Why writing about passive investing has become the best passive income strategy

Over the past few years, the supply of financial advice has quietly exploded.

Not just institutional research or traditional media, but a parallel ecosystem: YouTube channels, newsletters, Discord groups, online courses, “macro explainers,” real estate playbooks, crypto frameworks, and an ever-growing shelf of investing books authored by people most readers had never heard of five years ago.

At first glance, this looks like progress—financial education becoming more accessible, markets becoming more democratic.

But the timing is not random.

This proliferation tends to accelerate late in the cycle, when the nature of opportunity begins to change.

From extracting alpha to extracting attention

In early-cycle environments, returns are relatively easy to generate. Liquidity expands, valuations re-rate, and broad exposure does most of the work. You do not need a complex framework to make money—being positioned is often enough.

Late in the cycle, that changes.

Opportunities compress. Dispersion increases. Edges become smaller, more technical, and harder to scale. Generating excess returns—true alpha—requires differentiated information, speed, or structural advantages – and those do not scale well. Content does.

A portfolio strategy can only absorb so much capital before its returns degrade. A YouTube video or a “passive income” guide, on the other hand, has near-zero marginal cost and effectively infinite distribution.

At that point, the rational economic shift is subtle but powerful:

When extracting alpha becomes harder, extracting attention becomes more profitable.

The passive income paradox

This is where the narrative turns.

“Passive income” becomes the dominant theme precisely when it is hardest to achieve.

Real passive income—durable, scalable, low-effort cash flow—is constrained. If widely accessible, it tends to be arbitraged away. Rental yields compress. Dividend strategies become crowded. Even historically successful investing styles lose effectiveness once they become universally adopted.

The mechanism is simple – let’s look at an example:

Suppose an apartment generates €12,000 per year in rent and is selling for €120,000. The rental yield is:

If similar properties normally yield 5–6%, investors quickly notice the opportunity. More buyers will enter that market seeking for a higher return. Competition pushes the property price upward. If the apartment eventually rises to €240,000 while rents remain unchanged, the yield falls accordingly:

The same dynamic applies to dividend stocks, bond spreads, and many popular “income” strategies. High returns attract capital, and capital itself gradually erodes the opportunity.

This is one of the most important mechanisms in finance:

Unusually high returns rarely remain unusually high once they become widely recognized.

Yet content about passive income scales effortlessly. Writing about dividend investing, rental portfolios, or option income strategies requires no balance sheet. Packaging the idea is often easier than executing it. And importantly, the audience is vast: a large base of individuals seeking financial autonomy without proportional increases in complexity or risk.

The result is a paradox:

One of the most effective passive income strategies is producing content about passive income.

A generation shaped by extraordinary returns

Part of the phenomenon may also reflect historical conditioning. Over the last four decades, investors operated in an unusually favorable macroeconomic backdrop. Inflation and interest rates declined structurally from the early 1980s onward, supporting both equity valuations and bond prices simultaneously. Falling financing costs boosted real estate, while globalization and abundant liquidity supported corporate profitability.

For long stretches, passive exposure worked exceptionally well. A broad equity index, a leveraged rental property, or a diversified bond portfolio often generated attractive returns with relatively little sophistication. Entire generations of investors became accustomed to an environment where asset prices generally moved upward over time.

The danger comes when temporary macroeconomic conditions are mistaken for permanent investing laws.

Late-cycle behavior often emerges precisely when investors extrapolate past returns indefinitely into the future.

When education becomes product

None of this implies that financial education is inherently low quality – it is necessary – but incentives matter. As the space becomes more crowded, content increasingly competes on engagement rather than accuracy. Certainty tends to outperform nuance. Strong narratives outperform probabilistic thinking. Predictions outperform conditional scenarios.

Over time, part of the ecosystem shifts from education to productization:

- Courses promising actionable frameworks

- Memberships offering “high-conviction ideas”

- Communities monetizing access rather than insight

The same tools that democratized investing have also democratized the ability to sell investing.

