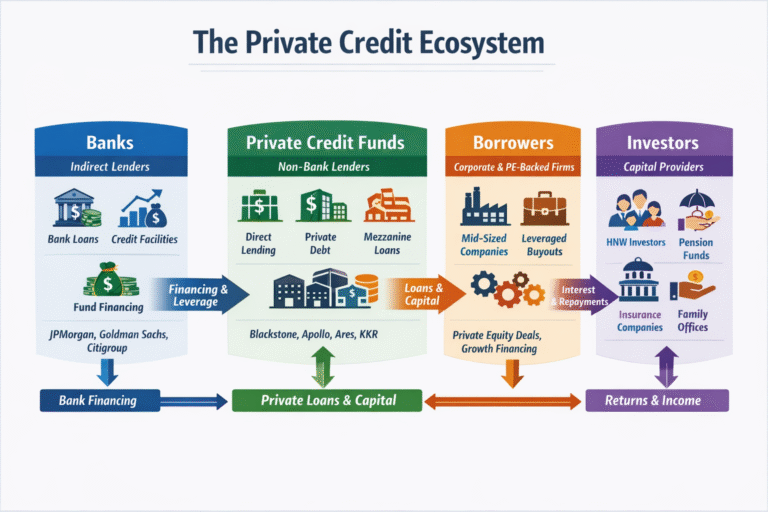

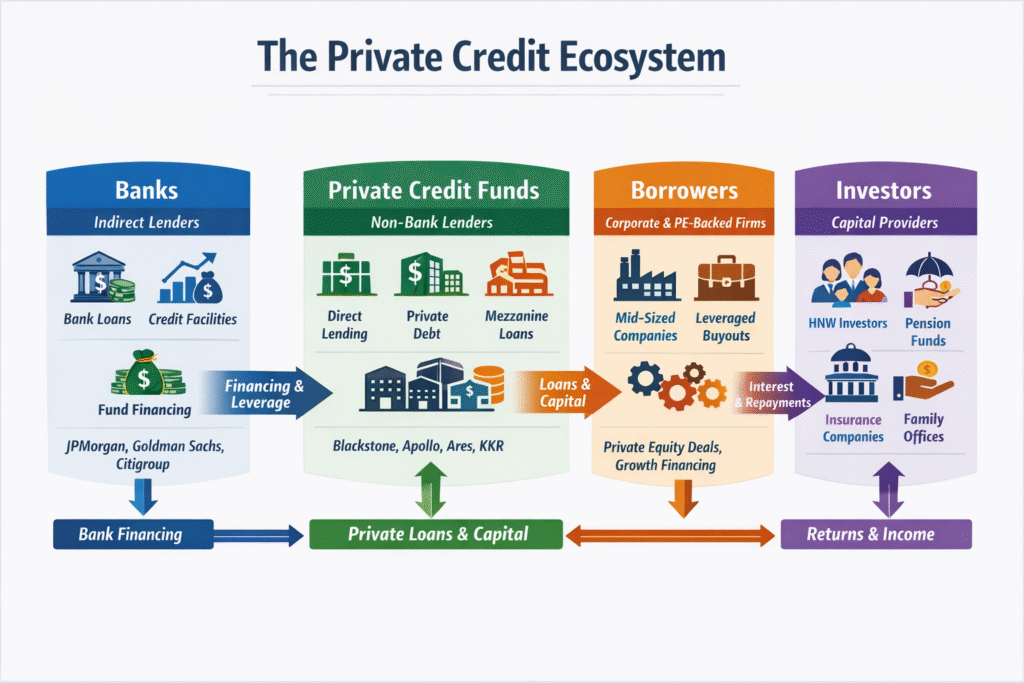

Private credit is no longer a niche corner of finance. Large firms such as Blackstone, Apollo, and Ares now manage hundreds of billions in private loans, while semi-liquid funds like BCRED and Apollo Debt Solutions are increasingly accessible to a broader range of investors.

