Introduction — Markets Follow Liquidity, Not Narratives

Financial markets are often described as mechanisms that price fundamentals, expectations, and risk, yet in practice they are far more sensitive to a less visible but more powerful force: liquidity. While economic narratives shift constantly—growth versus recession, inflation versus disinflation—asset prices tend to move most consistently with the availability of capital, rather than with the stories used to justify those movements.

Liquidity, in this sense, is not simply cash in the system, but the capacity and willingness of financial actors to deploy capital, and it is this capacity that ultimately determines whether markets rise, stagnate, or collapse.

I. What Is Liquidity? A Functional Definition

Liquidity is often loosely defined as the amount of money in the system, but such a definition is insufficient, as it fails to capture the mechanisms through which capital is created, transmitted, and deployed across the financial system.

A more precise definition would describe liquidity as the ease with which assets can be bought or sold without significantly impacting their price, combined with the availability of credit and funding to support those transactions. In other words, liquidity is both a stock (money available) and a flow (money in motion).

This distinction is important, because a system may appear liquid in aggregate terms while still experiencing localized shortages, particularly when credit conditions tighten or when market participants become unwilling to provide liquidity at prevailing prices.

II. Measuring Liquidity — Imperfect Proxies

Unlike inflation or GDP, liquidity cannot be observed directly and must instead be inferred through a set of imperfect indicators, each capturing a different dimension of the system.

One commonly used proxy is the money supply, particularly measures such as M2 money supply, which includes cash, deposits, and near-money instruments. While useful, M2 captures only the stock of money and does not fully reflect credit dynamics or financial market conditions.

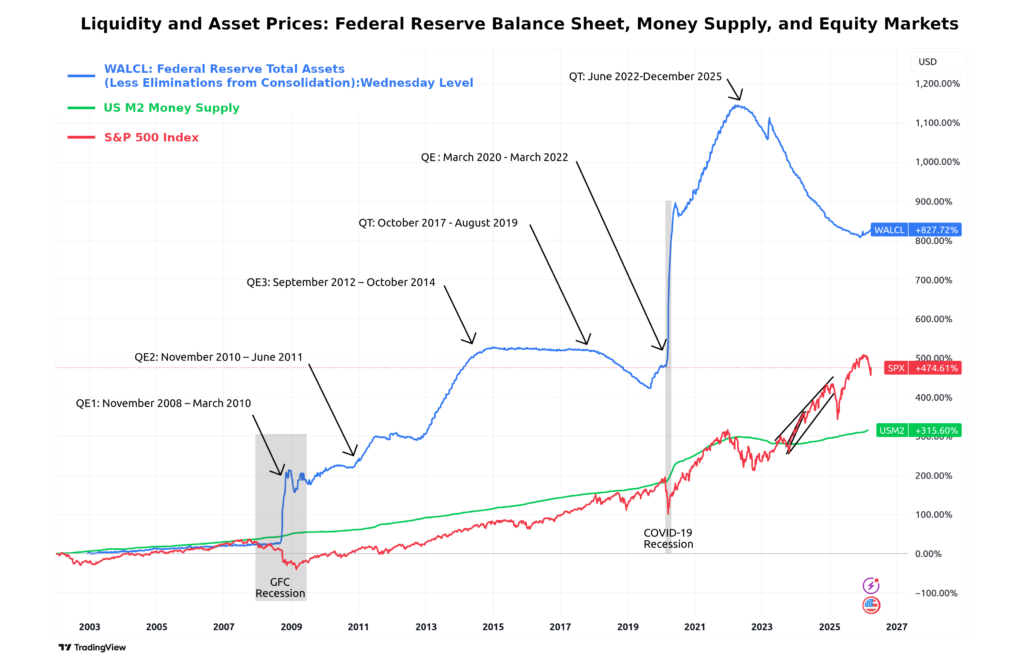

Central bank balance sheets provide another important signal, particularly through the actions of institutions such as the Federal Reserve, whose asset purchases and lending programs directly inject reserves into the banking system. Expansions of the balance sheet are generally associated with increased liquidity, while contractions signal tightening conditions.

Market-based indicators, such as credit spreads, repo rates, and volatility indices, offer a more dynamic view of liquidity, reflecting the cost and availability of funding in real time. For instance, widening credit spreads often indicate a deterioration in liquidity conditions, as lenders demand higher compensation for risk.

