Why Credit Conditions Matter: The Hidden Signals Behind Economic Stress

Economic downturns rarely begin with obvious signals like rising unemployment. Instead, stress tends to emerge quietly—within the financial system itself.

One of the most important but often overlooked areas is credit conditions.

These determine how easily households and businesses can access financing—and when they tighten, the economy often follows.

What Are Credit Conditions?

Credit conditions refer to:

- how easy it is to borrow

- how expensive borrowing is

- how much risk lenders are willing to take

They are influenced by:

- interest rates

- market sentiment

- bank balance sheets

- financial system stress

Key idea

“Credit conditions are where monetary policy meets the real economy.”

Why Credit Conditions Drive the Cycle

Even if central banks cut or raise rates, what matters is:

Do banks and markets actually lend?

When credit is:

- loose → growth accelerates

- tight → the economy slows

This is why credit often leads the business cycle.

Key Indicators to Track Credit Conditions

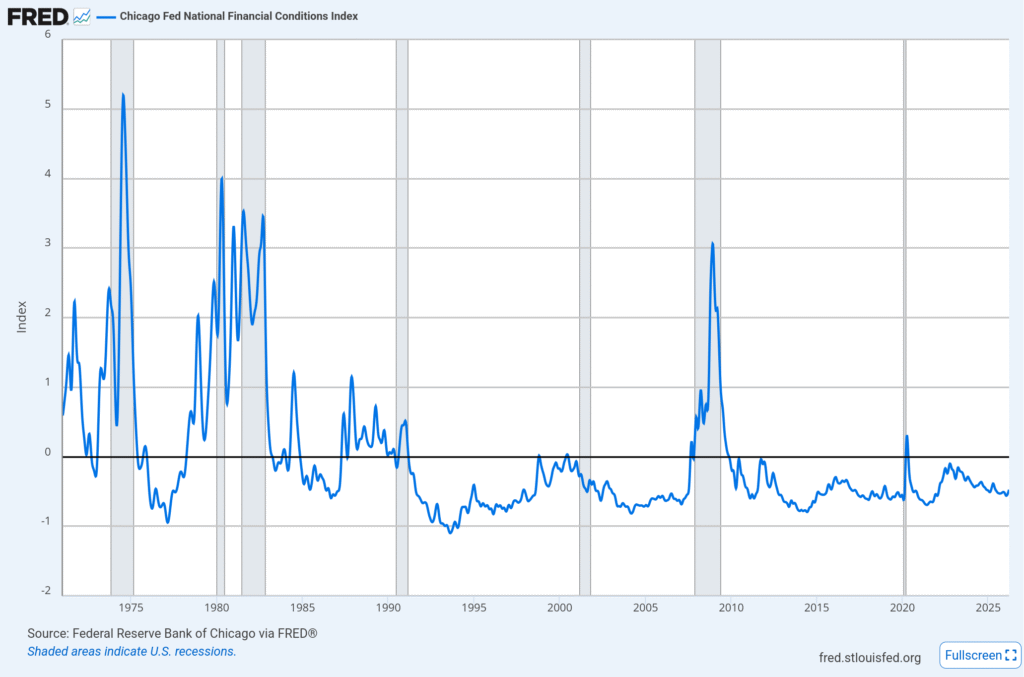

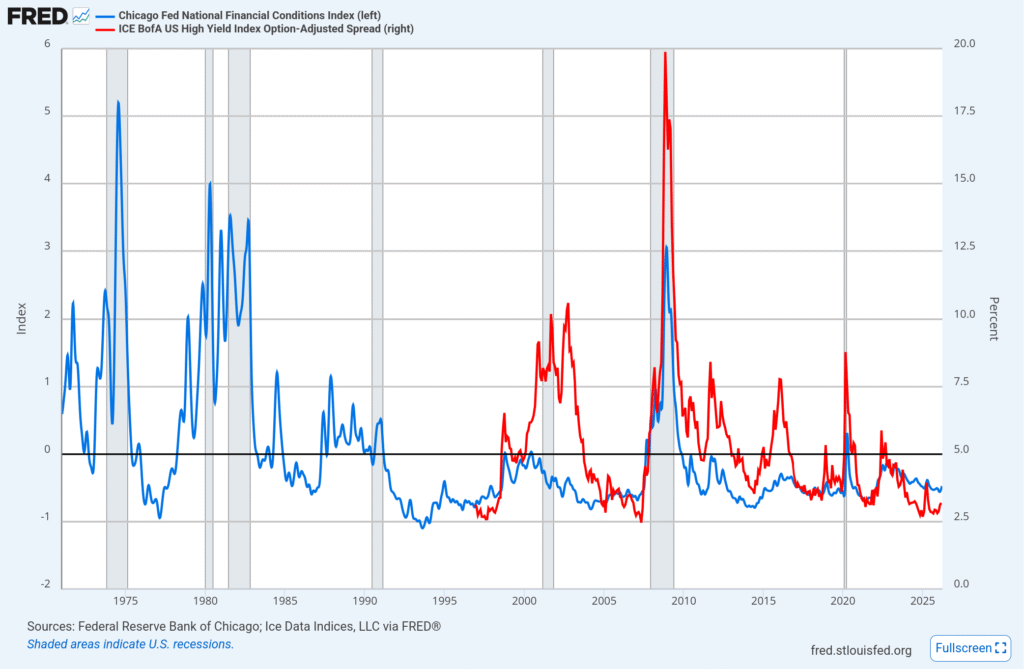

1. Financial Conditions Index (NFCI)

The Chicago Fed National Financial Conditions Index is one of the most comprehensive measures.

What it includes:

- interest rates

- credit spreads

- leverage

- market volatility

How to read it:

- Below 0 → loose financial conditions

- Above 0 → tight financial conditions

Why it matters:

It captures system-wide stress, not just one market.

2. Credit Spreads (High Yield vs Treasuries)

One of the most important real-time indicators is the spread between high-yield (junk) bonds and government bonds

This is often tracked using indexes like the ICE BofA US High Yield Index Option-Adjusted Spread.

What it shows:

- investor risk appetite

- perceived default risk

Typical behavior:

- Spreads narrow (low) → confidence, easy credit

- Spreads widen (high) → stress, tightening

