1. Intel and the Rise — and Erosion — of x86 Dominance

1.1 The Birth of Intel and the Modern Semiconductor Industry

Intel was founded in 1968 by Robert Noyce and Gordon Moore, two of the key pioneers of the semiconductor industry. Initially focused on memory chips, Intel gradually evolved into the dominant producer of microprocessors during the personal computer revolution of the 1980s and 1990s.

The launch of the Intel 4004 microprocessor in 1971 marked one of the foundational moments of the modern computing era. Over the following decades, Intel established itself as the dominant supplier of x86 processors powering personal computers, servers, and enterprise infrastructure across the global economy.

By the 1990s, Intel had become one of the most profitable and strategically important technology companies in the world. Its partnership with Microsoft created the so-called “Wintel” ecosystem that dominated desktop computing for decades.

At the core of Intel’s success was a business model that combined chip design, manufacturing, process engineering and in-house chip fabrication. Unlike many modern semiconductor companies, Intel owned and operated its own fabrication facilities (“fabs”). These fabs manufacture the physical silicon wafers on which chips are produced. Semiconductor fabrication is one of the most technologically complex and capital-intensive industrial activities in the global economy, requiring tens of billions of dollars in investment and continuous process upgrades.

For most of its history, Intel’s ownership of advanced fabs represented a major competitive advantage. The company controlled both processor architecture and manufacturing technology, allowing it to optimize performance and maintain industry-leading margins.

However, the structure of the semiconductor industry gradually changed.

1.2 The Rise of TSMC and the Foundry Model

Taiwan Semiconductor Manufacturing Company (TSMC) was founded in 1987 by Morris Chang with a radically different business model: instead of designing chips itself, TSMC would manufacture chips for external clients. This “pure-play foundry” model transformed the semiconductor industry.

Rather than spending enormous sums building fabrication plants, chip designers could outsource manufacturing to TSMC while focusing on architecture, software ecosystems, and product development. Over time, companies such as NVIDIA, Advanced Micro Devices (AMD), Qualcomm and Apple adopted so-called “fabless” business models, meaning they designed chips without owning the fabs that manufactured them. This distinction became increasingly important economically.

Modern fabs require immense capital expenditures, continuous upgrades, large engineering teams, and high operating costs. As semiconductor manufacturing complexity increased, owning fabs became both a strategic advantage and an enormous financial burden. TSMC benefited from scale economies by manufacturing chips for many customers simultaneously. Fabless firms, meanwhile, avoided the capital intensity associated with running their own manufacturing operations.

The divergence in profitability between fabless semiconductor firms and integrated manufacturers eventually became striking. For example, NVIDIA’s recent net profit margins exceeded 50% during the AI boom, while Intel’s margins deteriorated sharply during its restructuring and foundry expansion phase. The difference is not merely explained by product quality or market positioning; it is also deeply connected to capital intensity. NVIDIA designs chips and outsources manufacturing primarily to TSMC. Intel, by contrast, bears the immense fixed costs associated with designing, building, upgrading, and operating fabrication facilities. As the semiconductor industry evolved toward specialization, Intel increasingly found itself carrying a cost structure that many competitors no longer faced.

1.3 Intel’s Strategic Decline

Several events gradually weakened Intel’s historical dominance.

The smartphone revolution of the late 2000s shifted computing toward low-power ARM-based architectures, an area where Intel failed to establish leadership. Meanwhile, TSMC’s manufacturing capabilities improved rapidly, enabling fabless competitors such as AMD to produce increasingly competitive x86 processors.

AMD’s Ryzen and EPYC product lines, manufactured by TSMC, became major competitive threats in both consumer and server markets during the late 2010s.

Intel also experienced repeated manufacturing delays, particularly around advanced process nodes such as 10 nm. These delays damaged investor confidence and allowed competitors to close — and eventually surpass — Intel’s process technology leadership.

The symbolic turning point came in 2020, when Apple announced its transition away from Intel processors toward internally designed ARM-based silicon for Mac computers.

At roughly the same time, artificial intelligence emerged as the dominant growth theme within semiconductors. AI training and inference workloads relied heavily on graphics processing units (GPUs), an area overwhelmingly dominated by NVIDIA.

By the early 2020s, Intel was no longer perceived as the unquestioned leader of advanced computing. Instead, it increasingly appeared to investors as a former industry champion attempting to recover technological relevance amid profound structural changes in the semiconductor industry.

2. The Foundry Pivot and the Launch of IDM 2.0

2.1 The Introduction of IDM 2.0

In March 2021, shortly after returning as CEO, Pat Gelsinger introduced Intel’s “IDM 2.0” strategy, one of the most ambitious transformations in the company’s history.

The strategy had three primary objectives:

- Continue manufacturing Intel’s own chips internally,

- Increase use of external foundries such as TSMC where appropriate,

- Transform Intel into a contract manufacturer for external customers through Intel Foundry Services (IFS).

IFS was formally launched in 2021 as Intel’s attempt to compete directly with TSMC and Samsung in the merchant foundry business.

The timing was not accidental. The global semiconductor shortage during the COVID-era exposed the fragility of semiconductor supply chains and increased political concerns regarding dependence on Asian manufacturing capacity — particularly Taiwan.

Intel recognized an opportunity to reposition itself not merely as a CPU company, but as a strategic manufacturing platform for the United States and Europe.

2.2 Why Intel Pursued the Foundry Strategy

The logic behind Intel Foundry Services extended beyond simple diversification. By the early 2020s, TSMC had become the dominant advanced semiconductor manufacturer globally. Many of the world’s most important technology firms — including Apple, NVIDIA, AMD, and Qualcomm — relied heavily on TSMC for production. This concentration created geopolitical concerns, particularly given rising tensions involving Taiwan and China. The United States government increasingly viewed domestic semiconductor manufacturing capacity as strategically important. The CHIPS and Science Act later reinforced this trend by providing incentives for semiconductor investment within the United States.

Intel therefore attempted to position itself as:

- a domestic manufacturing champion,

- a geopolitical alternative to TSMC,

- and a critical supplier for the future AI infrastructure buildout.