Ultimately, no single metric captures liquidity in its entirety, and a comprehensive view requires combining monetary, financial, and market-based indicators.

Sources:

- Federal Reserve balance sheet (H.4.1): https://www.federalreserve.gov/releases/h41/

- M2 data (FRED): https://fred.stlouisfed.org/series/M2SL

III. How Money Is Created — Credit as the Engine of Liquidity

A common misconception is that money is primarily created by central banks, when in reality the majority of money in modern economies is created through commercial bank lending, a process in which new deposits are generated when banks extend credit.

When a bank issues a loan, it simultaneously creates a deposit in the borrower’s account, effectively expanding the money supply. This process, often described within the framework of fractional-reserve banking, means that liquidity is fundamentally linked to the willingness of banks to lend and the demand for credit from borrowers.

Central banks influence this process indirectly through interest rates, reserve requirements, and regulatory conditions, but they do not fully control it. As a result, liquidity is highly procyclical: it expands during periods of optimism and contracts during periods of stress.

This dynamic explains why credit conditions are so closely tied to economic cycles, as tightening lending standards can quickly translate into reduced liquidity and declining economic activity.

Sources:

- Bank of England, “Money creation in the modern economy”: https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy

- BIS credit statistics: https://www.bis.org/statistics/credit.htm

IV. Central Banks and Liquidity — QE, QT, and Intervention

While banks create money through lending, central banks play a crucial role in shaping liquidity conditions through monetary policy tools, most notably Quantitative Easing and Quantitative Tightening.

Quantitative Easing (QE) involves large-scale asset purchases, typically government bonds, which increase bank reserves and lower yields, thereby encouraging lending and risk-taking. In contrast, Quantitative Tightening (QT) reduces the size of the central bank’s balance sheet, withdrawing liquidity from the system and often leading to tighter financial conditions.

Beyond these structural tools, central banks also intervene during periods of market stress through emergency liquidity facilities, such as repo operations or direct lending programs, as seen during the Global Financial Crisis and the COVID-19 market crash, when liquidity support was deployed at unprecedented scale to stabilize markets.

These interventions highlight an important reality: liquidity is not only a market phenomenon, but also a policy variable, subject to active management by central authorities.

Liquidity expansions, particularly during periods of quantitative easing, have consistently coincided with strong asset price performance, while periods of balance sheet contraction have been associated with weaker or more volatile market conditions.