Private credit has grown rapidly over the past decade, becoming one of the most important—and least understood—segments of global finance.

Originally dominated by institutional investors, it is now increasingly accessible to a broader audience through semi-liquid funds and wealth platforms.

But as the asset class expands, so do concerns about:

- liquidity

- transparency

- valuation

- and systemic risk

Recent developments in 2025–2026 suggest that private credit may be entering a more fragile phase.

What Is Private Credit?

Private credit refers to loans made outside the traditional banking system, typically by:

- private funds

- asset managers

- direct lending vehicles

These loans are often:

- made to mid-sized or leveraged companies

- structured privately (not traded on public markets)

- held to maturity

Key Difference vs Bank Lending

Traditional banks:

- originate loans

- hold them (or syndicate them)

- are tightly regulated

Private credit funds:

- originate and hold loans

- operate with less regulatory oversight

- rely on investor capital

But Banks are Still Involved

This is crucial—and often overlooked.

Banks still:

- lend to private credit funds

- provide credit lines

- finance deal pipelines

In fact, U.S. banks had hundreds of billions in exposure to private credit and private equity funds as of 2025

👉 This creates an indirect link between:

- private markets

- and the traditional banking system

Examples of Private Credit Players and Funds

Large Private Credit Firms (Institutional Leaders)

These firms dominate the private credit space and manage hundreds of billions in assets:

- Blackstone → one of the largest players globally

- Apollo Global Management → strong focus on direct lending and structured credit

- Ares Management → major direct lending platform

- KKR → active across private credit and leveraged finance

- Carlyle Group → growing private credit business

These firms typically lend to:

- mid-sized companies

- leveraged buyouts

- private equity-backed firms

Semi-Liquid / Retail-Oriented Private Credit Funds

- Blackstone Private Credit Fund (BCRED)

- Apollo Debt Solutions BDC

- Ares Strategic Income Fund

- Blue Owl Credit Income Corp

Key characteristics:

- offer periodic liquidity (monthly/quarterly)

- invest in illiquid loans

- increasingly marketed to wealth clients

Business Development Companies (BDCs)

BDCs are publicly listed vehicles that give exposure to private credit:

- Main Street Capital

- Ares Capital Corporation

- FS KKR Capital Corp

These are useful because:

- they trade publicly

- you can observe discounts to NAV (important signal)

Banks (Indirect Exposure)

Even though private credit is “non-bank lending,” traditional banks are still involved:

- JPMorgan Chase

- Goldman Sachs

- Citigroup

They provide:

- financing to funds

- credit lines

- deal structuring

This is where systemic risk transmission can occur.

Why Private Credit Grew So Fast

Several structural forces drove the boom:

- tighter banking regulation after 2008

- companies staying private longer

- demand for higher yields

The result:

👉 a market that grew to around $3 trillion in 2025, with projections toward $5 trillion by 2029

Key Risks in 2026

1. Liquidity Risk (The Biggest One)

Private credit is fundamentally illiquid.

- loans are not actively traded

- exits depend on refinancing or maturity

Recent events highlight this risk:

- Funds have capped investor withdrawals amid rising redemption requests

Some vehicles have gone further, suspending withdrawals entirely for years

👉 This creates a mismatch:

- investors expect periodic liquidity

- assets cannot be easily sold

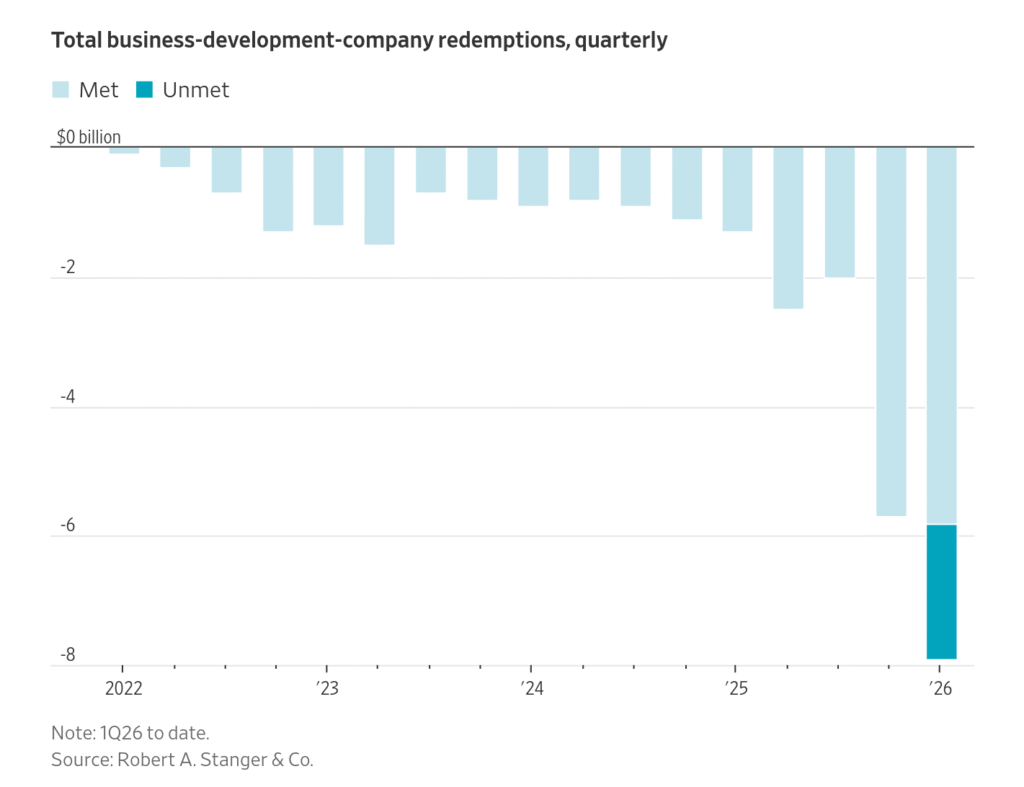

2. Redemption Pressure and “Gating”

In 2026, the industry is facing:

- rising redemption requests

- slowing fundraising

More than $11 billion was withdrawn from private credit funds in recent months

To manage this:

- funds impose withdrawal limits (e.g. 5% per quarter)

👉 Without these limits, outflows would likely be much larger.

3. Valuation Opacity

Unlike public bonds:

- private loans are not marked daily

- valuations rely on internal models

This raises concerns about:

- stale pricing

- delayed recognition of losses

Markets are already reacting:

- many listed private credit vehicles trade below their stated asset values

👉 This suggests investors may not fully trust reported valuations

4. Rising Default Risk

While defaults remain moderate, they are rising:

- leveraged loan defaults reached ~5.5% in early 2026

some estimates suggest “true” default rates may be higher when restructuring is included

Additionally:

- forecasts expect further deterioration into 2026

5. Payment-in-Kind (PIK) Risk

One of the most subtle but important risks:

👉 borrowers paying interest with IOUs instead of cash

This has been increasing:

- up to 15–17% of income in some funds comes from PIK structures

This can indicate:

- borrower stress

- delayed defaults

6. Sector Concentration (Especially Tech)

Private credit is heavily exposed to:

- software

- asset-light companies

These sectors are vulnerable to:

- disruption (e.g. AI)

- weak collateral value

👉 In a downturn, recovery values may be low.

7. Liquidity Illusion for Retail Investors

A major emerging issue:

Many newer funds offer:

- periodic liquidity (monthly/quarterly redemptions)

But in reality:

- underlying assets remain illiquid

This creates a structural mismatch.