2.3 Why Foundry Economics Are Difficult

Building a successful foundry business is extraordinarily difficult. Modern semiconductor fabs can cost tens of billions of dollars and require years before reaching efficient production levels. Profitability depends heavily on:

- manufacturing yields,

- utilization rates,

- customer trust,

- ecosystem integration,

- process reliability,

- and long-term contracts.

TSMC’s dominance was not built solely through superior technology. The company accumulated decades of trust within the semiconductor ecosystem. Customers designing advanced chips require confidence that manufacturing processes will remain stable and predictable over multi-year periods.

Intel faced the difficult challenge of simultaneously rebuilding process leadership, scaling new fabs, funding enormous capital expenditures, and convincing external clients to trust Intel Foundry Services. As a result, the transition has been imposing substantial pressure on Intel’s financial performance.

One of the most difficult challenges facing Intel is not merely technological, but reputational. In semiconductor manufacturing, process yield is critical. Yield refers to the percentage of functional chips produced from each silicon wafer. Even small differences in yield can dramatically impact profitability because advanced semiconductor manufacturing involves enormous fixed costs and highly complex production processes.

Leading-edge nodes are particularly difficult. As transistor dimensions shrink and manufacturing complexity increases, maintaining high yields becomes progressively harder. Delays, defects, or inconsistent production can quickly erode margins and undermine customer confidence.

This is where Intel faces one of its greatest structural disadvantages relative to TSMC. TSMC spent decades building a reputation for reliable execution, stable production, and predictable yields across multiple technology generations. For customers designing chips that may require years of development and billions of dollars in downstream products and infrastructure, manufacturing reliability is essential.

A failed product launch or manufacturing issue can have enormous financial consequences for semiconductor customers. As a result, foundry relationships tend to be highly trust-dependent and relatively sticky. Once customers commit to a manufacturing ecosystem, switching suppliers becomes difficult, costly, and risky.

Intel’s repeated manufacturing delays during the 10nm transition materially damaged that trust. The company’s difficulties in maintaining process leadership during the late 2010s created a perception that Intel was no longer the industry’s most reliable advanced-node manufacturer. Meanwhile, competitors such as AMD benefited indirectly by leveraging TSMC’s increasingly mature process technology.

Today, Intel is attempting to reverse that perception through aggressive development of advanced nodes such as Intel 18A. However, the challenge extends beyond technical capability alone. Intel must convince potential customers that yields will remain competitive, timelines will be reliable, supply commitments will be honored, and process performance will be sufficiently stable for large-scale production.

This may partially explain why markets react strongly to reports involving companies such as NVIDIA, Apple, Microsoft, or Amazon engaging with Intel Foundry Services. Such agreements are not merely potential revenue opportunities; they also function as ecosystem validation signals.

In many ways, Intel’s turnaround therefore depends not only on rebuilding manufacturing capability, but also on rebuilding trust.

3. Financial Deterioration and the Collapse in Sentiment

3.1 Revenue and Margin Compression

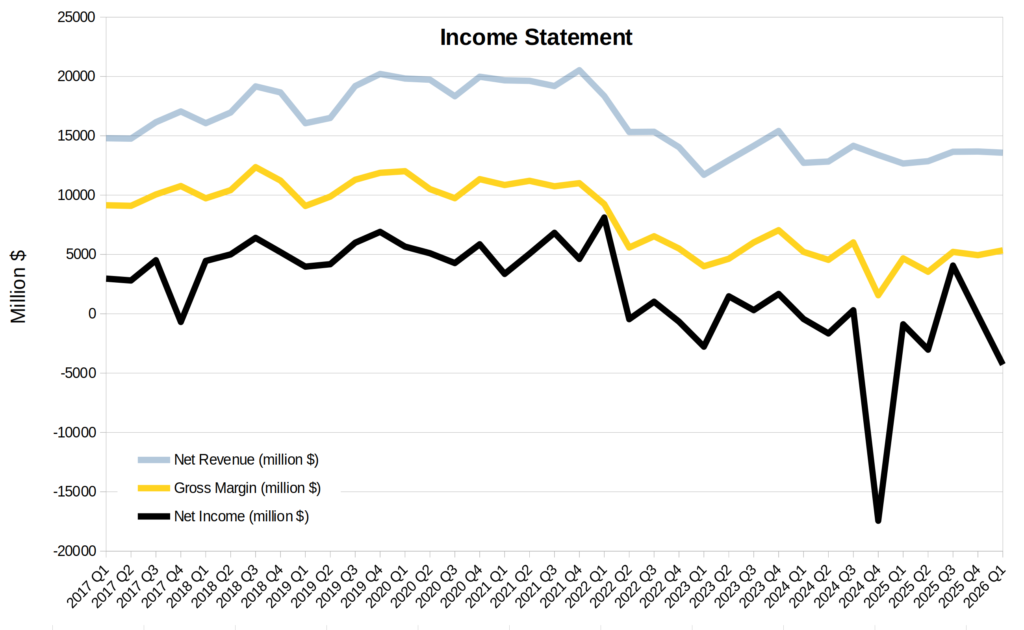

Intel’s financial deterioration accelerated sharply after 2021. In 2021, Intel generated approximately $79 billion in revenue with gross margins near historical norms above 55%. However, over the following years, both revenue and profitability declined substantially.

By June 2022, the management proceeds with dramatic actions to keep liquidity under stressful conditions (copied from the earnings release presentation of Q2 2022):

“We announced the planned implementation of cost-reduction measures, including reductions in headcount, other operating expenditures, capital expenditures, and cost of sales. These initiatives are designed to accelerate profitable growth, enable further operational efficiency and agility, and create capacity for sustained investment in technology and manufacturing leadership.”

“Our Board of Directors declared a Q3 2024 dividend of $0.125 per share on our common stock consistent with prior quarters. We announced our Board of Directors suspended the declaration of dividends on our common stock starting with Q4 2024, recognizing the importance of prioritizing liquidity to support the investments needed to execute our strategy. The Board of Directors reiterated our long-term commitment to a competitive dividend as cash flows improve to sustainably higher levels.“

“As part of our SCIP program, we completed a transaction with Apollo Global Management, Inc. (Apollo), under which Apollo led an investment of $11.0 billion to acquire a 49% equity interest in an entity related to our Fab 34 in Leixlip, Ireland. Fab 34 is our leading-edge high-volume manufacturing (HVM) facility designed for wafers using the Intel 4 and Intel 3 process technologies.”