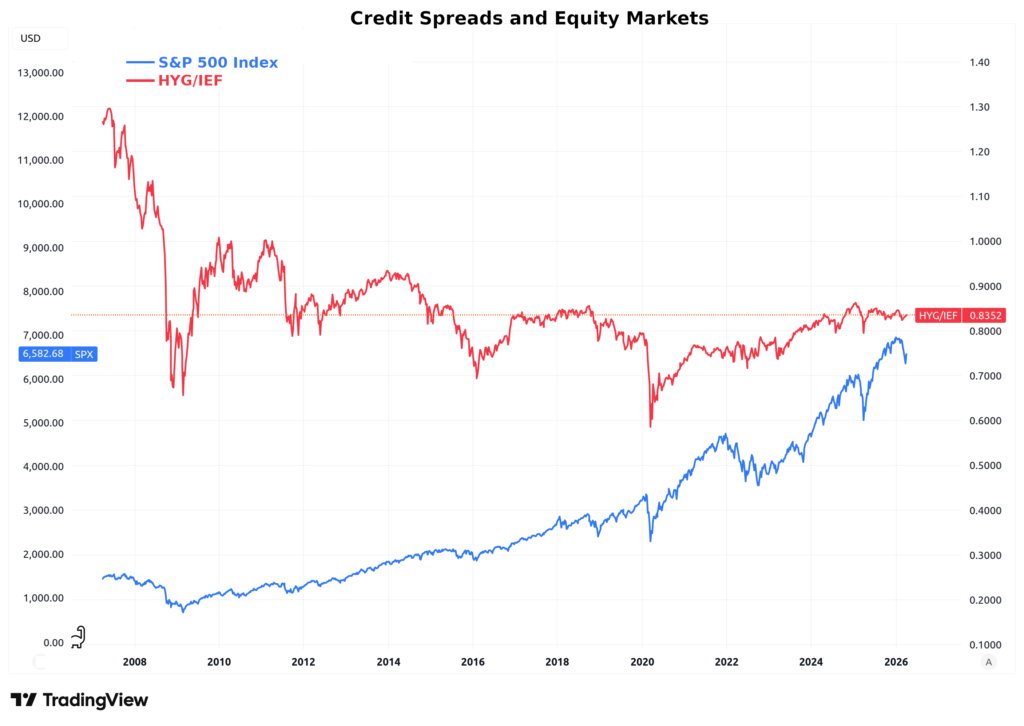

Credit spreads, proxied in the figure below by the relative performance of high-yield bonds versus Treasuries, do not consistently lead equity markets, but rather reflect the underlying state of financial conditions. While spreads showed clear signs of stress ahead of the 2008 financial crisis, most subsequent episodes—such as the European sovereign crisis, the 2015–2016 growth scare, and the COVID-19 shock—were characterized by simultaneous repricing across asset classes. This suggests that credit markets tend to lead only when the source of instability originates within the financial system itself, while in broader macro shocks, spreads and equities adjust in tandem.

Sources:

- Federal Reserve QE programs: https://www.federalreserve.gov/monetarypolicy.htm

- ECB asset purchase programmes: https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html

V. When Liquidity Dries Up — Historical Episodes

Periods of financial stress are often characterized not by a lack of assets or opportunities, but by a sudden disappearance of liquidity, as market participants become unwilling or unable to transact.

During the Global Financial Crisis, the collapse of structured credit markets led to a freezing of interbank lending, as trust between institutions deteriorated and funding markets seized up. Similarly, in March 2020, even highly liquid assets such as U.S. Treasuries experienced severe dislocations, requiring intervention from the Federal Reserve to restore market functioning.

Conversely, periods of abundant liquidity, such as the post-2009 QE era or the stimulus-driven environment of 2020–2021, have been associated with strong asset price appreciation across equities, real estate, and alternative assets, reflecting the expansion of capital available for investment.

These episodes illustrate that liquidity is not constant, but cyclical, and that its contraction can have rapid and far-reaching consequences.

Sources:

- IMF Global Financial Stability Reports

- Federal Reserve, March 2020 interventions

VI. Asset Prices and Liquidity — Transmission Across Markets

Liquidity does not impact all assets equally, but its influence is pervasive across financial and real asset classes.

Equities tend to benefit directly from increased liquidity, as lower discount rates and greater risk appetite drive valuations higher, particularly for growth-oriented sectors. Bonds are influenced both by liquidity and by policy, as central bank purchases can compress yields and reduce volatility.

Commodities respond to liquidity through both financial and real channels, as increased capital flows into futures markets while economic expansion supports demand. Meanwhile, alternative assets such as real estate, art, and collectible markets often experience delayed but pronounced effects, as excess liquidity eventually seeks diversification into less liquid stores of value.

Historical examples reinforce this relationship: the post-2008 QE period saw a sustained rise in equity and real estate markets, while the liquidity surge following the COVID-19 market crash contributed to rallies not only in stocks but also in speculative assets, including cryptocurrencies and collectibles.

In this sense, liquidity acts as a common denominator across asset classes, shaping not only price levels but also correlations and market dynamics.

VII. Liquidity as a System-Level Constraint

Ultimately, liquidity represents a system-level constraint on financial markets and the broader economy, determining not only what is possible, but also what is sustainable.

When liquidity is abundant, capital flows freely, risk is embraced, and asset prices rise. When liquidity contracts, the same system can quickly reverse, as funding becomes scarce, risk tolerance declines, and prices adjust downward.

This dynamic underscores a key insight: markets are not solely governed by fundamentals, but by the interaction between fundamentals and liquidity, with the latter often dominating in the short to medium term.

Conclusion — Tracking Liquidity, Not Narratives

Understanding liquidity is therefore essential for interpreting market behavior, not as a predictive tool, but as a framework for understanding how and why capital moves.

While narratives will continue to evolve, liquidity provides a more stable lens through which to view markets, offering insight into the underlying forces that drive cycles, amplify trends, and ultimately shape economic outcomes.