And in many cases, the economics of selling financial content are superior to the economics of applying the underlying strategy at scale.

The illusion of scalable edge

A useful way to think about this is through scalability. If a strategy is truly robust and capacity-constrained, broadcasting it widely tends to reduce its effectiveness. This is well understood in institutional investing, where alpha is treated as a scarce resource. Yet much of the retail-facing content ecosystem implicitly assumes the opposite: that profitable strategies can be infinitely shared without degradation.

History suggests otherwise. Dividend investing became increasingly crowded during the post-2008 search for yield, pushing many “safe” income stocks to historically expensive valuations. Real estate investing evolved from a niche business into a mass-market aspiration amplified by social media, compressing rental yields in many cities. More recently, option-income products and covered-call ETFs surged in popularity as investors searched for yield regardless of underlying market conditions.

The same pattern appears repeatedly:

- A strategy performs well

- Capital floods into it

- Valuations rise

- Future returns decline

Even systematic trading strategies face similar pressures. A market inefficiency may persist when only a few participants exploit it, but once thousands of traders and algorithms pursue the same signals, the edge often disappears faster.

If everyone knows the shortcut, it eventually stops being one.

A late-cycle signal

Taken together, the proliferation of financial gurus is less about individual credibility and more about systemic conditions.

It reflects:

- A saturation of straightforward opportunities

- A large audience conditioned by prior gains

- A shift from return generation to narrative monetization

In that sense, the signal is not simply that people are talking about markets. It is that so many people are building businesses around explaining how to succeed in them.

Historically, similar dynamics tend to emerge near peaks in speculative cycles—not as precise timing tools, but as behavioral indicators.

When participation broadens, narratives simplify, and the business of investing increasingly migrates from portfolios to platforms, the underlying environment is usually no longer early-cycle optimism. It is often late-cycle enthusiasm.

Attention follows performance

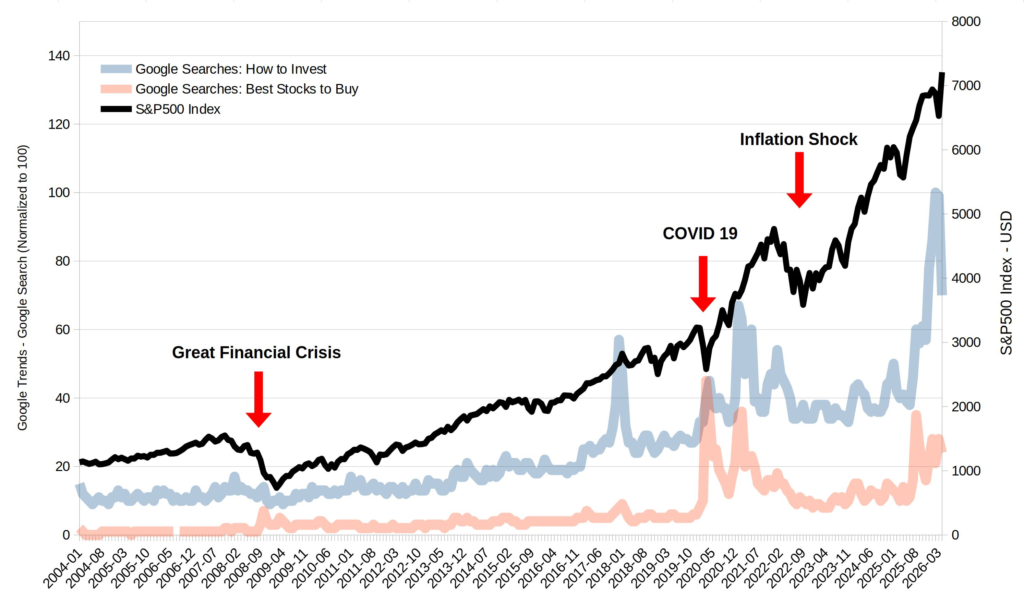

One of the clearest signs of speculative participation is that public attention tends to follow price rather than precede it.