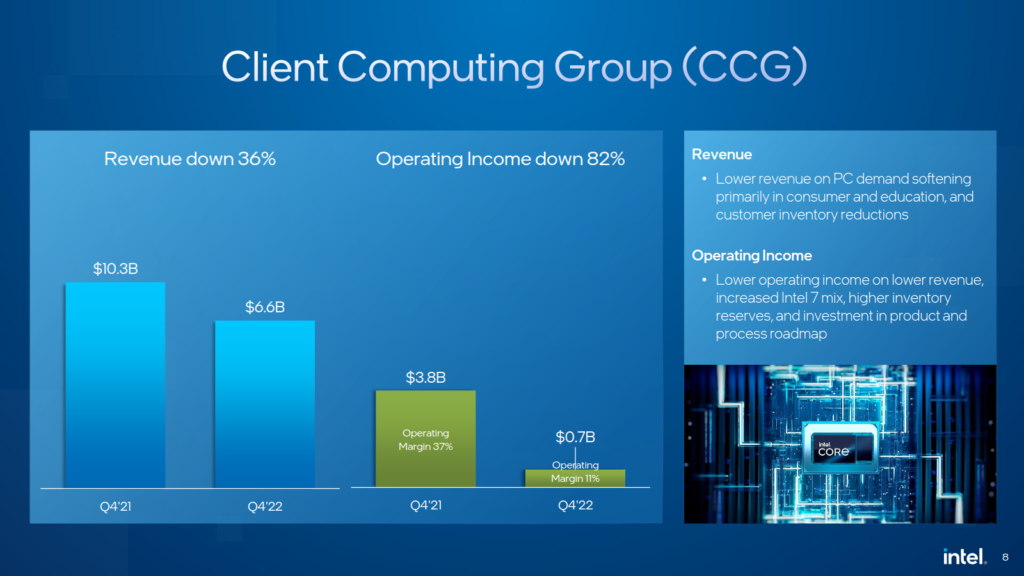

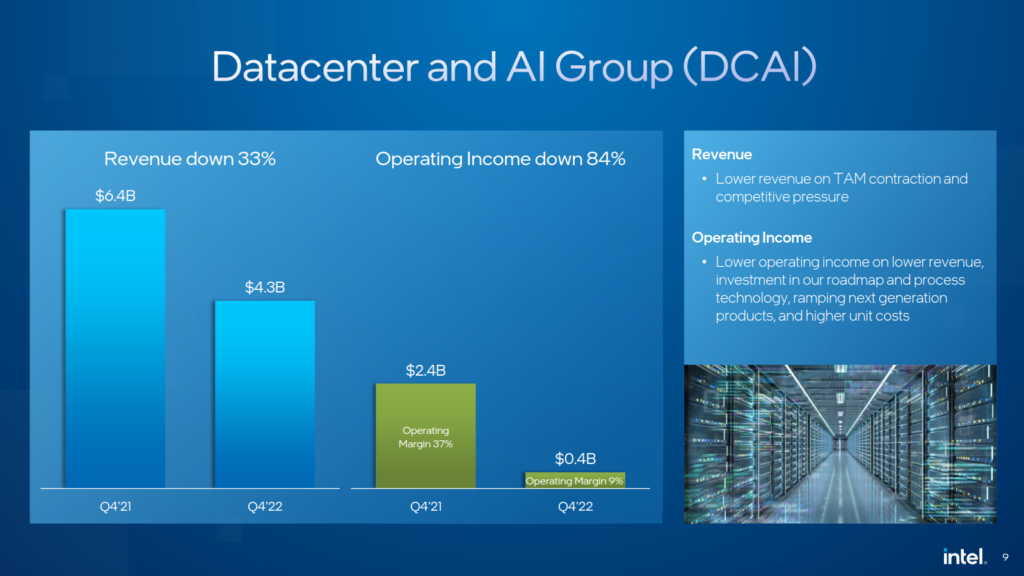

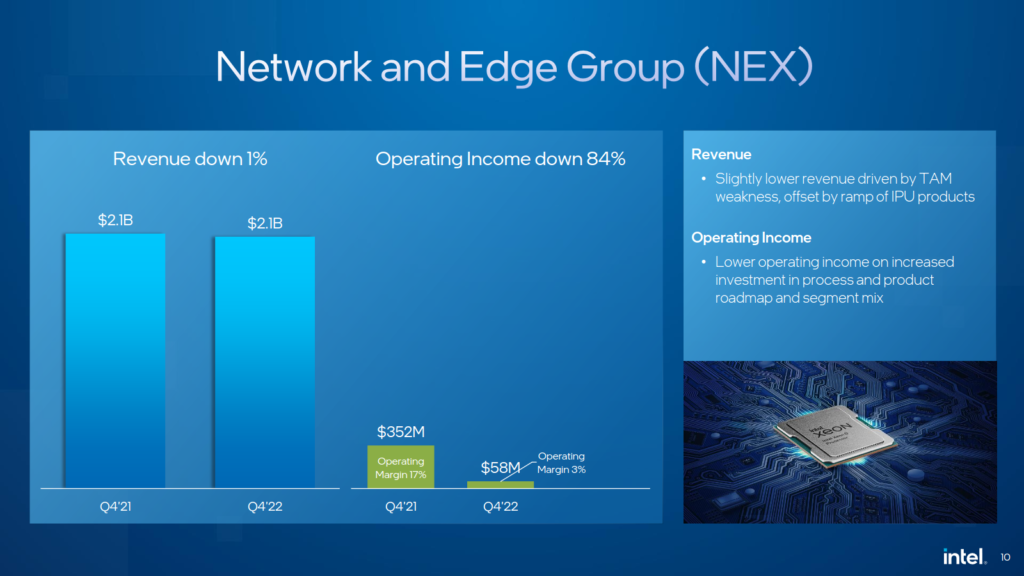

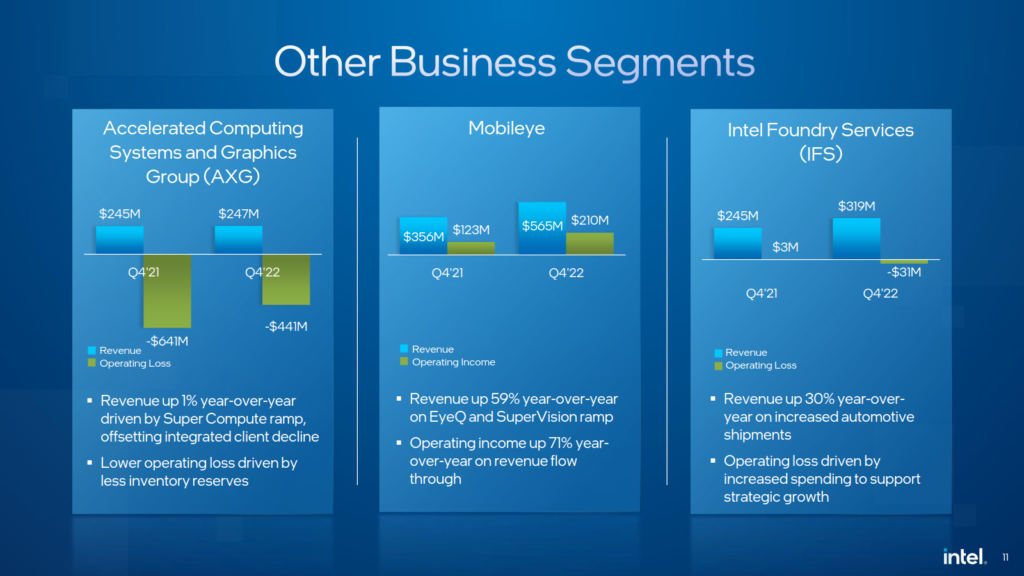

By Q4 2022, the earnings deck shows a series of bar graphs with downward trends for both revenue and operating income essentially in all business segments, as shown below:

By 2023:

- annual revenue had fallen to roughly $54 billion,

- gross margins declined toward the low-40% range,

- and free cash flow came under severe pressure.

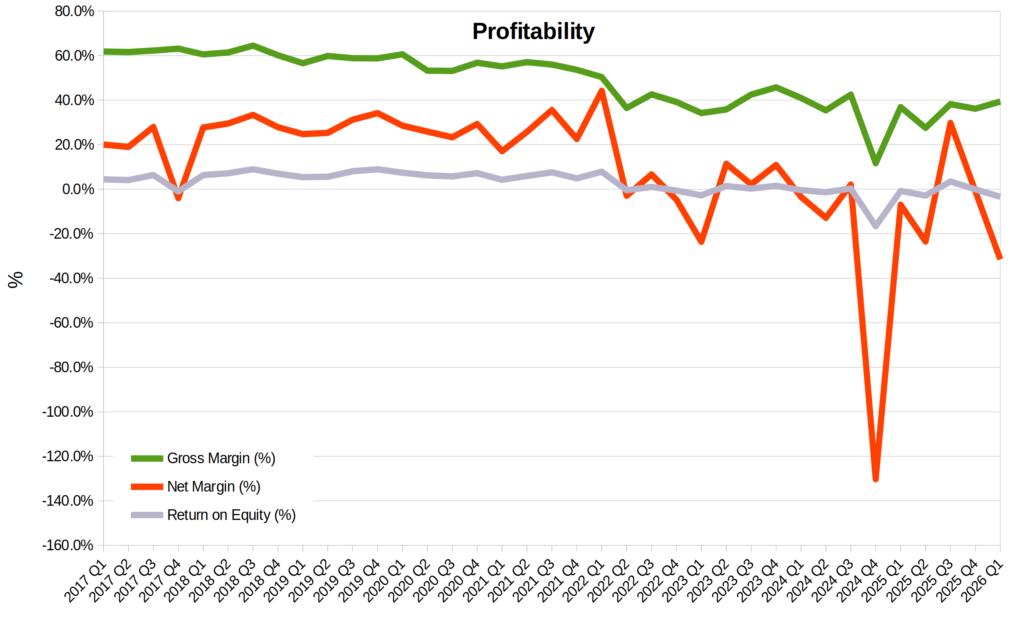

The magnitude of the margin deterioration was particularly striking. For decades, Intel had been known as one of the most profitable large industrial technology companies globally, frequently generating gross margins above 60%. The decline toward roughly 40% represented not merely cyclical weakness, but a dramatic compression in economic efficiency.

Several factors contributed:

- weaker PC demand after the pandemic,

- competitive pressure from AMD,

- heavy foundry-related investments,

- underutilized fabs,

- process transition costs,

- and rising depreciation expenses.

Unlike fabless competitors such as NVIDIA, Intel continued carrying the immense fixed costs associated with operating fabrication facilities, a difference that became increasingly visible during the AI boom.

NVIDIA’s asset-light fabless model allowed extraordinary profitability expansion, with net margins exceeding 50% during parts of the AI cycle. Intel, meanwhile, remained burdened by capital-intensive manufacturing operations and restructuring costs.

The contrast highlighted how differently semiconductor companies can behave financially depending on their position within the supply chain.

3.2 The 2024 Collapse

By 2024, investor sentiment surrounding Intel had deteriorated dramatically.

The stock declined from approximately $43 to below $20 as markets questioned:

- Intel’s technological competitiveness,

- the viability of its foundry ambitions,

- and whether the company could realistically catch up to TSMC and NVIDIA.