Some investors may not fully understand this risk—especially outside institutional circles

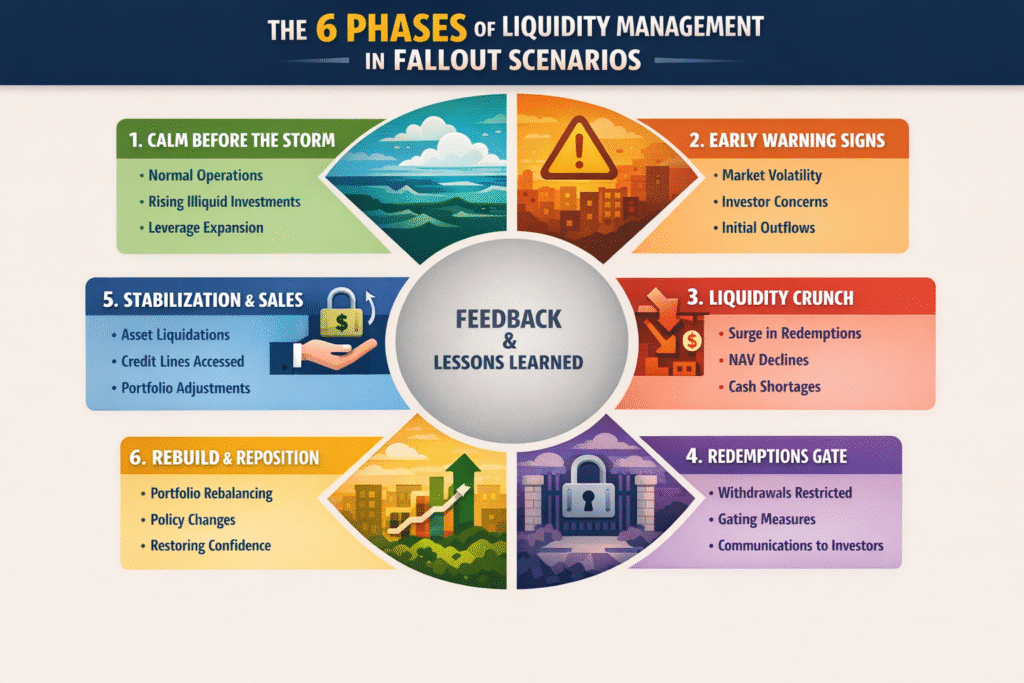

Market Signals in 2025–2026

Recent developments suggest stress is building:

- Bond spreads for private credit funds widened before redemption waves

- Large asset managers imposed withdrawal caps

- Investor confidence is weakening

Even experienced market participants are warning:

The system may be vulnerable to a “spark” after years of risk accumulation

Private Credit Funds Withholding or Limiting Withdrawals (2026)

1. Apollo Limits Withdrawals (March 2026)

- Apollo Global Management capped withdrawals in its $25bn Apollo Debt Solutions fund

- Redemption requests reached ~11%

- Only ~45% of requested capital was returned

👉 Classic example of:

- liquidity mismatch

- gating to avoid forced selling

2. BlackRock Restricts Withdrawals

- BlackRock limited withdrawals in a flagship private credit fund

- Investors requested $1.2bn, but only about half was paid

3. Industry-wide redemption caps (5% standard)

- Major firms including Ares Management and Apollo imposed 5% quarterly limits

- Investors withdrew $11+ billion in recent quarters

👉 This is key:

The system is not fully liquid—withdrawals are being managed

4. $4.6B+ “Trapped” Investor Capital

- Over $4.6 billion stuck behind withdrawal limits

- Investors waiting in queues to exit

“Investors are discovering that liquidity is conditional.”