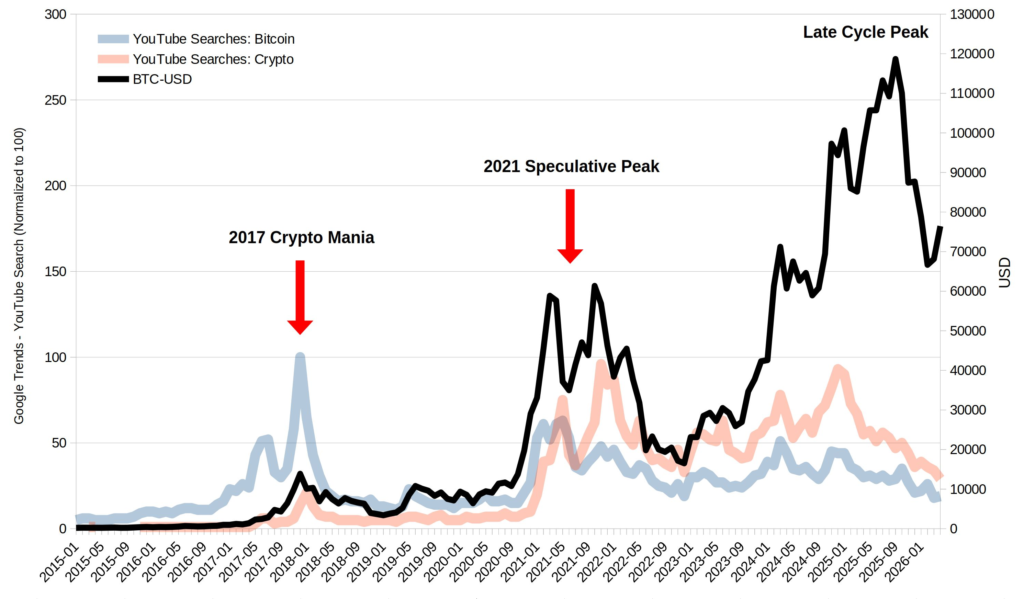

Google Trends data illustrates this dynamic clearly. Searches related to investing and crypto speculation tend to accelerate during or after major price advances, not before them.

In equities, searches such as “best stocks to buy” often spike after sharp market drawdowns or during recoveries, reflecting a reactive search for opportunity once volatility becomes visible. Meanwhile, broader queries such as “how to invest” have trended structurally upward over the last decade, suggesting a gradual expansion of retail participation and financial curiosity.

The post-2022 inflation shock may also have reinforced the perception that participation in financial markets is no longer optional. As purchasing power eroded and housing affordability deteriorated, investing increasingly became viewed not merely as wealth accumulation, but as a necessary tool for long-term financial stability.

The pattern is even more pronounced in crypto markets. YouTube searches for “bitcoin” and “crypto” closely track major price cycles, particularly during the speculative peaks of 2017 and 2021. Retail attention surged alongside price appreciation, reinforcing the feedback loop between market performance, media coverage, and public participation.

In speculative environments, price appreciation itself becomes marketing. That dynamic matters because rising search interest creates incentives for:

- more content creators

- more courses and memberships

- more prediction-driven commentary

- more simplified narratives around wealth creation

As speculative enthusiasm expands, an entire ecosystem emerges to monetize it.

Implications

For investors, the takeaway is not to disengage from financial content altogether, but to recalibrate expectations.

Most content is useful as:

- A summary of news

- A way to map prevailing narratives

- A reflection of sentiment

It is far less reliable as a source of differentiated edge.

True alpha, where it exists, tends to be:

- Capacity-constrained

- Information-sensitive

- Difficult to communicate at scale

Which is precisely why it is rarely packaged as mass-market content.

Closing thought

Late in the cycle, markets do not just inflate asset prices—they inflate financial narratives.

And when making money becomes harder, explaining how to make money quietly becomes one of the more scalable trades available.