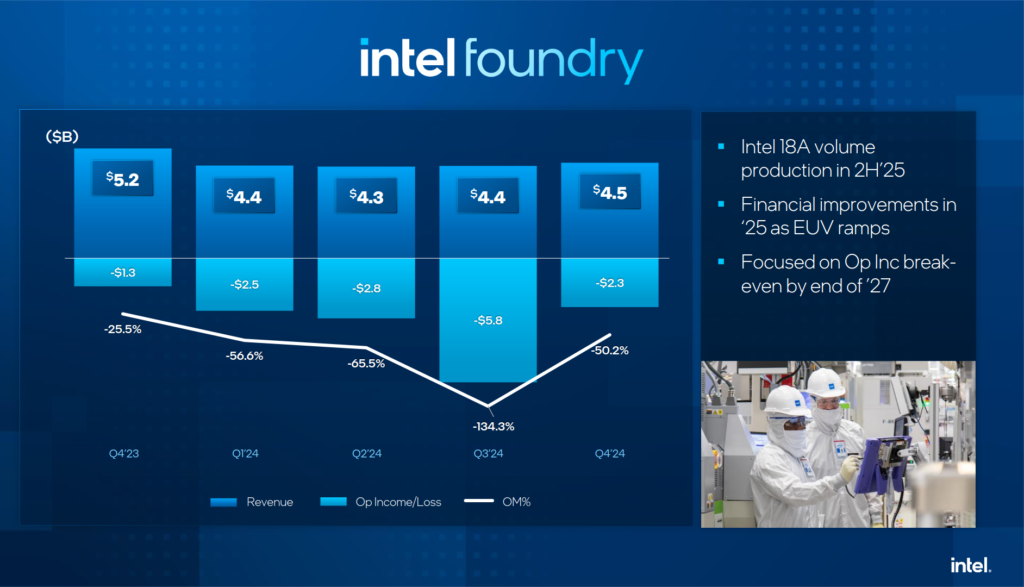

In Q4 2024, we can see how intel foundry was dragging the company’s results (notice the operating margins):

The dividend suspension further reinforced fears that Intel’s historical business model had fundamentally weakened.

At the lows, Intel increasingly traded less like a leading technology company and more like a distressed industrial turnaround dependent on government support and future execution.

In hindsight, this likely represented a phase of extreme pessimism.

Yet the pessimism was not irrational, as Intel faced:

- deteriorating margins,

- massive capital expenditures,

- technological delays,

- and some of the strongest competitors in the global semiconductor industry.

The key question was whether markets had begun extrapolating those challenges too aggressively into the future.

4. The Return of Optimism and the AI Narrative

4.1 Lip-Bu Tan and the Shift in Perception

One of the most important catalysts behind Intel’s recovery narrative was the arrival of Lip-Bu Tan as Chief Executive Officer in March 2025. Intel officially announced Tan’s appointment on March 12, 2025, with the role becoming effective on March 18, 2025.

Before joining Intel, Tan was best known for serving as CEO of Cadence Design Systems between 2009 and 2021. During his tenure, Cadence underwent a major operational and financial transformation, significantly improving margins, expanding revenue, and becoming one of the most important software providers within semiconductor design automation. Intel itself noted that Cadence’s stock appreciated by more than 3,000% during Tan’s leadership.

Tan also founded Walden International, a semiconductor-focused venture capital firm with deep ties across the global chip ecosystem. His reputation within the industry extends beyond management; he has long been regarded as one of the semiconductor sector’s most connected investors and strategic advisors.

Importantly, Tan had already served on Intel’s board before resigning in August 2024 amid reported disagreements regarding the company’s direction and pace of execution. His return as CEO was therefore interpreted by markets as a signal that Intel intended to accelerate operational discipline and execution credibility.

The market’s reaction was immediate. Intel shares rallied sharply following the announcement, reflecting renewed investor confidence that the company’s turnaround strategy might finally gain coherent leadership.

4.2 AI Changes Intel’s Strategic Positioning

The explosion in artificial intelligence infrastructure spending fundamentally altered how markets viewed semiconductor companies.

Importantly, Intel did not necessarily need to dominate AI accelerators to benefit from the broader AI boom.

AI growth increased demand for:

- CPUs,

- advanced packaging,

- networking,

- memory,

- foundry diversification,

- and domestic semiconductor manufacturing capacity.

While NVIDIA emerged as the dominant supplier of AI GPUs, the scale of AI infrastructure investment created opportunities across the semiconductor supply chain. Investors increasingly began viewing Intel not merely as a struggling CPU company, but as a potential strategic manufacturing and infrastructure asset within the AI economy.

At the same time, geopolitical concerns regarding Taiwan increased the perceived value of domestic semiconductor production capacity in the United States and Europe.

As a result, Intel’s valuation increasingly reflected:

- industrial policy,

- geopolitical diversification,

- and future AI infrastructure optionality,

rather than purely near-term earnings power.

This shift helps explain why Intel’s stock price recovered far faster than the company’s underlying profitability metrics.

5. Strategic Partnerships and Government Support

5.1 NVIDIA — From Competitor to Strategic Partner

One of the most important developments in Intel’s turnaround narrative has been the evolving relationship with NVIDIA.

Historically, the two companies occupied different but increasingly overlapping areas of the semiconductor industry. Intel dominated CPUs, while NVIDIA became the central player in AI acceleration through GPUs.

However, the AI boom created incentives for broader ecosystem cooperation.

Recent reports indicate that Intel and NVIDIA have expanded collaboration around:

- AI systems integration,

- CPU-GPU interoperability,

- advanced packaging,

- and potentially foundry manufacturing relationships.

In May 2026, Lip-Bu Tan publicly stated that Intel and NVIDIA were “collaborating to develop exciting new products,” further fueling speculation regarding deeper technological cooperation. Several reports also indicated that NVIDIA had invested approximately $5 billion into Intel as part of broader strategic cooperation efforts surrounding AI infrastructure and domestic semiconductor manufacturing.

The significance of this partnership extends beyond any individual product announcement. NVIDIA’s willingness to engage with Intel serves as a form of ecosystem validation for Intel Foundry Services. Even limited manufacturing or packaging cooperation from the dominant AI chip company materially improves Intel’s credibility within the semiconductor supply chain. This is particularly important because foundry businesses rely heavily on customer trust and ecosystem confidence. If companies such as NVIDIA are willing to cooperate with Intel Foundry Services at advanced nodes, markets may increasingly view Intel as a credible second-source manufacturing alternative to TSMC.