5. Oaktree vs Others (Contrast Case)

- Oaktree Capital Management honored ~8.5% withdrawals

- Others enforced stricter caps

Useful nuance:

- not all funds behave the same

- but pressure is industry-wide

6. Early Warning Signals from Bond Markets

- Bonds of private credit funds started falling before redemptions surged

- Spreads widened across funds from:

- BlackRock

- Blackstone

- Blue Owl

- Ares

Take note: markets often detect stress before it becomes visible

Bankruptcies & Credit Stress Linked to Private Credit

1. First Brands (Auto Parts Supplier)

- Bankruptcy concerns surfaced in 2025–2026 cycle

- Linked to:

- leveraged financing

- private credit exposure

2. Tricolor (Subprime Auto Lender)

- Experienced funding stress and restructuring pressure

- Also tied to private credit exposure

3. Broader Pattern of Stress

Examples highlighted across the cycle:

- Collateral disputes (e.g. double-pledging concerns)

- Weak borrower quality in leveraged sectors

- Tech exposure (especially software companies)

4. Market Financial Solutions (2026 Collapse)

- London-based lender collapse cited as a private credit risk case

- Triggered concerns about systemic exposure

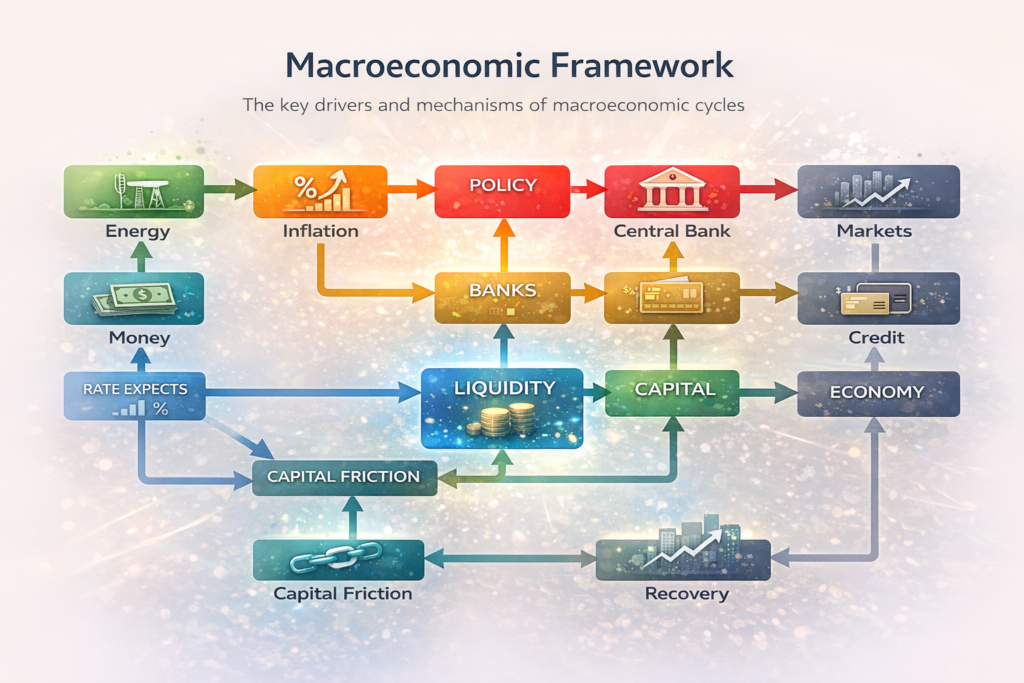

How This Fits Into the Macro Cycle

This connects directly to the broader macro view:

- Interest rates rise

- Credit conditions tighten

- Risk assets come under pressure

Private credit sits at the intersection of:

- credit risk

- liquidity risk

- valuation risk

Which makes it especially sensitive to tightening cycles.

Is This Systemic?

The debate is ongoing.

Bear case:

- opacity + leverage + liquidity mismatch

- potential contagion through banks

Bull case:

- defaults still contained

- risks are dispersed, not systemic

Final Thoughts

Private credit has become a core part of modern financial markets—but it remains structurally different from traditional credit.

In a world of tighter monetary policy and slowing growth:

👉 the key question is no longer yield

👉 but liquidity, transparency, and resilience