, they work through bank balance sheets.

When rates rise:

- borrowing costs increase

- defaults risk rises

- banks become more conservative

When rates fall:

- lending becomes attractive again

- risk appetite slowly returns

Key Insight

“Central banks set the direction, but banks determine the speed and strength of the cycle.”

Why Tightening Often Leads to Recessions

Central banks don’t aim to cause recessions—but it often happens because:

- tightening works with a lag

- credit conditions can shift abruptly

- financial systems are fragile at turning points

This is why:

👉 Most recessions are preceded by aggressive tightening cycles

A Note on Unconventional Policies

In recent decades, central banks have gone beyond traditional rate changes.

Examples include:

- large-scale asset purchases

- balance sheet expansion

- attempts to influence longer-term rates

In some cases (like Japan), central banks have even tried to directly control parts of the yield curve.

👉 These policies aim to:

- stabilize markets

- support lending

- prevent deep recessions

This topic will later be expanded in a dedicated article

How This Fits Into the Bigger Picture

This is a possible chain reaction that can lead to a recession:

- Oil shocks → inflation → rate hikes

- Rate hikes → credit tightening

- Credit tightening → recession

👉 This is the full macro chain.

Final Thoughts

The business cycle is not random—it is largely driven by the interaction between:

- central bank policy

- and private sector credit creation

Interest rates are the starting point. But it is credit conditions, shaped by banks, that ultimately determine whether the economy expands or contracts.