5.2 Apple — Symbolic Rehabilitation for Intel Foundry

Among the recent developments surrounding Intel, perhaps none carried more symbolic importance than reports regarding a preliminary manufacturing agreement involving Apple. In May 2026, multiple reports indicated that Apple and Intel had reached a preliminary agreement for Intel to manufacture some chips used in Apple devices. Discussions reportedly lasted more than a year before formal negotiations intensified in recent months.

The historical significance of this development is difficult to overstate. Apple’s transition away from Intel processors beginning in 2020 represented one of the clearest public signs of Intel’s technological decline. Apple abandoned Intel’s x86 processors in favor of internally designed ARM-based silicon manufactured primarily by TSMC. Now, years later, Intel may partially re-enter Apple’s semiconductor supply chain — not as a CPU supplier, but as a manufacturing partner.

According to reports, Apple may evaluate Intel’s 18A process technology for selected chips, potentially including lower-end or supplementary silicon products. Although the precise products and manufacturing volumes remain unclear, the market interpreted the development as a major validation event for Intel Foundry Services.

The agreement also reflects broader industry pressures. TSMC’s leading-edge capacity has become increasingly constrained due to explosive AI-related demand from customers such as NVIDIA, AMD, and hyperscale cloud providers. Apple therefore has incentives to diversify manufacturing relationships and secure additional advanced-node capacity. Importantly, this deal appears less about Apple abandoning TSMC and more about supply-chain diversification.

5.3 The U.S. Government and Intel as a Strategic Asset

A major component of Intel’s recovery narrative involves direct and indirect support from the United States government for semiconductor manufacturing and advanced packaging projects across Arizona, Ohio, New Mexico, and Oregon. Ultimately, the U.S. government acquired a 10% passive ownership stake in Intel in August 2025. The deal was finalized through an $8.9 billion agreement that converted previously unpaid Biden-era CHIPS Act grants and Defense Department funds into 433.3 million shares of Intel common stock.

The government’s role reportedly extended beyond financing. Several reports indicated that U.S. officials actively encouraged technology firms — including Apple and NVIDIA — to deepen cooperation with Intel Foundry as part of broader domestic semiconductor initiatives.

The broader message from Washington became clear: Intel was no longer viewed merely as a semiconductor company. Instead, it was increasingly treated as strategic infrastructure, domestic manufacturing capacity, and a geopolitical counterweight to Asian semiconductor concentration. This shift significantly changed investor psychology and contributed to the current valuation.

5.4 Tesla, Amazon, and Microsoft — The Hyperscale AI Opportunity

Intel has also pursued deeper relationships with hyperscale technology firms and AI infrastructure players including Tesla, Amazon, and Microsoft.

These relationships are particularly important because hyperscalers increasingly seek:

- custom silicon,

- advanced packaging capacity,

- AI inference optimization,

- and diversified semiconductor supply chains.

In Tesla’s case, reports have connected Intel to broader AI infrastructure and manufacturing initiatives associated with Elon Musk’s expanding ecosystem, including custom silicon and domestic chip manufacturing ambitions.

Meanwhile, Amazon and Microsoft continue investing aggressively in proprietary AI chips, cloud infrastructure, and sovereign compute capacity. This trend creates opportunities for Intel Foundry Services to participate in custom manufacturing, advanced packaging, or infrastructure partnerships even if Intel itself does not dominate AI accelerator design.

The broader implication is significant. The semiconductor industry is increasingly evolving toward vertically integrated AI ecosystems, custom silicon development, and geographically diversified manufacturing capacity. If Intel succeeds in becoming even a secondary supplier within this ecosystem, the company could secure a strategically important role despite trailing NVIDIA in AI accelerators and TSMC in manufacturing scale.

However, these partnerships remain early-stage relative to Intel’s long-term ambitions. Announcements and strategic agreements improve perception, but Intel still faces the difficult challenge of converting ecosystem relevance into sustainable foundry profitability.