During crises:

- spreads spike sharply (e.g. 2008, 2020)

3. Bank Lending Standards

Banks periodically report whether they are tightening or loosening lending standards.

A key source is:

- the Senior Loan Officer Opinion Survey

What to watch:

- % of banks tightening credit

Why it matters:

This is often an early signal of recession risk.

4. Real Interest Rates

Not just nominal rates—but inflation-adjusted rates.

When real rates are:

- rising → borrowing becomes more restrictive

- high → pressure builds on borrowers

This is especially important in:

- housing

- corporate debt

5. Liquidity & Market Functioning

In stressed environments:

- liquidity dries up

- bid-ask spreads widen

- markets become less efficient

Even small shocks can have outsized effects.

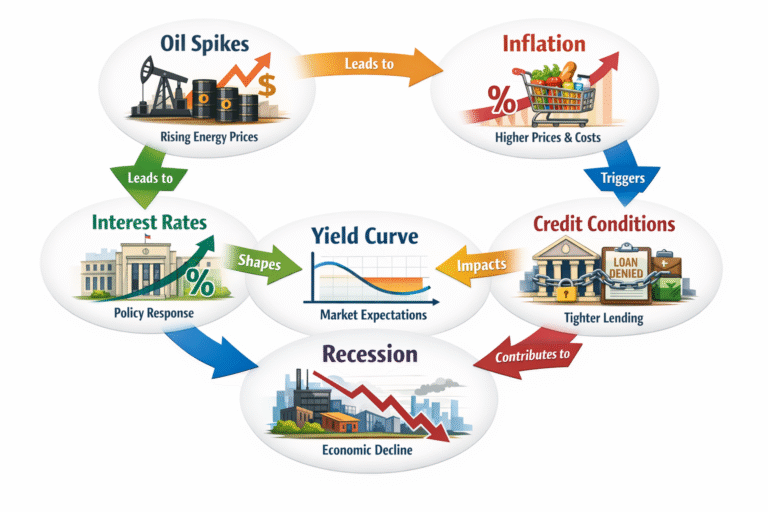

How Credit Tightening Leads to Recession

Here’s the mechanism:

- Interest rates rise

- Credit spreads widen

- Banks tighten lending

- Borrowing declines

- Investment and consumption fall

- Economy slows → recession

Strong takeaway

“Recessions don’t start when unemployment rises—they start when credit quietly stops flowing.”

Historical Examples

2008 Global Financial Crisis

- Credit spreads exploded

- Banks stopped lending

- Financial system stress triggered deep recession

2020 COVID Shock

- Spreads widened rapidly

- Liquidity evaporated

- Central banks intervened aggressively

2022–2024 Cycle

- Rising rates

- gradual tightening in credit

- stress emerging in parts of the system

Why Credit Is the Most Important Indicator

Compared to other indicators:

- Yield curve → expectations

- Labor market → lagging

- Inflation → noisy

Credit conditions:

- reflect real stress

- affect real activity

- move early

Final Thoughts

If you want to understand where the economy is heading, don’t just look at growth or inflation.

Look at: how easy it is to borrow. Because when credit tightens, everything else tends to follow.