6. Financial Analysis — Valuation Ahead of Fundamentals?

6.1 Revenue Decline and Margin Compression

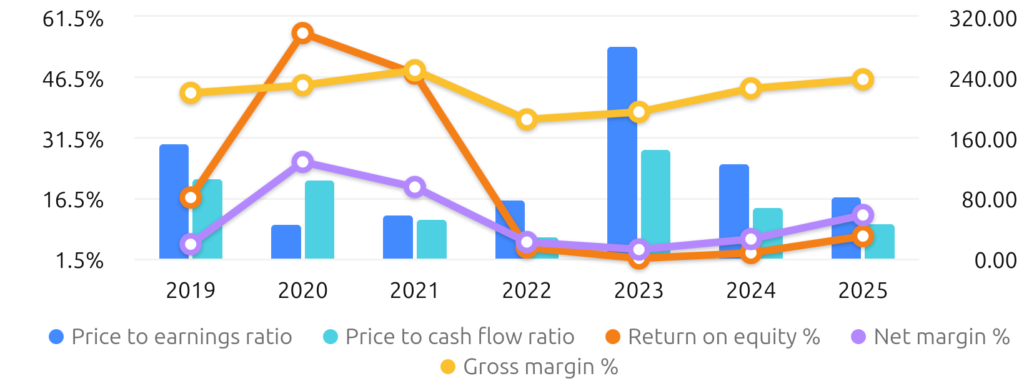

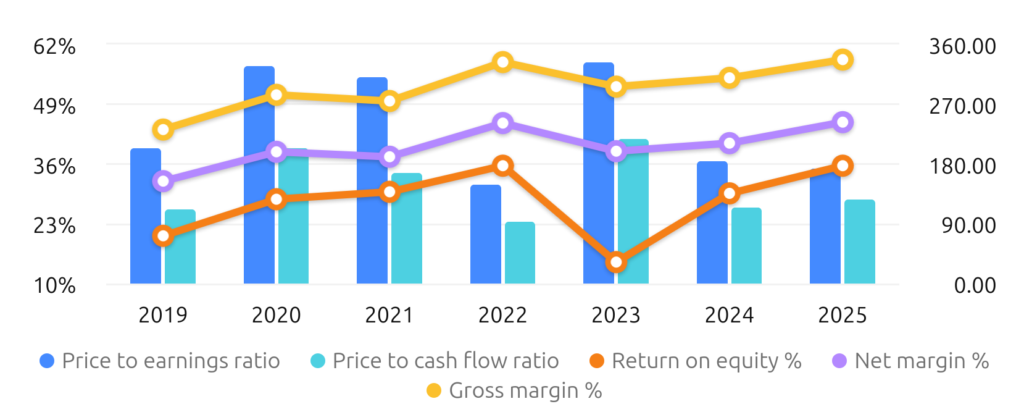

Between 2017 and 2021, Intel remained a highly profitable (gross margins ~60%, net margins ~25%) semiconductor company generating relatively stable revenue and multi-billion-dollar quarterly earnings. However, beginning in 2022, the company entered a period of severe margin compression and earnings deterioration driven by competitive pressure, foundry investments, weaker PC demand, and restructuring costs.

Since 2022 Intel has not been profitable (close to zero net income). Additionally, this business is heavily reliant on fixed assets and infrastructure which is not fully utilized yet, resulting in a small return on equity, which went from ~6% in the period 2017-2021 to an average of -0.8% in the years 2022-2026.

6.2 The Foundry Cost Problem

Intel historically operated with software-like semiconductor margins. However, the company’s push to rebuild manufacturing leadership and scale foundry operations materially compressed profitability. By contrast, NVIDIA’s fabless model allowed margins to expand dramatically during the AI cycle. AMD also experienced margin pressure during the post-pandemic slowdown, although profitability remained positive and margins began improving again from 2025 onward.

The Taiwanese chip manufacturer TSMC has taken advantage of scale and specialization to keep the fab business profitable. “Margins and return on equity remain strong and have continued improving in recent years.” However, the company’s valuation already reflects considerable optimism. Although TSMC’s valuation appears elevated relative to historical industrial companies, the firm combines characteristics rarely found together: dominant market share, exceptional returns on capital, structural barriers to entry, geopolitical importance, and exposure to nearly every major growth area within semiconductors.

Semiconductor foundries exhibit extreme operating leverage. Once fabrication plants are built, incremental production can generate substantial profitability provided utilization rates remain high. TSMC’s scale advantage and dominant market position allow the company to maintain high utilization across multiple technology cycles, supporting strong margins despite the capital intensity of the business.

Unlike Intel, which historically depended heavily on the success of its own processor products, TSMC benefits from the broader growth of the semiconductor ecosystem itself. Whether AI demand ultimately favors NVIDIA, AMD, Apple, Qualcomm, or custom hyperscaler silicon, much of the manufacturing demand still flows through TSMC’s fabs.

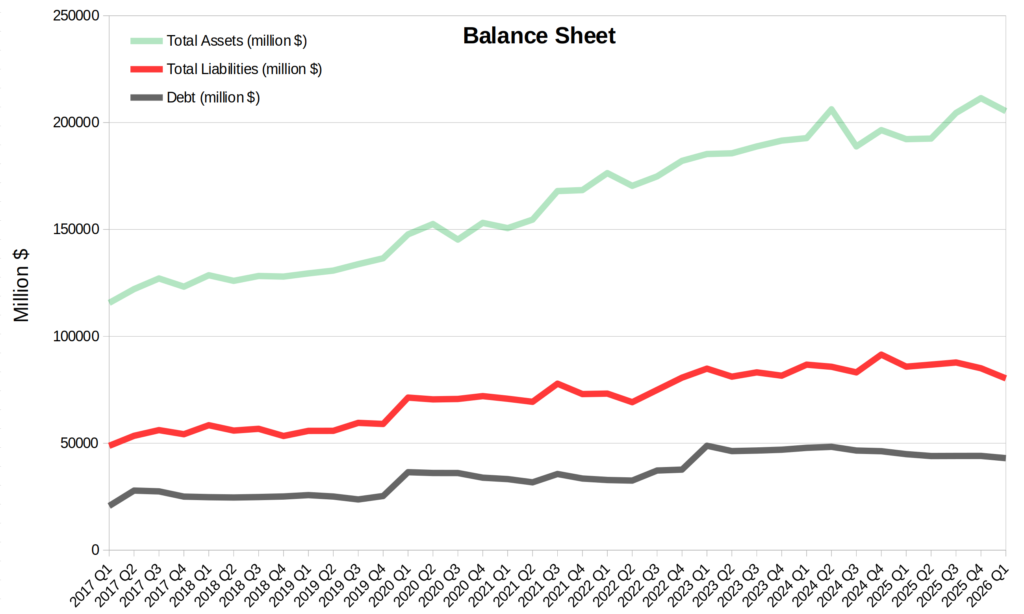

6.3 Balance Sheet Expansion and Capital Intensity

Intel’s turnaround is not occurring through financial engineering or software scalability. It is being attempted through one of the largest industrial investment cycles in the semiconductor industry. To fund these investments, Intel’s debt has jumped considerably in 2020 and in 2023.

The rise in total assets reflects fab construction and infrastructure buildout, which can be a sign of a promising future – if these assets are properly utilized and if Intel is capable of securing new customers into its fab business. If it fails to do so, the new infrastructure will be an even bigger drag on earnings – and the last nail in the coffin of the historical silicon giant.

Intel’s historical vertically integrated structure was once a major strategic advantage. However, as semiconductor manufacturing became increasingly specialized and capital-intensive, the industry gradually shifted toward a separation between chip design and fabrication. This transition favored fabless firms with lighter balance sheets and foundries with sufficient scale to spread capital costs across many customers.

6.4 The Recovery in Market Valuation

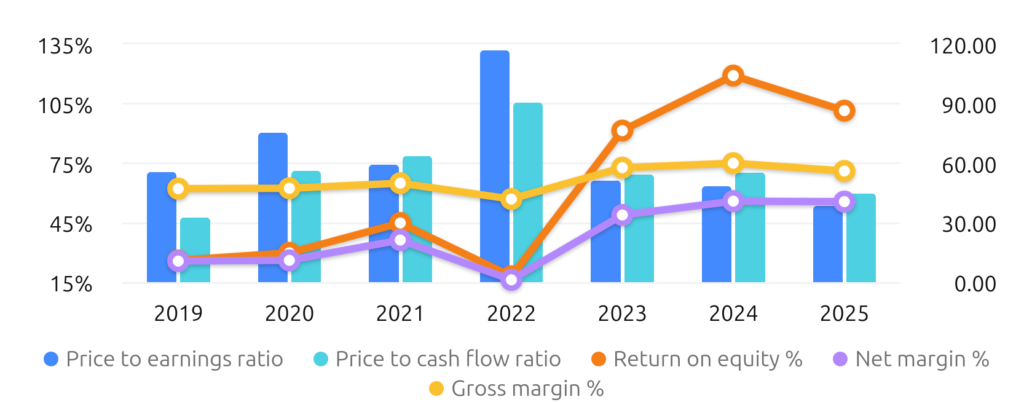

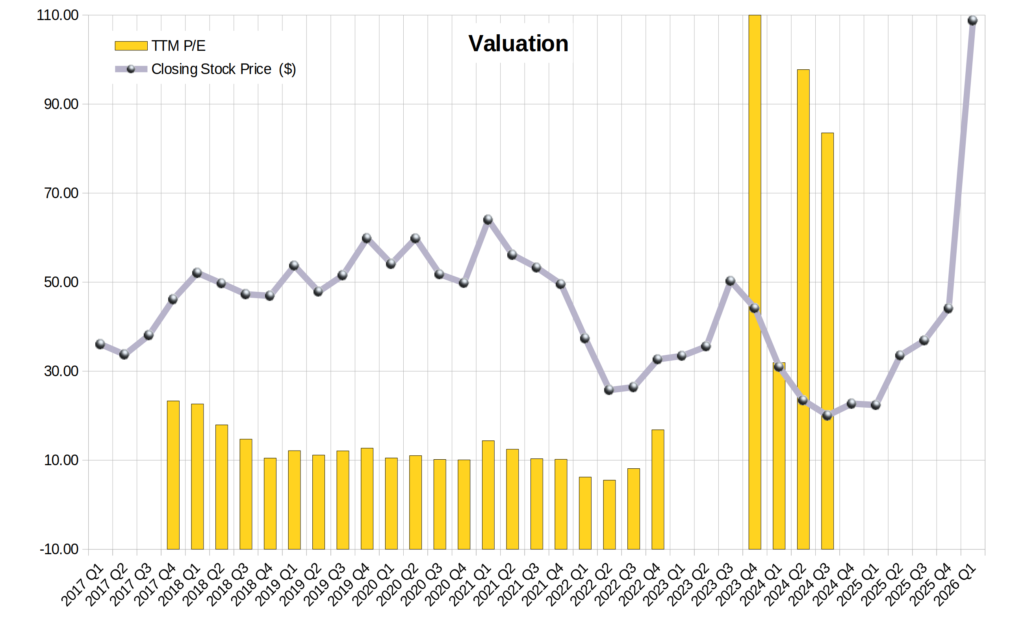

The stability of Intel’s earnings until late 2021 granted a very reasonable valuation with a P/E ratio around 10, and a stock price with low volatility. However, in the period 2022-2024, as both the top line and the bottom line shrunk, the volatility increased.

Ironically, despite Intel’s substantially weaker margins and ongoing restructuring challenges, recent market enthusiasm surrounding AI infrastructure and domestic manufacturing has led investors to rapidly re-rate the company’s valuation. The market increasingly appears willing to price Intel based on future strategic importance rather than current profitability (which is none).

7. The Verdict: Narrative Versus Economics

Intel’s recovery story reflects one of the defining characteristics of financial markets: the tendency for investor sentiment to swing between extremes. At the lows near $19 per share, markets appeared to assume that Intel’s decline was largely irreversible. The pessimism of 2024 underestimated Intel’s strategic importance, manufacturing base, and potential role within a rapidly changing geopolitical environment. The optimism of today may similarly underestimate the immense execution challenges involved in rebuilding manufacturing leadership and scaling a profitable foundry business.

Intel stock is up 400% since a year ago and now trades above $100 (let’s see for how long!). However, Intel’s turnaround remains incomplete. The company still faces substantial competitive pressure, high capital expenditures, uncertain foundry economics, and the challenge of converting long-term strategic positioning into durable financial performance. The current financial performance of the company is essentially unaltered, despite the CEO saying the company is fundamentally different. What changed were the narratives surrounding partnerships and an increased geopolitical relevance.

At the same time, Intel no longer needs to fully dominate the semiconductor industry to justify at least part of its recovery. In a world increasingly focused on AI infrastructure, supply-chain resilience, and domestic manufacturing capacity, strategic relevance itself has acquired economic value. Whether current valuations ultimately prove justified will ultimately depend on the gradual re-emergence of sustainable profitability, stronger margins, reliable execution, and credible long-term returns on invested capital.

The market has already moved from extreme pessimism toward renewed optimism.

The remaining question is whether Intel’s underlying economics can eventually catch up to the narrative – is the giant up to the challenge? The ongoing investments and strategy will take a few more years to fully materialize – now, we have to wait.

Disclosure: The author held shares of Intel during portions of 2024 and 2025 but does not currently hold a position in the company. This article reflects the author’s personal analysis/opinions and should not be interpreted as investment advice.

Sources and Reference Material

Company and Investor Relations Sources

- Intel Investor Relations

- Intel SEC Filings Archive

- Intel Newsroom – Lip-Bu Tan Appointment

- Intel Q1 2026 Earnings Materials

Financial and Industry Sources

- Reuters – Intel Stock Recovery Analysis

- Reuters – Apple and Intel Manufacturing Agreement

- Tom’s Hardware – Apple and Intel Deal Analysis

- PC Gamer – Intel and NVIDIA Collaboration

Suggested Books and Background Reading

- Chip War by Chris Miller

- The Intel Trinity by Michael Malone

- Only the Paranoid Survive by Andrew Grove